Bond market volatility is as high as it was in the 2008 financial crisis as the Fed accelerates the runoff of its $9 trillion balance sheet

- Volatility in the bond market has surged to levels seen during the 2008 Great Financial Crisis.

- The surge in volatility comes as the Fed accelerates the reduction of its $9 trillion balance sheet.

- Less liquid bond markets could spell trouble for equities, Ned Davis Research said.

Bond market volatility has hit levels seen during the 2008 Great Financial Crisis, and that volatility is starting to bleed into the stock market, according to Ned Davis Research.

In a Tuesday note, NDR highlighted how big of an impact the Fed's quantitative tightening program could have on asset prices as liquidity in the bond market continues to deteriorate.

The Federal Reserve has two big levers to pull in its bid to influence the economy and tame inflation, and while most investors are fixated on interest rate policy, the Fed's balance sheet plans can have an even bigger impact.

The Fed has committed to reducing its $9 trillion balance sheet, which mostly consists of US Treasury bonds and mortgage backed securities.

Fed Chairman Jerome Powell ramped up the purchases of US Treasurys, mortgage backed securities, and even corporate bonds during the height of the COVID-19 pandemic in an attempt to keep credit markets open when it was needed most.

The move worked, but in doing so the Fed's balance sheet ballooned from about $4 trillion before the pandemic to about $9 trillion today.

Now the Fed is on a path to unwinding those securities as the economy continues to regains its footing and recover from the pandemic. In September, the Fed boosted its monthly balance sheet runoff to $60 billion of Treasurys and $35 billion for mortgage backed securities, for a total of $95 billion per month.

If the Fed sticks with those monthly reduction plans, its balance sheet should decline by $1 trillion each in 2023 and 2024. But to get its holdings back to a pre-pandemic level of about 20% of GDP, as suggested by Fed Governor Chris Waller, NDR estimates the Fed would need to unwind $2.8 trillion of securities by April 2025.

Of course, such a reduction would have a big impact on both stock and bond markets – and in fact, it already is.

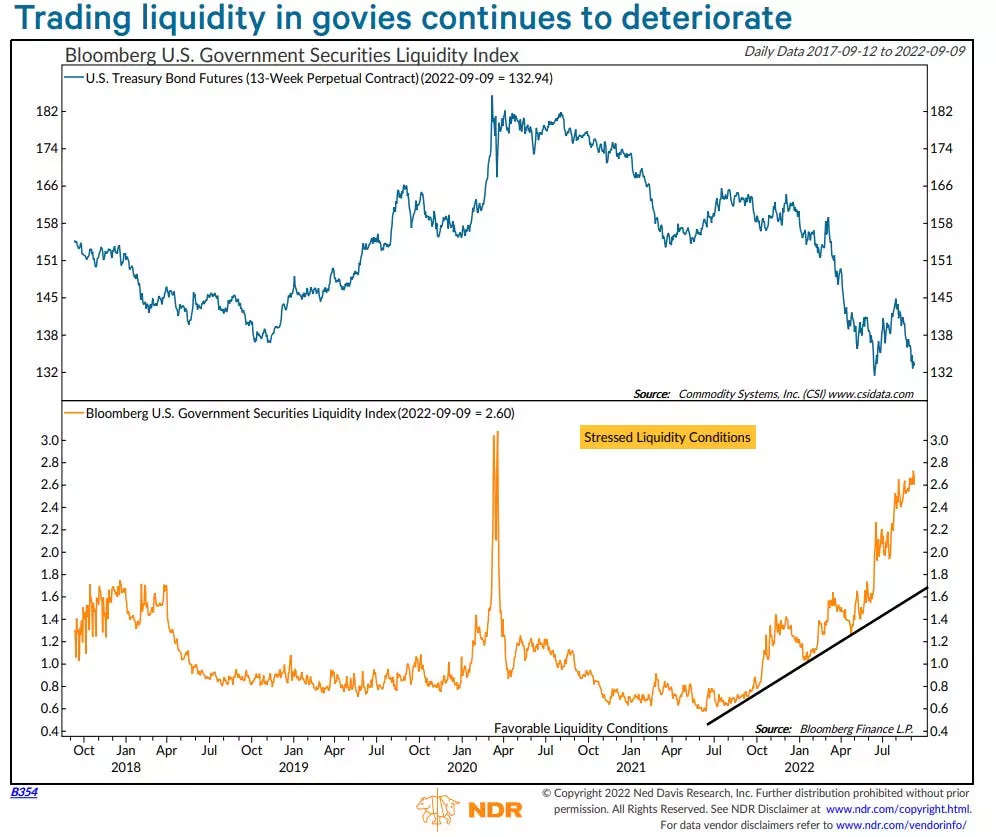

Trading liquidity in government bonds has declined significantly since the Fed unveiled its balance sheet reduction guidance in minutes released in April, as measured by the Bloomberg US Government Securities Liquidity index.

The index is currently showing "stressed liquidity conditions" and is already sitting at levels seen during the height of the COVID-19 pandemic in March 2020. What's worse is the liquidity deterioration in Treasurys is starting to spill over into the corporate bond market.

"The Fed may be creating different problems this time. Trading liquidity has been steadily getting worse all year and rivals the worst of the March 2020 period. Corporate distress has also risen," NDR said.

This has led to increased volatility in the bond market, and its beginning to bleed into the stock market, according to the note.

"Realized volatility is almost seven percentage points above its historical mean, while implied is nearly four points above its mean. You have to go back to the Great Financial Crisis and the European sovereign debt crisis to find comparable levels before the pandemic," NDR said.

There's no indication of how much quantitative tightening the bond and stock market will be able to handle, but NDR highlighted one indicator to monitor for potential problems.

"We want to monitor money market activity. Should the effective fed funds rate exceed the midpoint of the fed funds target range, it would indicate a tightening of financing conditions," NDR said.