YES Bank shares surge 5% as investors see a ray of hope after bank reported four fold growth in profit

Jul 26, 2021, 11:55 IST

- YES Bank has reported its highest quarterly net profit ever since December 2018 at ₹207 crore.

- Shares of YES Bank surged 5% as investors are cheering the company’s highest profit mark in recent times.

- However, analysts remain disappointed with the company on high stress loans and recommend a ‘sell’ rating on the stock.

Advertisement

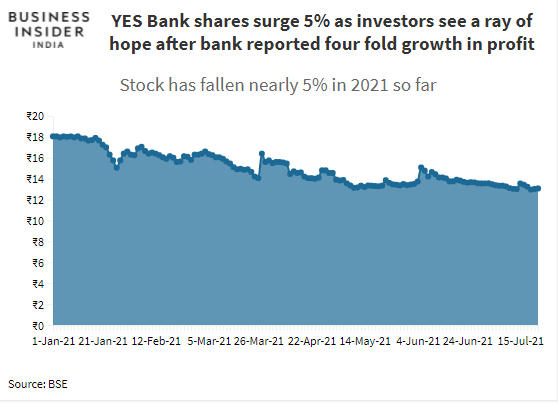

Shares of YES Bank surged 5% on July 26 as the private bank reported a four-fold jump in its net profit to ₹207 crore in June quarter compared to a profit of ₹45 crore the same time last year. This is the highest profit for the private bank since December 2018.While investors cheered YES Bank’s good profit growth in recent years, some analysts remain disappointed with the company on high stress loans and recommend a sell rating on the stock.

At 11:36 a.m., on July 26, shares of YES bank were trading 4.98% higher at 13.70 rupees.

The sudden jump in the lender’s profit is because of the lower provisions made for bad loans held with the bank. It has lowered provisions by 88% to ₹644 crore in June. The bank also expects the provision requirement to go down going ahead.

However, analysts studying the bank’s fundamentals and financials do not feel the same.

Advertisement

“While there is a significant improvement in earnings in Q1, profitability remains low with return on assets of 0.3%, and stress loans remain uncomfortably high at 29%... We expect credit cost to rise to 2.1% in FY23E [expected] as ageing provisions catch up,” said a report by Elara Capital while recommending a ‘sell’ rating on the stock.

Meanwhile, analysts at Kotak Institutional Equities believe that earnings are far too volatile given the impact slippages have on interest income (NII) and provisions. The bank’s capital position is above regulatory requirements, but the flexibility to make higher provisions is quite limited, said the report while maintaining a ‘sell’ rating on the stock.

SEE ALSO: YES Bank’s net profit grows four fold as provision for bad loans shrink

A Wharton MBA grad and a former GSK exec’s healthcare startup raises $3 million to reach more PCOS patients