All this is based on hopes that the BJP-led NDA will emerge victorious in the 2014 polls and that

The

|

Are these expectations running ahead of the ground reality? Can the election results really make a difference to the fundamentals that drive stock prices? How should investors play the stock markets, both in the run-up to the elections and afterwards? Our cover story this week attempts to answer these questions and tell you how to handle your equity

Great expectations

Barely five months from now, India will elect the 16th

|

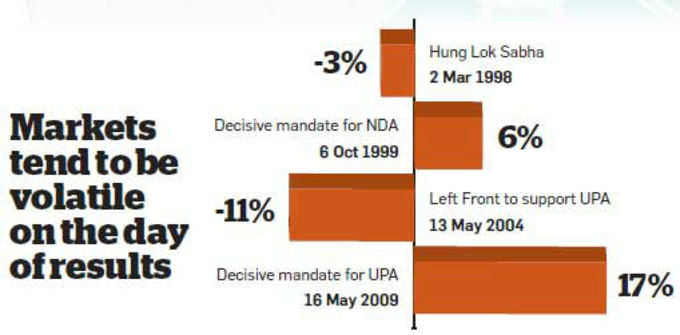

However, markets don’t wait for events to happen and discount them early on.

However, sentiments can carry the markets only so far. So, while the current positive mood will play a pivotal role and drive the markets in the near term, the rally will not be sustainable without the fundamentals matching the expectations. Only an improvement in the investment cycle can revive the economy. Sonal Varma and Aman Mohunta of Nomura point out, “The state elections are likely to boost sentiment, but they should not have any immediate impact on the fundamental outlook. India’s economic growth is bottoming out, but weak domestic demand amid tighter fiscal and monetary policies is likely to prevent any meaningful take-off.”

|

As far as the macro indicators go, the economy is still going through the motions. Even though the September quarter saw a marginal improvement in the GDP growth over the previous quarter, it is still near its 10-year low. The government has managed to control the current account deficit primarily by restricting

The other data paints a worrying picture. Industrial production declined by 1.8% in October, as against the 2% growth registered in September.

|

Another argument against fixation on a particular leadership is the historical continuity in reforms. In the past, reforms have come through irrespective of the party in power. For instance, some major economic reforms happened when the much-hated Third Front was in power (see page 16). For all its perceived shortcomings, even the incumbent

Experts agree that a stable government is more important than the party that comes to power. Nandkumar Surti, managing director and CEO,

How can expectations be derailed?

Even so, several factors could thwart the expectations of a sweeping change. Despite the anti-incumbency wave, which was visible in the state elections, it may not actually turn out to be a clear victory for the BJP. As Nomura points out, “State election outcomes are not always a reliable indicator of the general election prospects. Even if antiincumbency proves to be a core theme in the 2014 general election, it does not follow, of course, that the BJP would necessarily be the main beneficiary.” For instance, the newly formed

If there is a stable government after elections, it will take away a lot of uncertainty associated with the economy and support any recovery in the future. Of course, this is assuming that the ruling party will earnestly take up the cause at all. It remains to be seen whether the incoming party will have the resolve to take tough decisions, including those on diesel price decontrol, removal of subsidies, etc.

External risks could also play spoilsport. First is the threat of a downgrade of the Indian economy by global ratings agencies. S&P already has a ‘negative’ long-term outlook on India, the only one of the three rating agencies with this view. It has now warned of the possibility of a further downgrade in case of a hung Parliament or failure of the incoming government to push through key reforms. This would give government bonds ‘junk’ status, which can have very serious, negative implications for the economy.

|

A rating downgrade would not only cause a flight of

The second threat is from the winding down of the

What you should do

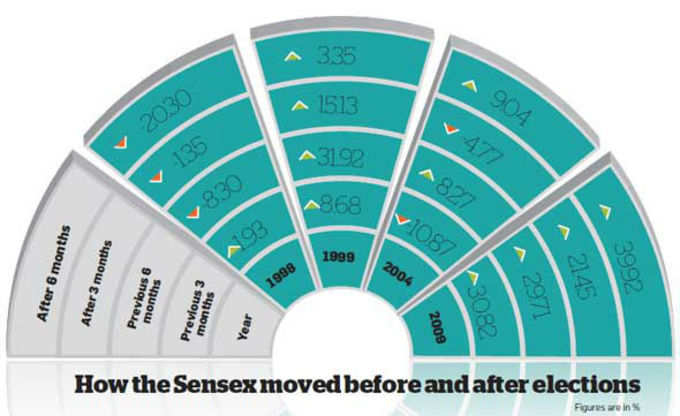

Whatever the outcome, it is a given that the stock markets will be heavily influenced by political developments till the elections and afterwards as well (see graphic). We would caution investors to temper their expectations and not be carried away with the upbeat mood. As Nomura cautions, “We think that chasing the rally is not prudent, as it remains to be seen how the incumbent party will react to its poor showing in the state elections.” Investors may remain hopeful, but should avoid giving in to the euphoria. If those hopes are not realised, the market reaction may be adverse, opines Pankaj Pandey, head of research,

Do not wait for election outcome

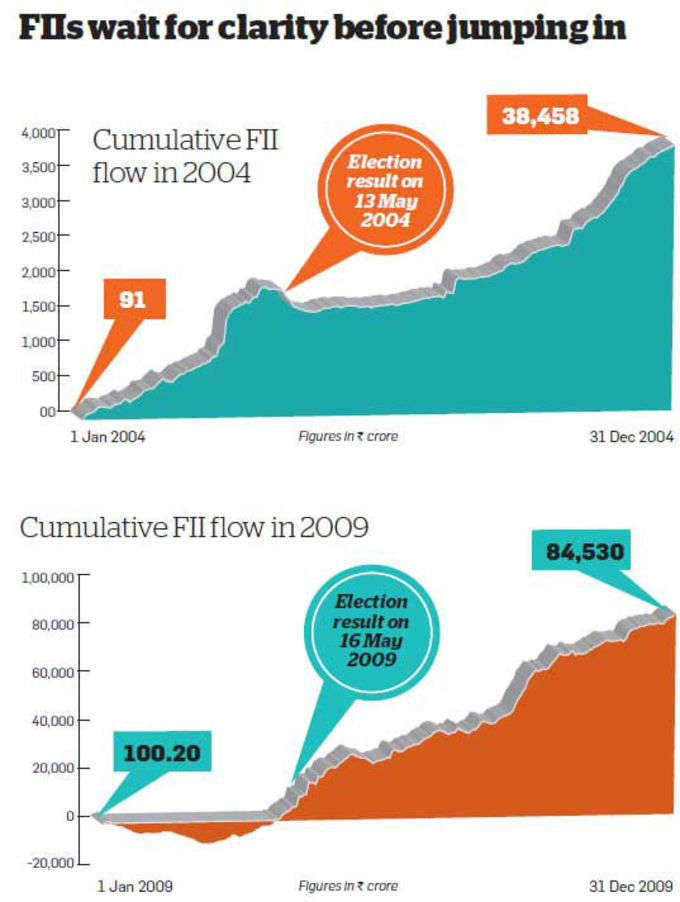

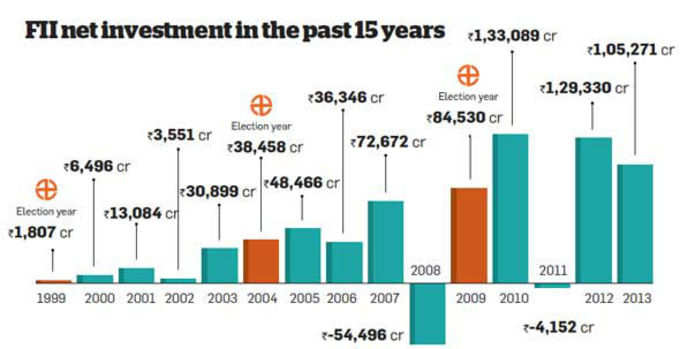

Some investors may be planning to stay out of the market till the elections are done with and clarity emerges. This may not be the best approach. As mentioned earlier, the markets don’t wait for events to happen. They would have already taken a course by the time the results are out. Surti insists, “The risk-reward equation is quite favourable right now and this is an opportune time for investors to start allocating to

As Pandey suggests, “Investors can remain light on stocks for the time being and invest in a staggered manner in the coming months.” However, be prepared for higher volatility as the markets are likely to be on tenterhooks till the results are out. Investing in equity

|

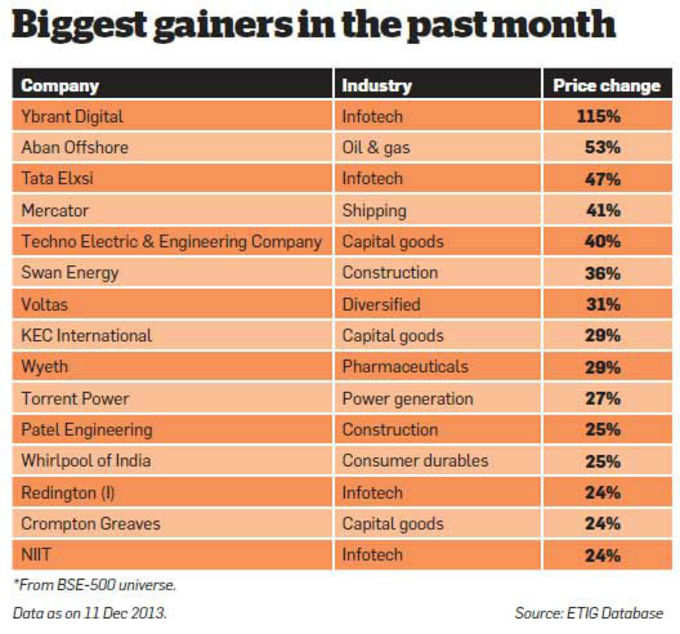

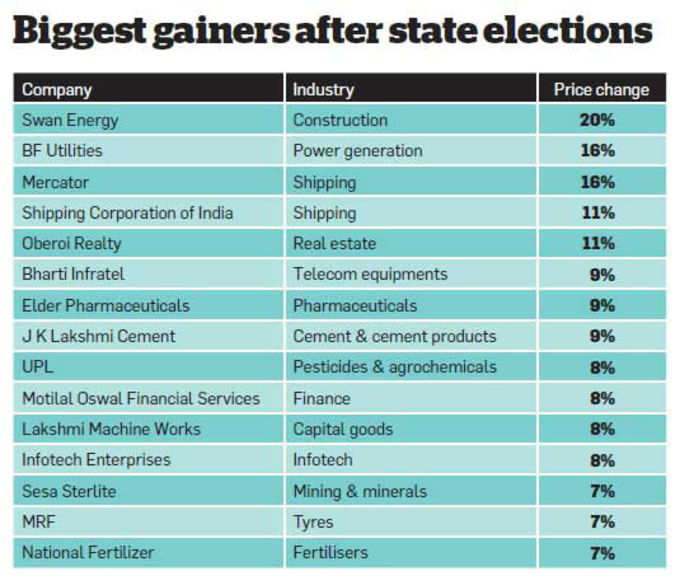

A few stocks shot up after the state poll results (see table). It would be too early to view this as a clear trend. Most economic indicators show that there is a long way to go for a turnaround in the investment cycle. However, you should catch hold of certain investment themes that are likely to play out in the event of an economic recovery and possible pick-up in investments. Besides, it is time that investors gradually lowered their exposure to overvalued defensive stocks and started adding cyclicals to their portfolio over the coming months. Many stocks in the capital goods, banking and auto sectors are available at cheap valuations. It is now a good entry point for those looking to invest for the next 3-5 years or more. Nomura asserts, “We expect market gains to be led by high-beta domestic cyclicals (banks and industrials, mainly) and expect defensives (

|

Do not let go of defensives

While defensive sectors are expected to underperform, don’t exit these sectors completely. Any turnaround in the economy will take some time to fructify. “We do not expect a pick-up in the investment cycle in the next two to three years,” insists Mishra. This means shifting completely in favour of economy-sensitives may not be a good strategy at this point. However, Mishra expects income growth at the bottom of the income pyramid to stay robust, which bodes well for the consumption sector. Defensives (consumer staples and pharma) and export themes (IT services) remain a good play given the struggling economy and weak currency. Shah says, “Investors should have a mix of defensives and economy-sensitives in their portfolios.” However, investors should avoid defensive stocks quoting at high valuations.

|

|