JPMorgan lists 6 reasons why they're bullish on stocks right now

Matthew Fox

- JPMorgan said there are six reasons stocks and risk-on securities are in a bullish environment since the March 23 low, according to an analyst note published Tuesday afternoon.

- The bank said that liquidity injections, low bond yields, investors being underweight equities, the defensive nature of the current market rally, the quick healing of credit markets, and the relaxation of lockdowns are all reasons to be bullish on stocks right now.

- JPMorgan has taken a bullish stance on stocks since mid-March.

- Visit Business Insider's homepage for more stories.

JPMorgan is bullish on stocks right now, and listed its six reasons why in a note published Tuesday afternoon.

The bank has been bullish on stocks since mid-March and thinks the current bullish environment can continue.

Since its March 23 low, the S&P 500 index has rallied nearly 30%.

From low bond yields to the relaxation of lockdown restrictions, here are JPMorgan's six reasons for being bullish on equities.

Read the original article on Business Insider6. "The rapid healing of credit markets"

JPMorgan has observed a "rapid healing" in credit markets via a recovery in credit spreads, and via a normalization in issuance. This has occurred much faster than after the Lehman Brothers collapse practically shut down credit markets overnight in 2008.

"In turn, the rapid normalization in corporate bond issuance should help reduce the severity of the current default cycle ... thus making the current economic contraction rather short lived," the bank said.

5. "The relaxation of lockdowns and signs of bottoming out in economic expectations"

JPMorgan said that economic normalization has begun as regions across the globe begin to relax lockdown restrictions that have shut down economies to help limit the spread of the novel coronavirus.

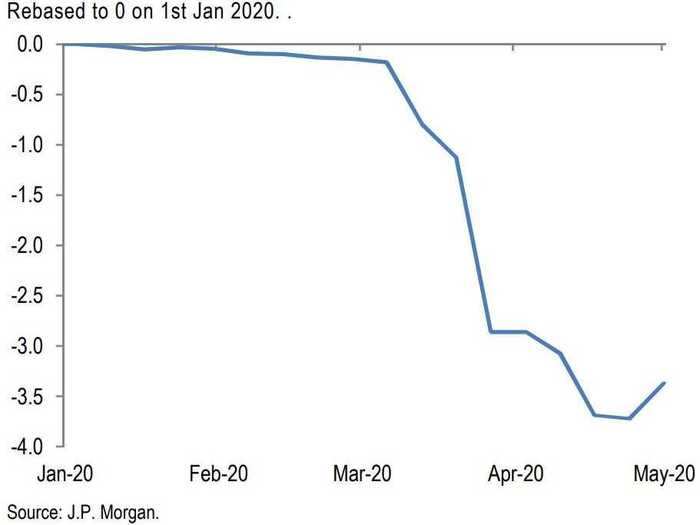

Additionally, the bank said, "the recent collapse in economists' expectations about GDP appears to be behind us as shown by the nascent recovery in our Global Forecast Revision Index."

The Global Forecast Revision Index measures the cumulative weekly changes in GDP forecasts for the current quarter.

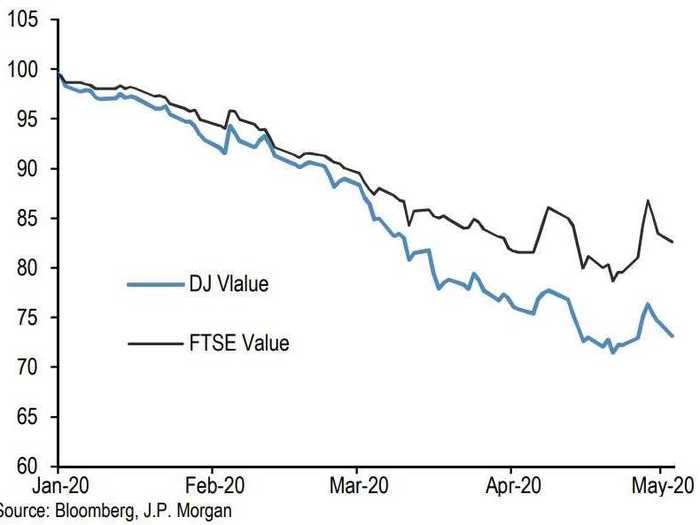

4. "The defensive nature of the risky market rally so far"

JPMorgan said that the global rally in equities since the March 23 bottom has been defensive in nature, with little participation by value stocks.

"Markets are still pricing in weak economic recovery as evidenced by still depressed dividend futures prices in equities and high credit spreads in HG and HY (which are still close to recession levels)," JPMorgan said.

The bank added that the equity market rally has been driven more by discount rate compression than high growth expectations over the past few weeks.

With such a wall of worry still in place, equities have more room to run as economic concerns slowly subside as a recovery takes shape, JPMorgan said.

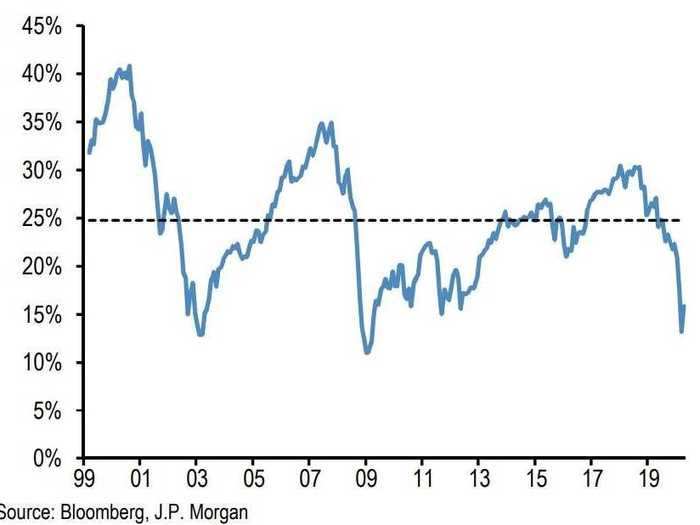

3. "The presence of an equity short base and equity underweights among investors"

When looking at fund flows, JPMorgan said that short covering is responsible for driving much of the recent market rally, and there's still more room left for this rally to continue.

According to the bank, there are three main fund flow forces: short covering, rebalancing portfolios, and volatility normalization.

Short covering occurs when bearish investors who short the market close their position by buying it back.

Rebalancing portfolios occurs when investors who are overweight bonds in their portfolio due to market moves will sell bonds and buy equities to get their portfolio back to its target allocation.

Volatility normalization includes risk parity funds that raise their equity exposure as market volatility calms down.

"In our mind the short covering force is likely done by around 50%, the rebalancing force is likely done by around 85%, and the volatility normalization force is likely done by around 70%," JPMorgan said.

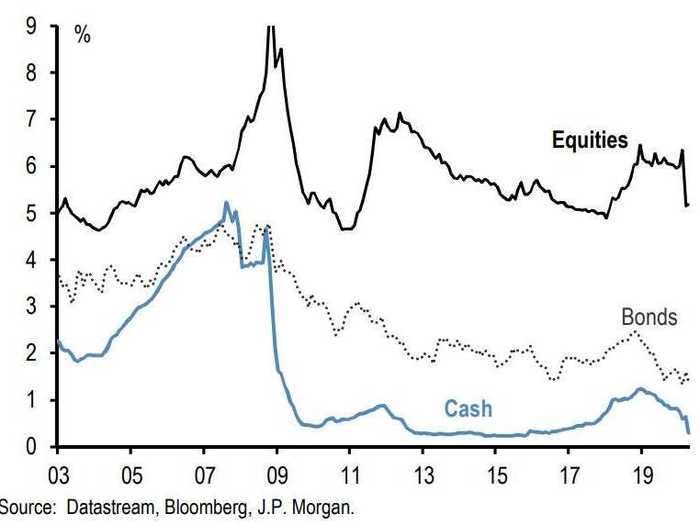

2. "Zero cash rates and low bond yields"

In other words: TINA, aka, There Is No Alternative.

JPMorgan said that with cash yielding close to zero for the foreseeable future, "there would be no other place for these cash balances to go than chasing equities and bonds in the world as the need for precautionary savings subsides over time."

JPMorgan argued that even when accounting for dividend and buyback declines caused by the global pandemic, equities offer superior yields over bonds and cash.

"To be conservative for equities we incorporate sustained divided cuts as implied by 2022 dividend futures and a sustained 25% decline in buybacks. Even after these conservative adjustments, we find that global equities offer higher than 5% yield, which compares to 1% for global bonds and close to 0% for cash," the bank said.

1. "Massive liquidity injections"

JPMorgan highlights the massive liquidity injections happening across the globe in response to the coronavirus pandemic, in the form of central bank balance sheet expansion and bank lending.

"We expect that global cash balances outside the banking system will likely expand by 20%, or 17% over the coming year, similar to the post Lehman experience," the bank said.

The bank added that so far, the US has experienced $2.4 trillion in cash expansion, which suggests that "we are only at the beginning of this process, with less than a fifth of the projected global cash injection having taken place so far."

READ MORE ARTICLES ON

Popular Right Now

Popular Keywords

Advertisement