At A Conference In Dubai, David Kotok Gave This Presentation On The Precarious State Of Global Monetary Policy

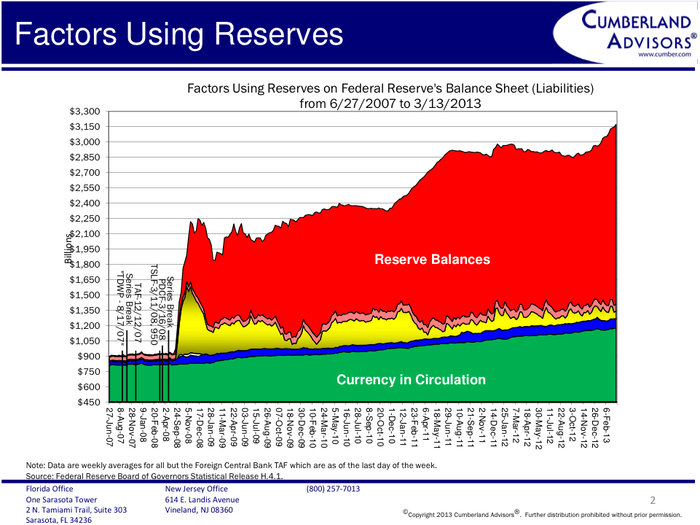

Notice that the size of the Fed’s balance sheet has grown from slightly over $900 billion before Lehman-AIG to approximately $3.2 trillion. The Fed continues to increase assets pursuant to its current policy.

The key to that slide is the green section labeled “Currency in Circulation,” which totals approximately $1 trillion. The red component is the excess reserves deposited at the Fed through the US banking system.

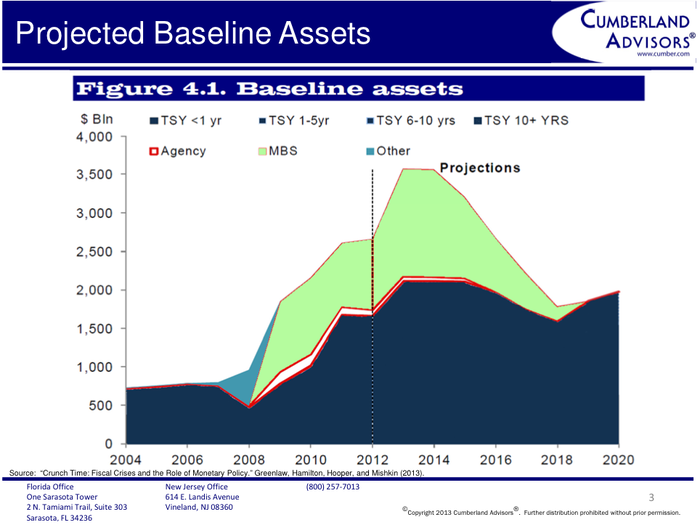

This shows 'the projected peaking of the Fed’s balance sheet at about $3.5 trillion and the gradual decline through 2020.'

From a 2013 special paper entitled “Crunch Time: Fiscal Crises in the Role of Monetary Policy,” by Greenlaw, Hamilton, Hooper, and Mishkin.

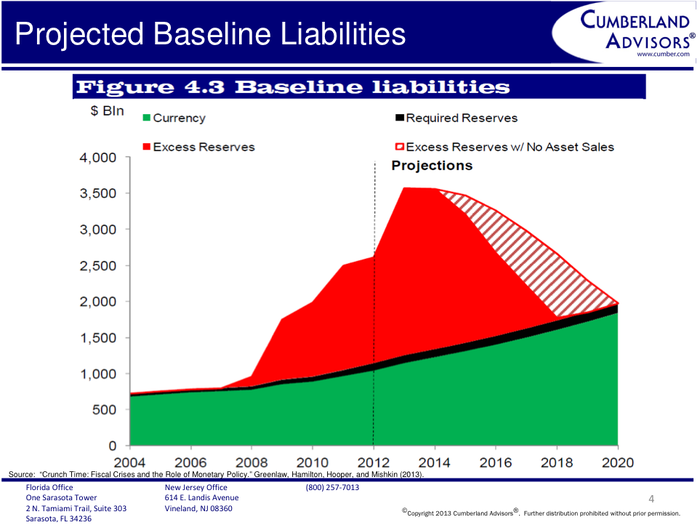

According to the authors’ projections, by 2020 the Fed’s mortgage backed paper will also have shrunk. The Fed will have permitted the excess reserve liability to run off as it reduces the asset side.

From a 2013 special paper entitled “Crunch Time: Fiscal Crises in the Role of Monetary Policy,” by Greenlaw, Hamilton, Hooper, and Mishkin.

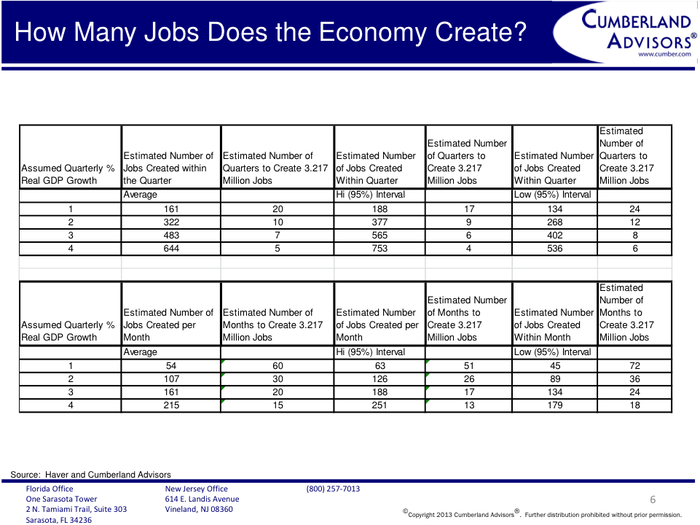

Here are 'simple assumptions to help us project the answer to the question: When will the unemployment rate hit 6.5 percent?'

Bob Eisenbeis used historical data in order to translate estimates of GDP growth into job-creation rates. The table projects job growth for both high- and low-confidence intervals.

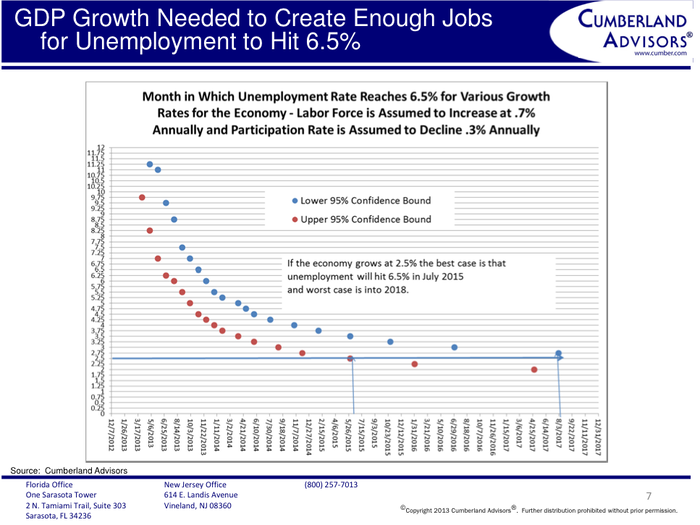

This show 'how much time it would take for the unemployment rate to fall to 6.5 percent, depending on GDP growth rate (vertical axis) and certain baseline assumptions.'

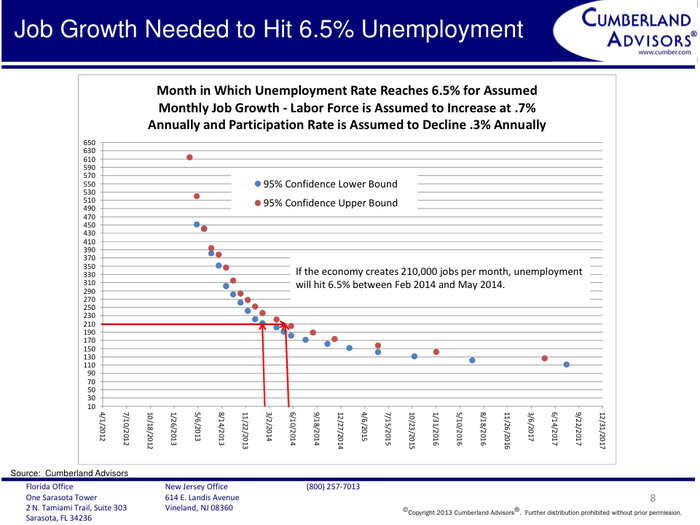

This 'shows the number of jobs the US economy needs to produce per month in order to hit a 6.5 percent unemployment rate.'

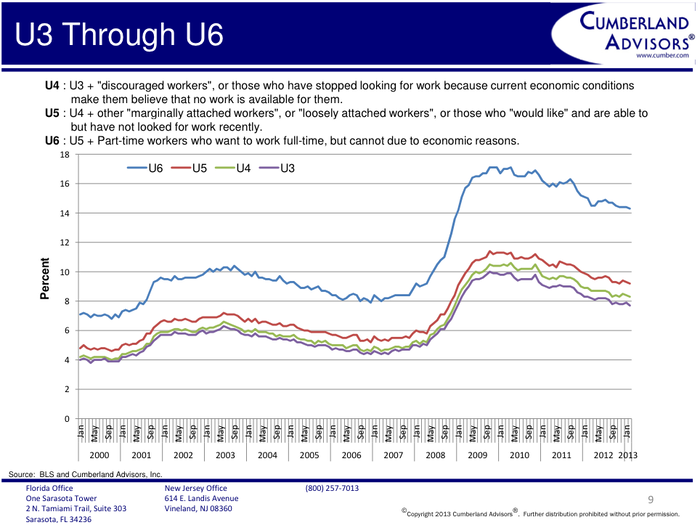

The Fed has selected the U3 unemployment rate for its 6.5 percent target. The parallel structure of these curves derives from the fact that these measures of unemployment are built one upon the next.

The labor force in the US comprises approximately 135 million people. Five to six million people fall into this category of part-time workers who cannot find full-time work. That is a huge overhang not addressed by the Fed’s policy of targeting 6.5 percent on the U3 measure of unemployment.

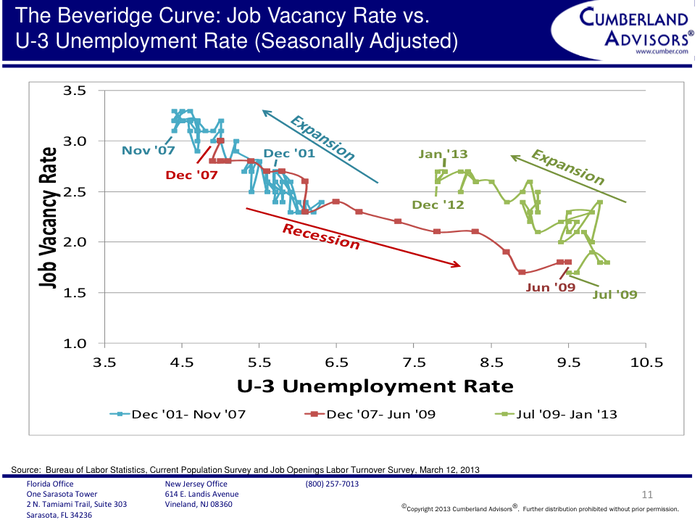

The curve tells you about the regime change that took place between the previous expansion, from December 2001 to November 2007 (shown in blue), and the present expansion (shown in green). The ’07-’09 recession is shown in red. The curve is created by taking the job vacancy rate and dividing it by the U3 unemployment rate.

"Beveridge curves tell you a lot about expansions and recessions and how difficult it is for recovery to take place in the labor force. Clearly, the recession was a regime change, according to these Beveridge curve calculations. The U3 unemployment rate is used in the curves on this slide. When you use the U6 unemployment rate, which the Fed is not doing, you find that the regime shift was actually much greater."

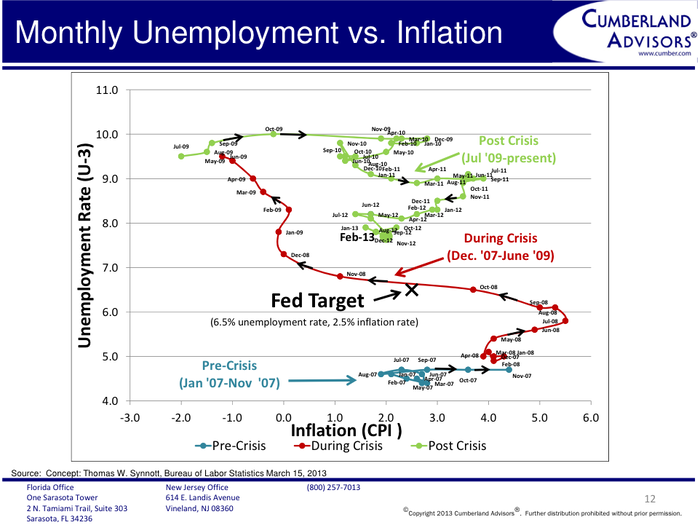

The idea is to show the difference in shifts in duration, slope, and composition of the Phillips curve... Clearly there is a large gap between the current situation, in February 2013, and the Fed’s targets of 6.5 percent for the U3 unemployment rate and 2.5 percent for the inflation rate.

This tracks "the Phillips curve, or inverse relationship between the unemployment rate and inflation rate. The concept was introduced to me by Thomas Synnott, a colleague at the National Business Economic Issues Council (NBEIC). Synnott uses the tracking system shown, with monthly data points. He describes it as an “under-damped oscillatory system.”"

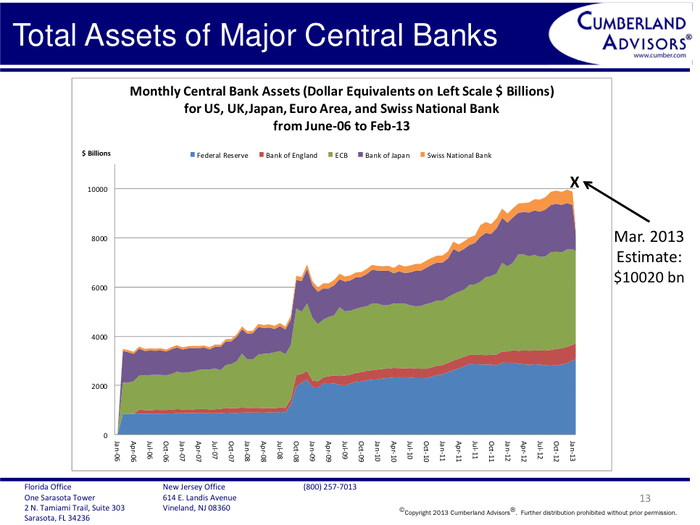

Essentially, these central banks started pre-crisis with about $3.5 trillion in total assets, in US dollar terms. Their assets now exceed $10 trillion and are growing.

For tracking purposes, here are the ECB's assets.

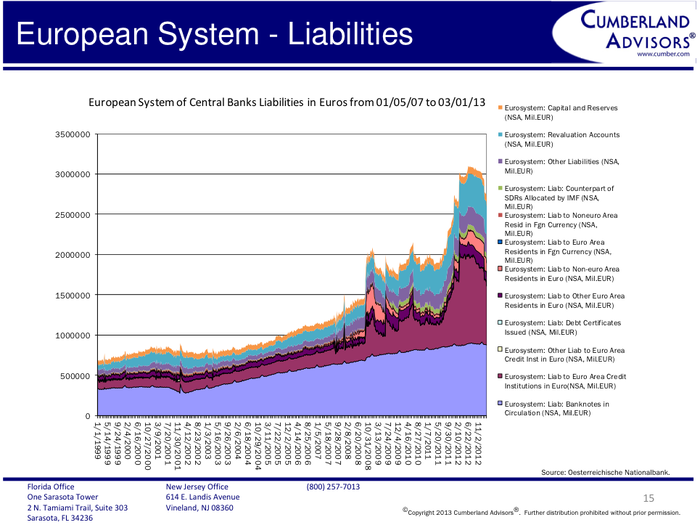

The ECB's liabilities

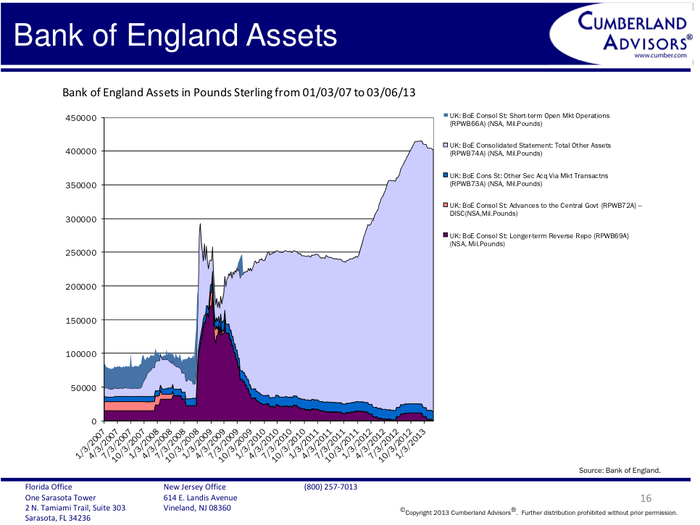

The BoE's assets

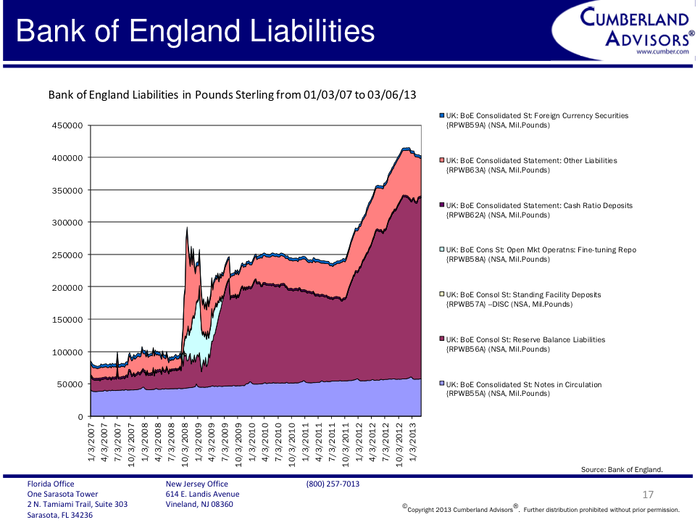

The BoE's liabilities

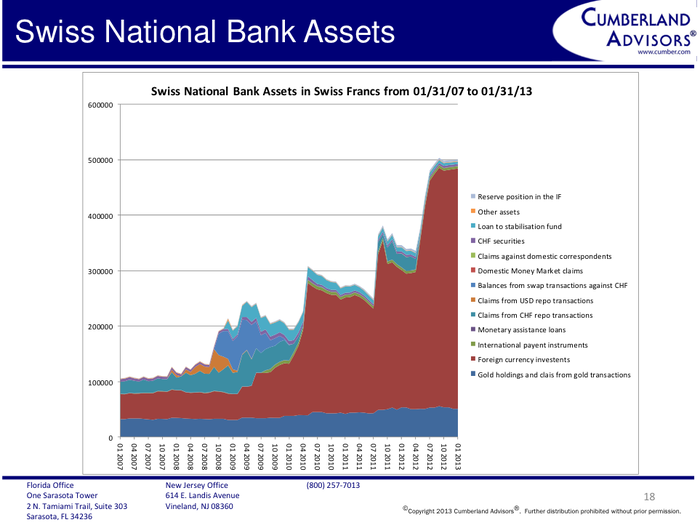

The SNB's assets

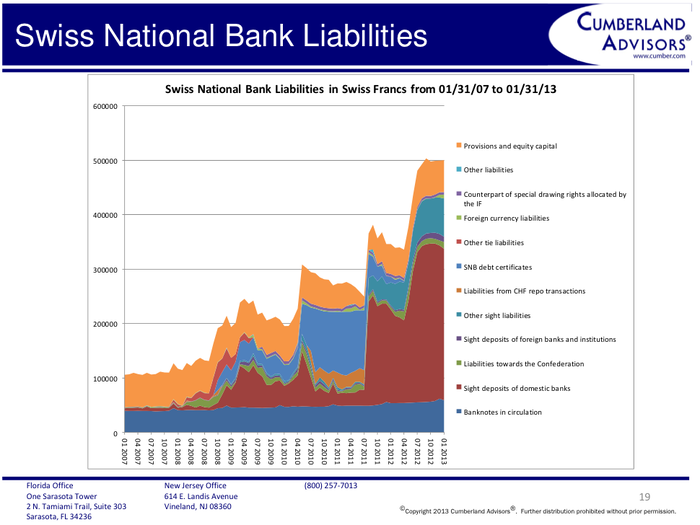

The SNB's liabilities

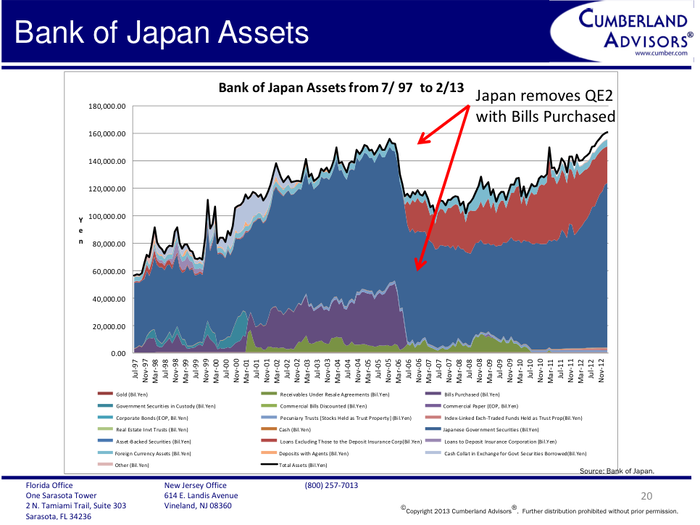

The BoJ's assets. 'Note that Japan is the only major country that has experienced extraction from quantitative easing. That happened in 2006.'

At the time, the Japanese quarter-end extraction shocked world markets quite seriously. This is the only case in modern history where a large extraction at quarter-end occurred.

All of this is completely unprecedented.

"We do not know how long this game of monetary quantitative easing will continue in the world. We do not know when it will stabilize. We do not know what will happen after that period, and we do not know how extraction will occur. What we do know is that world monetary affairs have never been in a situation like this before."

Another presentation you must see...

Popular Right Now

Popular Keywords

Advertisement