HUSSMAN: The Stock Market Is In A Fragile Equilibrium

There is stable and there is unstable equilibrium in the financial markets.

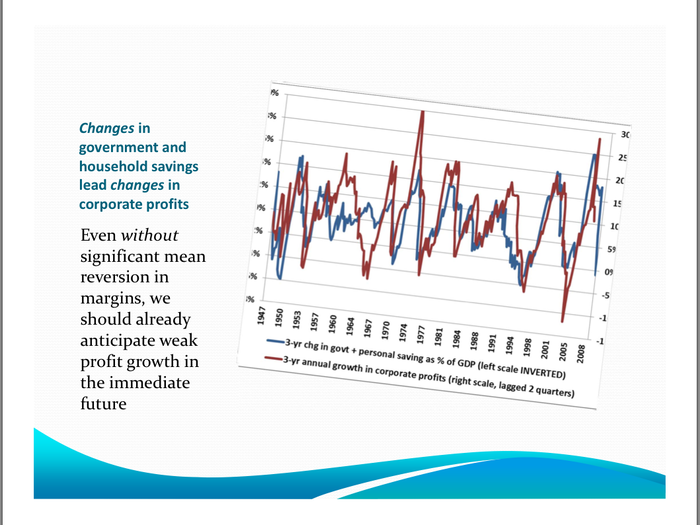

Here are the some basic insights into the equilibria listed in the previous slide.

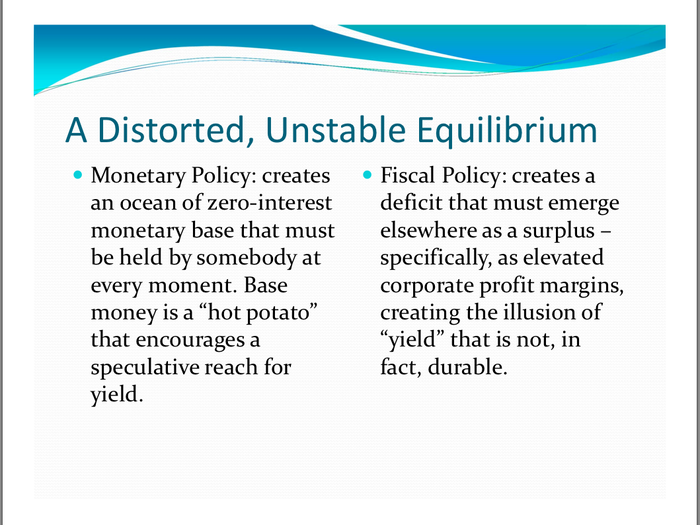

We can't just assume that an extra dollar of reserves will create $10 of spending without considering the economic issues that matter.

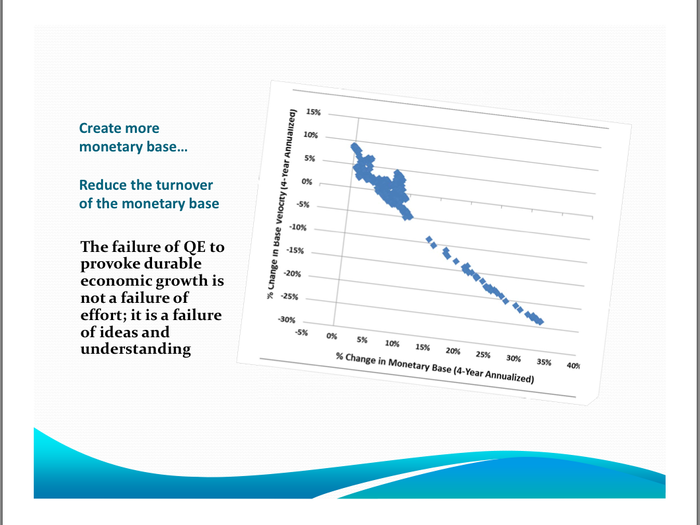

In the real world, when we increase the monetary base, it's turnover falls. This is why quantitative easing isn't' working.

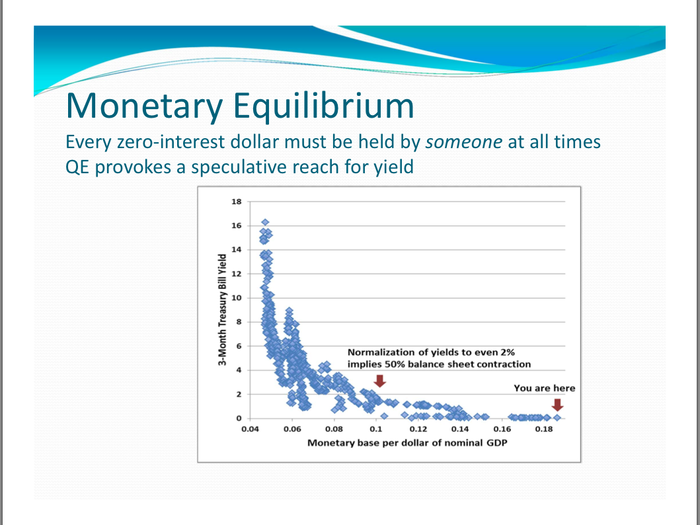

The fundamental purpose of quantitative easing is to provoke discomfort and a speculative reach for yield.

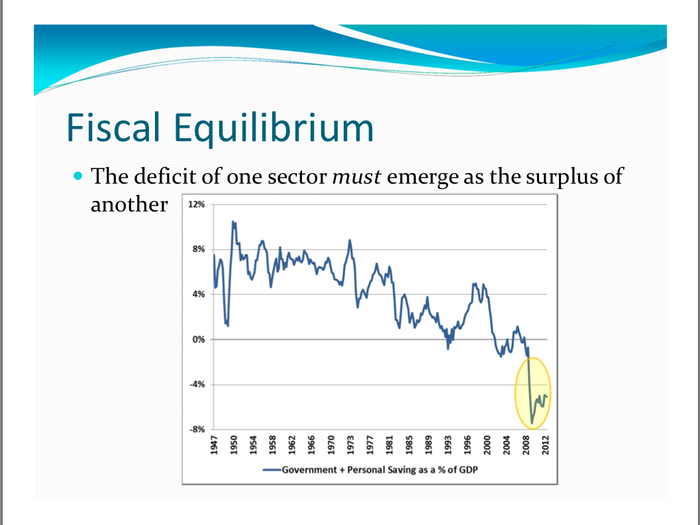

When government deficits rise, household savings fall.

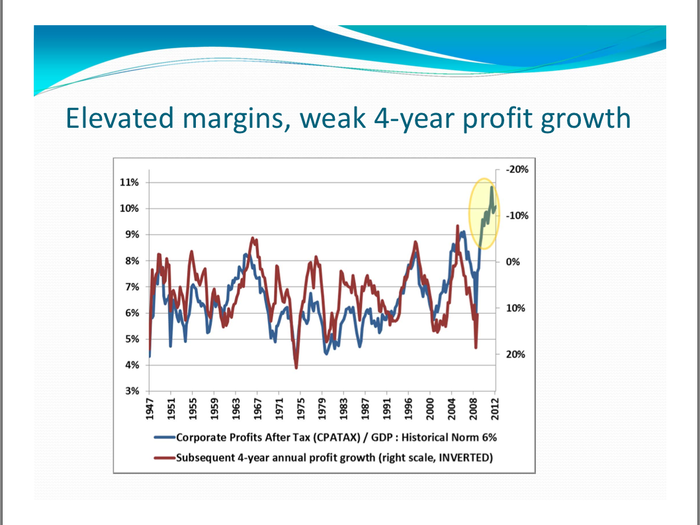

However, these huge profit margins come with a substantial drop in profit growth.

The record negative position in the government deficit and household savings equilibrium has forced corporate profitability to surge to a record high.

Current profit margins imply profit growth contraction at a 12% annual rate.

These distortions have encouraged investors to flock to the stock market where there is an illusion of high operating earnings yield.

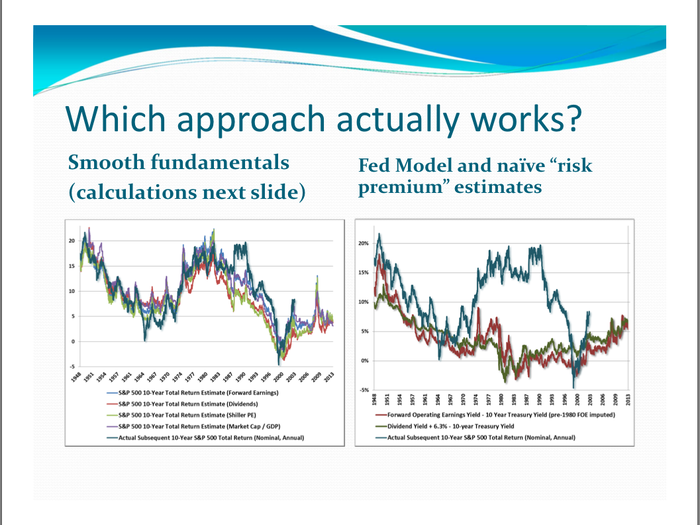

By many measures, the expected 10-year average total returns on stocks is near a very low 3.5%.

For your reference, here's how Hussman got to that low return estimate. In short, it assumes some reversion to the mean.

This fragile equilibrium that we're in because of monetary policy, because of fiscal policy, and because of the combination of yield-seeking plus the apperence of yield through forward operating earnings because profit margins are elevated -- this creates an environment where stock returns prospectively are very low.

Popular Right Now

Popular Keywords

Advertisement