Ethos IPO — Either avoid or go long-term say analysts

May 19, 2022, 15:24 IST

- Ethos, a luxury watch retailer intends to raise ₹472 crore with the initial public offer of its shares.

- Analysts have mixed views about investing in Ethos’ shares because of moderate growth in financial performance, while some believe that valuations are attractive and the firm has potential for strong growth in the next three years.

- The grey market suggests a weak listing as shares of the company were trading at 10% discount to a higher price band of ₹878 per share.

Advertisement

On the second day of its subscription, the ₹472 crore IPO of luxury watch retailer Ethos was subscribed 32%. This lukewarm response has been captured by the many analyst views who believe the company can either provide long-term returns while a few suggested they skip it. Analysts at ICICI Securities assign an ‘avoid’ rating to the IPO as it says they “await consistency in improvement in profit metrics that the company has exhibited in recent quarters.”

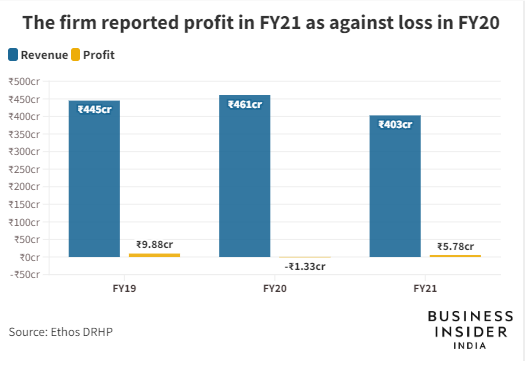

The luxury watch retailer made a profit of ₹5.78 crore in FY21 as against a loss of ₹1.33 crore in the previous year. However, its revenue has been declining for the last three fiscal years.

Good portfolio but the IPO view is ‘neutral’

The company has a portfolio of 50 premium and luxury watch brands including Omega, IWC Schaffhausen, Jaeger LeCoultre, Panerai, Bvlgari, Rado, Tissot, Raymond Weil and Balmain. Even those analysts who appreciated their portfolio are unconvinced about the returns it can provide.

“Ethos has strong brands and a wide range of products but we believe that these positives are captured in the valuations commanded by the company. Thus, we have a neutral rating on the issue,” said analysts at Angel One.

Advertisement

The grey market too suggests a weak listing as its shares were trading at 10% discount to a higher price band of ₹878 per share.

| Brokerage firms | Recommendation |

| Angel One | Neutral |

| ICICI Securities | Avoid |

| Nirmal Bang | Subscribe for long term |

| Hem Securities | Subscribe for long term |

A good ‘long’ term bet

The company has 50 outlets and it plans to launch 13 more in three years with new categories. A few analysts believe that it has good potential.

“We understand that the company is very small as compared to other listed retail players and focused on one category (currently), we believe that there is scope for growth in future,” said a report by Nirmal Bang.

Ethos not only has the highest revenue among its peers into multi brand outlets (MBOs), it is also the dominant market leader.

| Peers with multi brand outlets | FY20 revenue | Share in luxury watch market |

| Ethos | ₹457.8 crore | 20% |

| Kapoor Watch | ₹242.4 crore | 10% |

| Johnson Watch | ₹161.6 crore | 7% |

| Zimson | ₹150.5 crore | 6% |

| Kamal Watch | ₹111.2 crore | 5% |

| Khimani Watch | ₹55.9 crore | 2% |

| Helvetica Boutique | ₹35.7 crore | 2% |

The company has access to a large base of luxury customers. “It enjoys a leadership position in an attractive luxury watch market with early mover advantage in certified pre-owned business. Also Ethos being a founder-led company is supported by a professional management team. With strong growth prospects, we believe the company to be a candidate for long term investment purposes,” said a report by Hem Securities.

Advertisement

SEE ALSO: Heatwave has turned ACs from a luxury to a necessity — but margins remain muted for the players

Google Russia has no money to pay salaries to its 100 employees, heads for bankruptcy

Almost all — 92% — of Ladakh children suffer from anaemia and the rest of the country isn’t faring any better either