In the last few months, we’ve seen a real urgency from the Modi government to reduce the Indian economy’s dependence on hard cash. Multiple digital payment options have surfaced in this time. From retailers to banks, from the common man to the state, everyone has had to familiarise himself with internet or mobile-linked payment systems to get by.

In the last few months, we’ve seen a real urgency from the Modi government to reduce the Indian economy’s dependence on hard cash. Multiple digital payment options have surfaced in this time. From retailers to banks, from the common man to the state, everyone has had to familiarise himself with internet or mobile-linked payment systems to get by.With the 2017 budget, the government has taken digital transacting a notch higher by proposing the addition of 20 lakh Aadhaar-based Point of Sale (POS) machines by September 2017. An Aadhaar card has a unique identification number along with unique biometric data such as your thumbprint which work as a proof of identity and can be used to authenticate transactions settled directly from a user’s Aadhaar-linked bank account.

This is a significant development since there are now over one billion Indians with an Aadhaar ID, and they can now start transacting cashlessly when Aadhaar Pay becomes operational.

How Aadhaar Pay works

As a customer, you would require three things to carry out a transaction: your Aadhaar card number, your bank account linked to your Aadhaar card, and your fingerprint to authenticate the transaction.

A merchant, on the other hand, would need to install a fingerprint/biometric scanner, a smart phone with the number linked to his bank account, the Aadhaar Pay app on phone, internet/data connection and a bank account to get the payment credited.

The merchant must first install the Aadhaar Pay app on his smart phone and create a registered ID. Thereafter, the smart phone should be linked with the fingerprint scanner. Once the setup is complete, the customer can provide with the name of his bank, Aadhaar number and register his fingerprint on a biometric scanner to authenticate his transaction.

Advantages of Aadhaar Pay

This is highly effective for people living in rural and semi-urban areas in becoming a part of the banking system. The regions, which were cash-driven due to lack of access to debit and credit cards and e-wallets can now enjoy hassle-free transactions through Aadhaar cards.

Transactions through Aadhaar do not attract any extra charges unlike debit or credit cards at POS machines. While a POS machine costs more than Rs. 5000, a biometric scanner for Aadhaar Pay can be installed for Rs. 2000 only.

Transactions through Aadhaar Pay are secure since they require your presence and biometric authentication.

There are no annual charges associated with Aadhaar Pay yet unlike debit and credit cards, so you can consider reducing your dependence on plastic money in the future.

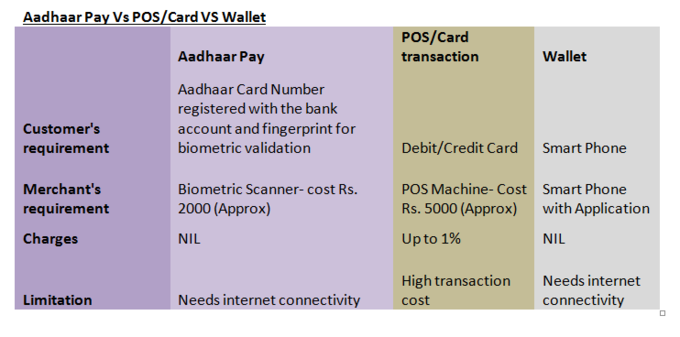

Aadhaar Pay Vs POS/Card VS Wallet

Customer's requirement Aadhaar Card Number registered with the bank account and fingerprint for biometric validation Debit/Credit Card Smart Phone

Merchant's requirement Biometric Scanner- cost Rs. 2000 (Approx) POS Machine- Cost Rs. 5000 (Approx) Smart Phone with Application

Charges NIL Up to 1% NIL

Limitation Needs internet connectivity High transaction cost Needs internet connectivity

Limitations

Aadhaar Pay works only where there is internet connectivity. While it is an effective mode of payment at merchant points, it cannot be used to transfer funds to another account.

If a customer wants his money back after making payment, there’s no way to immediately understand if the money has been credited back to his bank account.

E-wallets Vs

E-wallets require you to carry a smart phone, thus limiting its access to a certain set of people. You need to transfer money from your bank account to load your e-wallet before use, which may not seem user-friendly to many. Aadhaar Pay on the other hand is directly connected to your bank account allowing you to make payment without any limitations.

However, e-wallets offer you with cash backs and discounts on merchandise through business tie ups, which are missing in case of Aadhaar Pay.

Aadhaar Pay is going to revolutionize