Investing in Square today is like buying JPMorgan in 1871 as the payment company's Cash App realizes its growth potential, Mizuho says

- Buying shares of Square today is like investing in JPMorgan at its founding in 1871, Mizuho said in a note on Thursday.

- Mizuho believes Square's Cash App will become the ultimate neo-bank and money center bank of the future.

- The firm rates Square as a "Buy" with a $380 price target, representing potential upside of 59%.

- Sign up here for our daily newsletter, 10 Things Before the Opening Bell.

Square's Cash App has so much upside potential that buying shares in the fintech company today is anagolous to investing in JPMorgan at its founding in 1871, Mizuho analyst Dan Dolev said in a note on Thursday.

"We believe Cash App may be en route to becoming the ultimate neo-bank and the money center bank of the future," Dolev said.

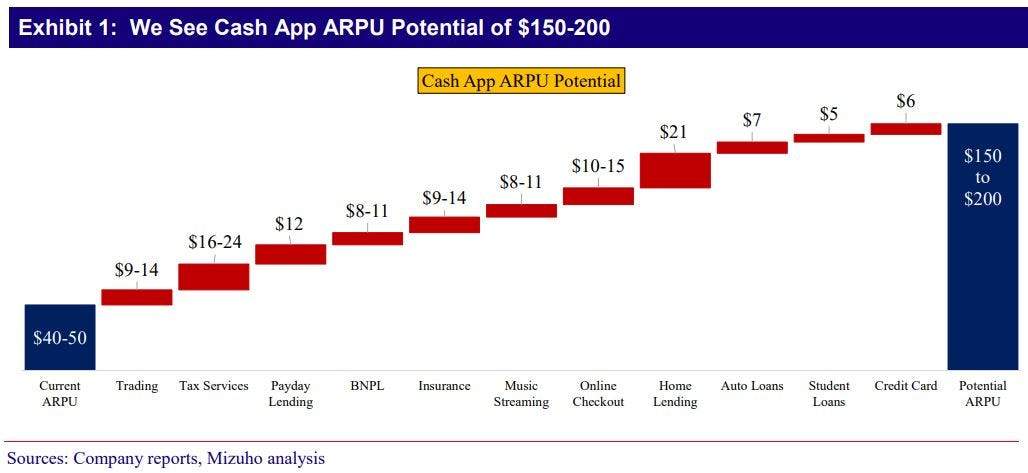

The firm sees a visible path for Cash App products to more than quintuple its average revenue per user to $200, and estimates the money sending app can capture a large portion of the US bank account total addressable market of 400 to 500 million accounts, according to the note.

Dolev estimates that Square's Cash App currently has between 30 and 40 million users, and that legacy banks like JPMorgan and Wells Fargo generate average revenue per user between $400 and $700, implying lots of upside potential for Square's growth trajectory.

"With vast potential upside to average revenue per user and users, we believe Cash App's gross profit could see 4x-8x growth over the coming years," Dolev explained, adding that it views Cash App as the "ultimate challenger bank."

The product fronts Dolev expects Square to tackle (and dominate) over the coming years includes retail crypto and stock trading, buy-now-pay-later, insurance, mortgage and auto loans, and tax services, among others, according to the note.

While the comparison between Square and JPMorgan in 1871 makes for a good headline, it's worth noting that the predecessor to America's largest bank didn't go public until 1942.

Mizuho reiterated its "Buy" rating on Square and set a price target of $380, representing potential upside of 59% from Wednesday's close. Shares of Square were down about 1% in Thursday trades, and are up 8% year-to-date.