Zomato is now bigger than Paytm — reasons why the market is not excited about Vijay Shekhar Sharma’s vision of a superapp

Nov 18, 2021, 17:26 IST

- Zomato had a higher market cap than One97 Communications, the listed parent of the digital payments giant Paytm.

- Part of the sell-off in Paytm shares could also be a reflection of the market mood.

- But, there is a lot more that the street is worried about.

- Founder Vijay Shekhar Sharma wants the market to be excited about Paytm as a superapp but many others have argued that a smartphone itself is a super app.

- Check out the latest news and updates on Business Insider.

Advertisement

Two of India’s most-awaited tech IPOs, that of Zomato and Paytm, came with a lot of anxiety around the price at which the shares were being sold to the first lot of public investors. Zomato still made some money for those who got the shares in the initial public offering (IPO) but those who got shares in the Paytm IPO have lost 27% on the opening day. By noon, Zomato had a higher market cap than One97 Communications, the listed parent of the digital payments giant Paytm. The overall market mood played a role in pushing down Paytm’s share price, Deven Choksey, managing director of KR Choksey Shares and Securities, told Business Insider. The sell-off seen earlier in the week intensified on Thursday (the day of Paytm’s market Debut) and 42 out of the Nifty 50 stocks were in the red. But that’s not the only reason why people sold Paytm shares.

| Company | Valuation pre-IPO | Valution sought in IPO | Market cap, as on November 18 |

| Zomato | $5.8 billion | $8.1 billion | ₹1,21,731 crore ($16.3 billion) |

| Paytm | $16 billion | $19.9 billion | ₹1,01,399 crore ($13.6 billion) |

It’s not that Paytm's advisors didn't see it coming. According to a Bloomberg report published in October, Paytm was advised to go for a lower valuation than $20 billion in its pre-IPO round but the company decided to skip the round altogether. Even stock brokerage firm Macquarie had given Paytm a with an underperform rating, and projected that the stock may fall to as much as ₹1,200 (compared to an issue price of ₹2,150) any time in the next one year .

Interestingly, Paytm was the highest valued Indian startup between 2019 to me this year. The company got a valuation of $19.9 billion in its public issue. The only smile that Paytm believers could steal was thanks to the meme fest on Twitter.

Advertisement

The drop in Paytm’s share price led to a fall of the stock market. “Today’s fall in the market is also largely due to collateral damage, Paytm loss to investors,” Deven Choksey, managing director of KRChoksey Shares and Securities said.

Manoj Dalmia, founder and director of Proficient Equities Private Limited also highlighted three reasons behind Paytm’s weak listing on the stock exchange. The issue ranges from high valuation to intense competition.

These are some of the issues pointed out by Manoj Dalmia of Proficient Equities, Scenes by Avalon’s Shashank Udupa, TaxationHelp.in’s Neha Nagar

| Issue | Reason |

| Overvaluation | The company is overvalued at a Price to Sales (P/S) value of 26 compared to its global peers, who have a P/S of 0.3-0.5 |

| Limited promoters in India | Nearly 75% of the promoters of Paytm are from other countries and are selling shares worth ₹10,000 crore, which is more than 50% of the issue. |

| Not a market leader | Paytm is not a market leader in any business it operates in. |

| Analyst rating | Falling grey market premium and Macquarie's downrating has pushed the stock into a downward momentum. |

| Lack of focused business model | It is present in all over the Fintech space but not doing well in any of them while the competition is rising from players like Google, Amazon, PhonePe. |

Dalmia is not alone in his pessimism around Paytm’s near-term prospects. “Dabbling in multiple business lines inhibits PayTM from being a category leader in any business except wallets, which are becoming inconsequential with the meteoric rise in UPI payments. Competition and regulation will drive down unit economics and/or growth prospects in the medium term in our view,” Macquarie Research analysts Suresh Ganapathy and Param Subramanian said.

Advertisement

ALSO WATCH: Even the biggest of conglomerates find it difficult to do more than two things right, market expert Saurabh Mukherjea told Business Insider. Paytm is one of the biggest digital payments companies in India with offerings across several digital modes of payments like unified payments interface (UPI), credit and debit cards payments. It also offers wealth management solutions through Paytm Money and banking services through Paytm Payments Banks.The company has 333 million total customers, 114 million annual transacting users and 21 million registered merchants.

Paytm has a strong market share in digital payments via the unified payments interface (UPI) but the margin is zero in peer-to-peer payments and wafer thin when merchants get paid.

In the personal finance space — where Paytm sells mutual funds, gold and stocks — it has a less than 1% market share and makes zero commission, according to Macquarie. In insurance, only one out of 100 policies are sold online and Paytm is pitted against an early bird like Policybazaar as well as legacy banks, which dominate the space.

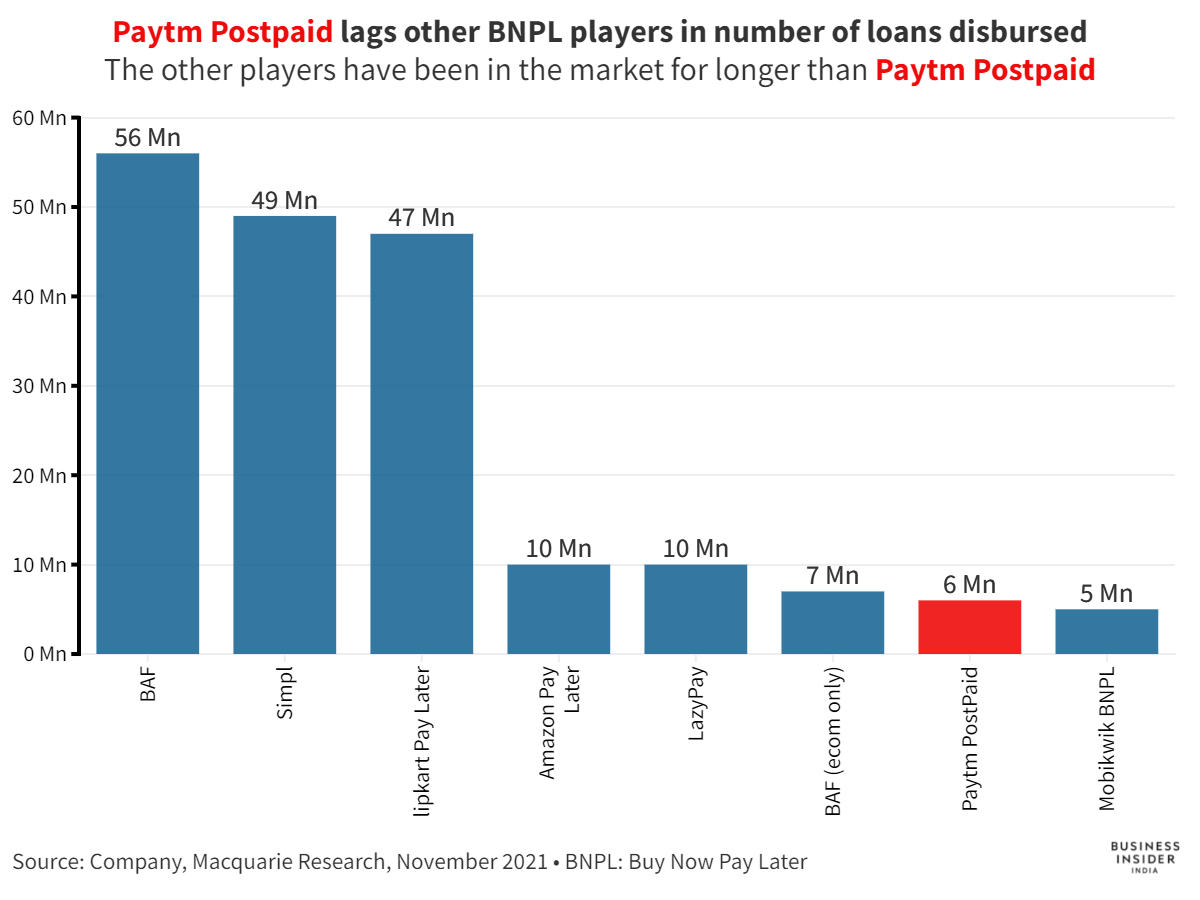

Paytm aims to make money from its lending business. “Since Paytm will largely be engaged in selling down these loans to partner banks or NBFCs (non-banking financial companies) balance sheets, the addressable fee pool is much lower,” said Macquarie, which pegged the potential market for buy now, pay later schemes to be anywhere between $45 billion and $50 billion by March 2026.

Advertisement

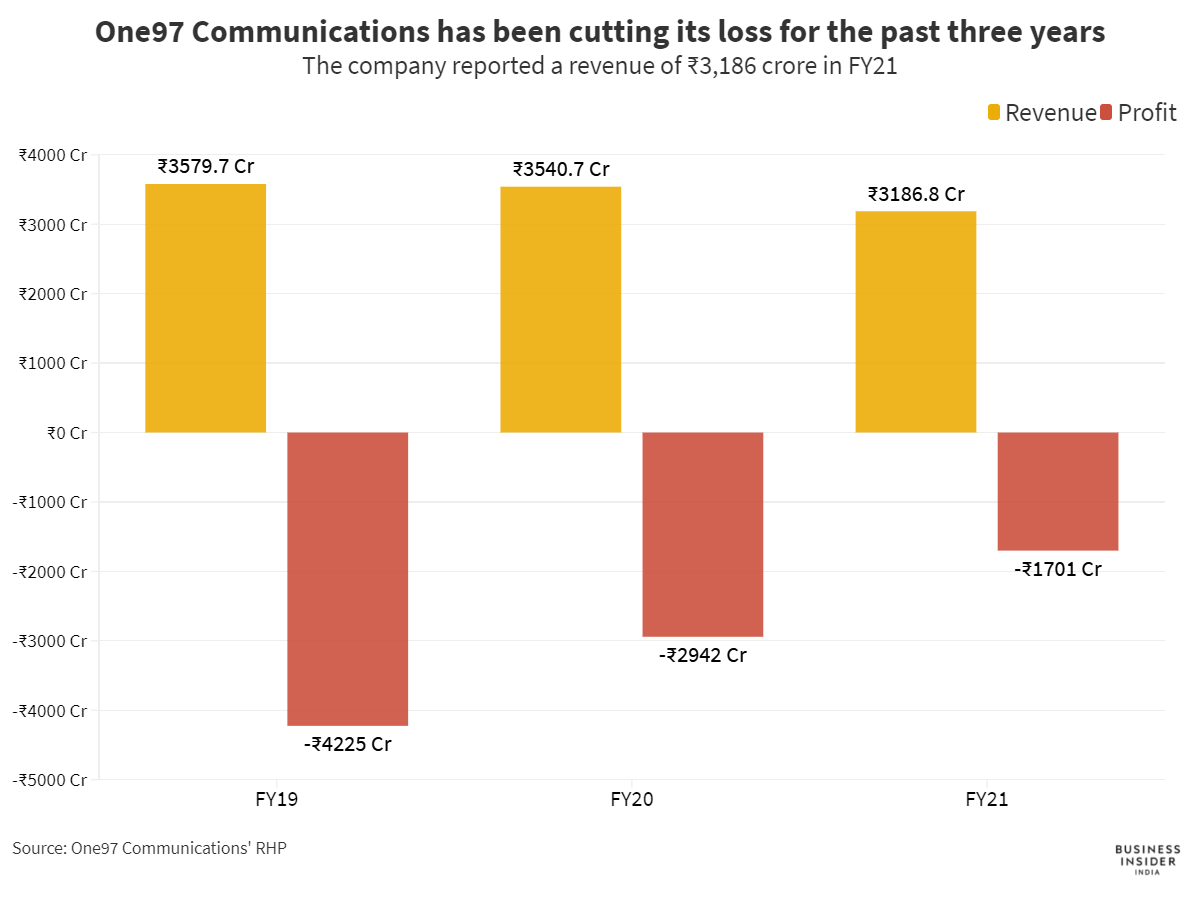

Despite a massive user base, the company’s revenue has been marginally declining on a year-on-year (YoY) basis. The company reported a revenue of ₹3,186 crore, with net loss of ₹1,761 crore. “Loss-making businesses will find it hard to sustain premium valuations,” Choksey added.

Ravi Singh, head of research and vice president at ShareIndia, noted that Paytm’s future growth is a key to watch for long term investors. “We advise the investors after looking at the overall valuations and earlier losses of Paytm, to book their positions and wait for 1700-1600 levels for fresh investment. Retail investors may remain cautious as the overall market is in profit booking zone pushing maximum stocks in downside territory,” he added.

“People ask me how do you raise money at such a high price? I say, I don’t raise money on a price but I raise money on a purpose,” founder and chief executive officer Vijay Shekhar Sharma. He wanted India to be as excited about his dream of a super app for anything that can be bought and sold online.

But many others have argued that a smartphone itself is a super app. Another startup founder Kavin Mittal, the man behind the $1.4 billion Hike Messenger, had similar ambitions but found it to be a misguided goal and dropped the plan in January 2021.

Will Sharma prove his detractors wrong with Paytm? Only time will tell.

Advertisement

SEE ALSO:

India’s biggest IPO lists 9% below the IPO price and it may fall even further, warn analysts

Paytm is likely to list below IPO price and experts advice serious investors to wait a while before buying

ITC has a ₹2,500 crore IT business hiding in plain sight and that makes the street go Yippee!