The Stock Market Is Not Doomed To Crash - Here's The Full Argument Why

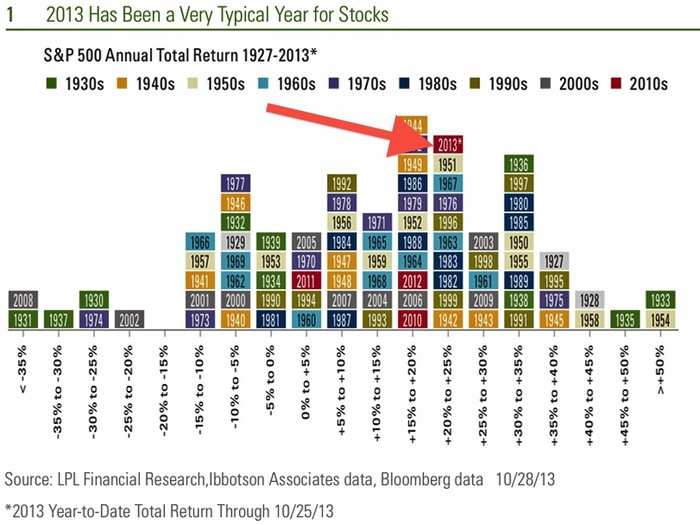

Stocks have delivered very typical 3-year average returns.

Even this year's huge rally is quite precedented.

"The annual total return of 20–25% this year is the second most common outcome for the stock market since records for the S&P 500 began in 1927. In fact, were it not for the recent gains in 2010 and 2012 boosting the number of occurrences that returns fell in the 15–20% range, the 20 – 25% range would be tied for the most common annual outcome for the stock market."

Source: LPL Financial

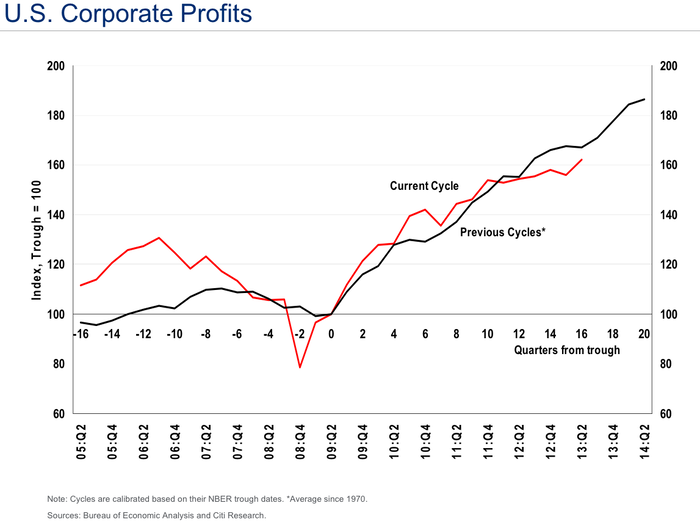

The impressive corporate profit recovery is quite average.

Source: Citi

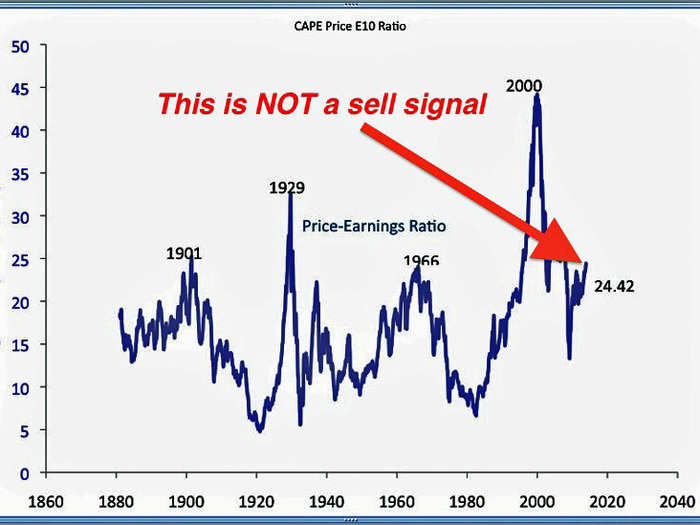

Stocks may look expensive relative to 10-year average earnings. But this is NOT signaling an imminent crash...

Robert Shiller, who popularized the CAPE method of measuring stocks again 10-year earnings, says CAPE should not be used to time crashes...

"I think the bottom line that we were giving – and maybe we didn’t stress or emphasize it enough – was that it’s continual. It’s not a timing mechanism, it doesn’t tell you – and I had the same mistake in my mind, to some extent — wait until it goes all the way down to a P/E of 7, or something.

"But actually, the lesson there is that if you combine that with a good market diversification algorithm, the important thing is that you never get completely in or completely out of stocks. The lower CAPE is, as it gradually gets lower, you gradually move more and more in. So taking that lesson now, CAPE is high, but it’s not super high. I think it looks like stocks should be a substantial part of a portfolio."

Source: Robert Shiller, Business Insider

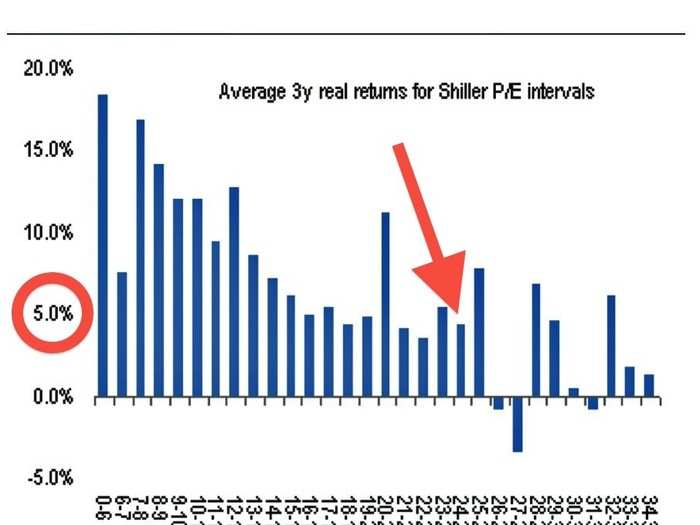

Stocks may fluctuate in the near-term, but CAPE only signals low single-digit average annual returns.

"We recognize that some investors are concerned that absolute valuations for US equities are at elevated levels. This is the certainly the case on the Shiller P/E. However, we find current multiples have not necessarily been a pre-cursor of falling markets. We note that markets are typically most vulnerable when the Shiller P/E is above 26x (compared to 24x currently)."

Source: Credit Suisse

Corporate cash levels are high, which means balance sheets are more liquid than ever. They also justify higher CAPE levels.

Source: Jefferies

Earnings growth estimates are being revised down this year, but that's what usually happens.

Source: Morgan Stanley

And relative to those earnings expectations, the PE multiple says valuations are below the 15-year average.

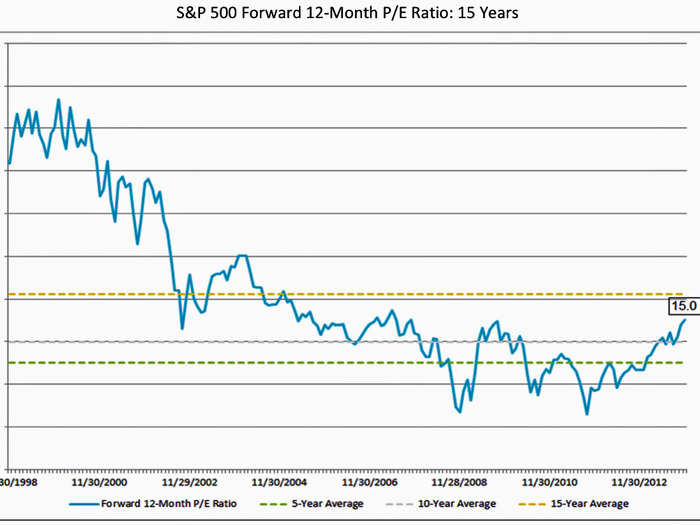

"...the current forward 12-month P/E ratio is still well below the 15-year average (16.2). During the first two to three years of this time frame (1998 – 2001), the P/E ratio was consistently above 20.0, peaking at around 25.0 at various points in time. With the forward P/E ratio still below the 15-year average and not close to the higher P/E ratios recorded in the early years of this period, one could argue that the index may still be undervalued."

Source: FactSet

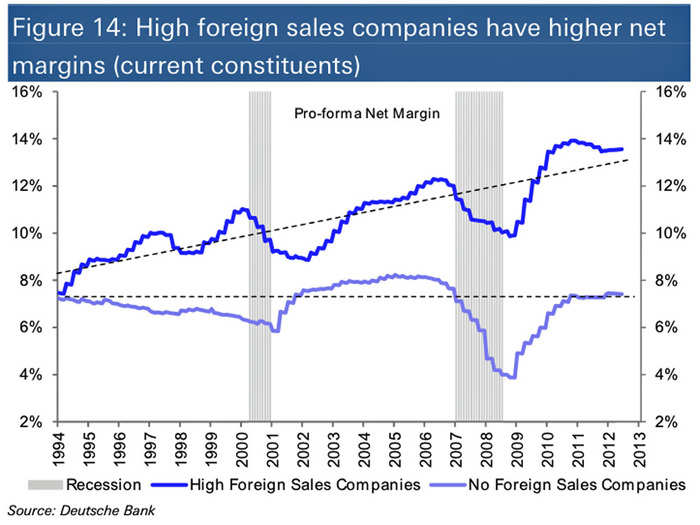

Profit margins are high and susceptible to cyclical swings. But they are on a sustainable long-term upward trend...

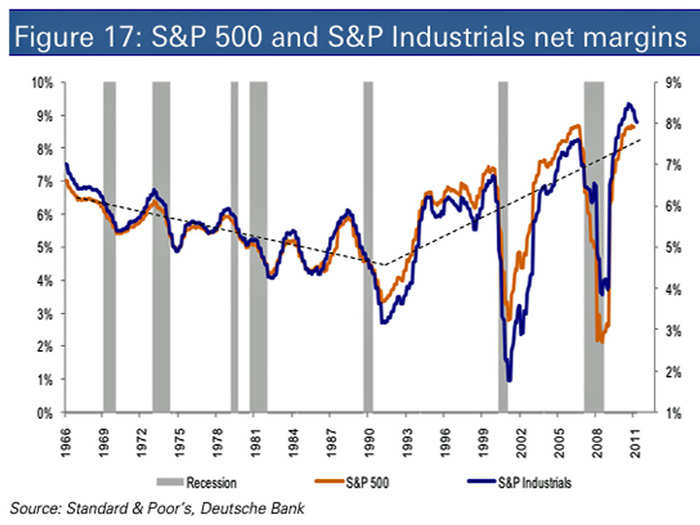

Much of the margin gains are due to increased overseas exposure were costs and taxes are lower.

Source: Deutsche Bank

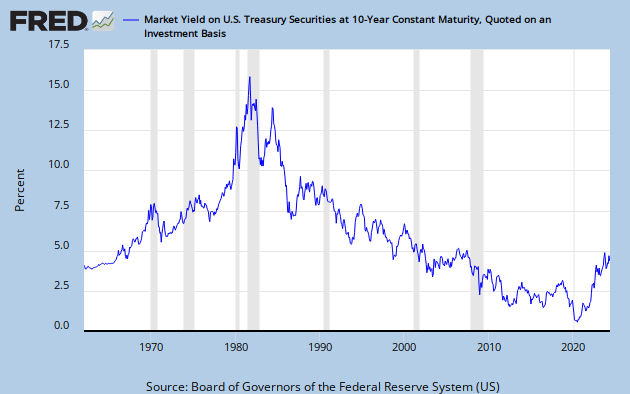

And lower debt levels will blunt the impact of rising rates.

"Even more compelling - and we believe supportive of equities in an eventually rising interest rate environment (UBS' Year End 2014 10 year interest rate forecast is 3.2% vs. the current 2.75%) once the Fed is satisfied that 3% growth is achievable – is the elevated level of Total Yield less the interest rate on the US 10 year Treasury."

Source: UBS

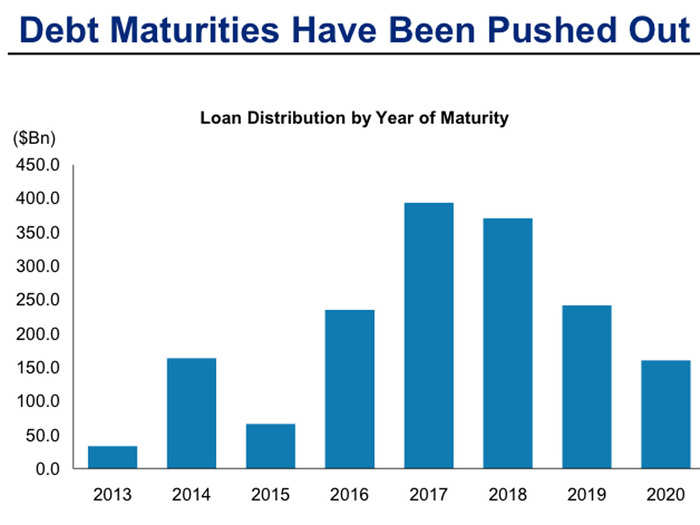

And due to aggressive refinancing at current low rates, it'll be years before we should be concerned about rates raising interest expenses.

Source: Morgan Stanley, RBC Capital

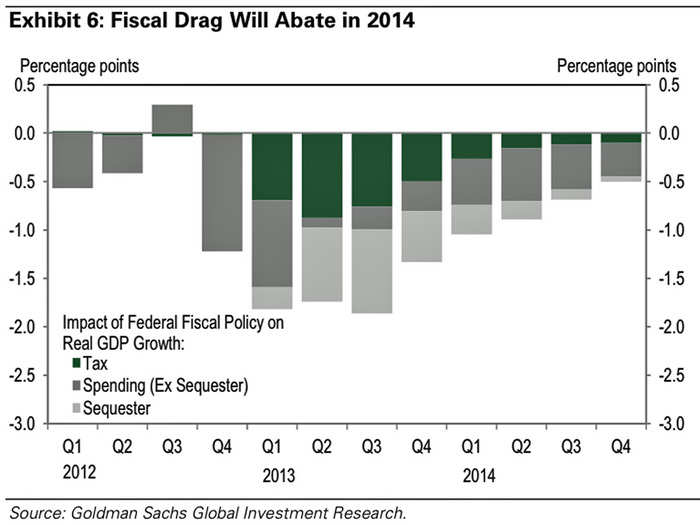

Government demand will be boosted by a waning fiscal drag.

"The estimates of fiscal drag that underlie our economic forecast assume full sequestration in 2014. Removing sequestration for one year would increase federal outlays by around $80bn (0.5% of GDP) in CY 2014."

Source: Goldman Sachs

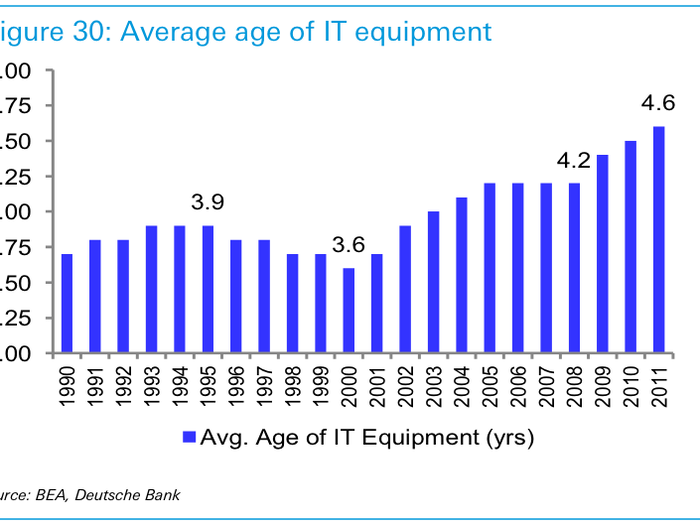

Corporate demand will be fueled by the need to replace old equipment.

"Corporate IT spending has been sluggish since 2010. Most of IT spending is productivity enhancing and stepped up tech spending in the late 1990s was a key driver of strong productivity growth. We think aging IT equipment and companies outsourcing their IT infrastructure to produce savings will boost IT enterprise spending. Global semiconductor sales increasing to its highest level in 3 years in September is encouraging."

Source: Deutsche Bank

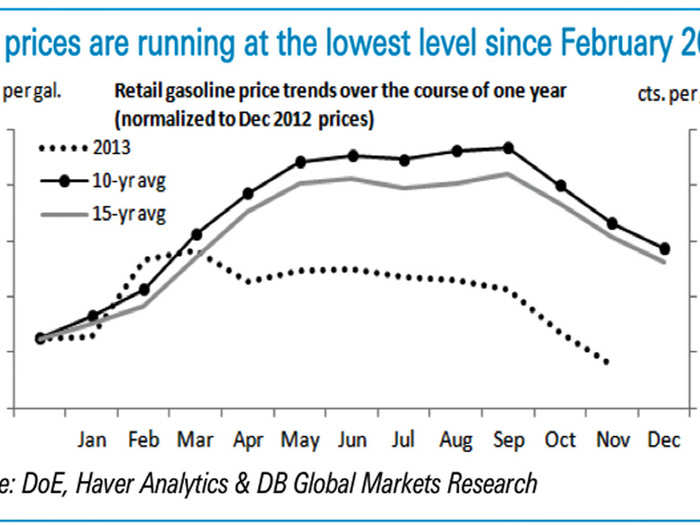

Consumer demand will get a nice boost thanks to falling gas prices.

"A one cent change in gasoline prices reduces annual household consumption by roughly $1 billion. At present, gasoline prices are down -$0.26 compared to a year earlier, although the rolling 26-week average is down by a lesser -$0.12. Thus, based on the aforementioned rule of thumb, the resulting economic stimulus from lower gasoline prices is relatively mild (in the range of $12 to $26 billion)." —Carl Riccadonna

Source: Deutsche Bank

The fact that bulls are warning of a correction actually reduces the odds of a correction.

"Despite the hurdles from valuation, sentiment and even technicals, one of the problems for the bears is that everyone seems to acknowledge that we are due for a correction. Even the bulls are anticipating one — hoping for one, in fact, in the name of a pause that refreshes (keep that powder dry)."

Furthermore, all of the stock market doomers are actually predicting stocks will go... up!

John Hussman: "...we should neither expect, rely or be shocked by a further blowoff..."

Jeremy Grantham, GMO: "My personal guess is that the U.S. market, especially the non-blue chips, will work its way higher, perhaps by 20% to 30% in the next year or, more likely, two years..."

Richard Russell: "I continue to think that this bull market will end in an upside explosion."

Bob Janjuah, Nomura: "I still see end Q4 2013, through to end Q1 2014, as the window in which we see a significant risk-on top before giving way, over the last three quarters of 2014 and through 2015, to what could be a 25% to 50% sell-off in global stock markets."

The Stock Market Is Not Doomed To Crash - Here's The Full Argument Why

{kind=link}

Popular Right Now

Popular Keywords

Advertisement