9 Formulas You Have To Know To Pass Wall Street's Hardest Exam

Capital Asset Pricing Model (CAPM): Attempts to explain the relationship excess market risk and expected return.

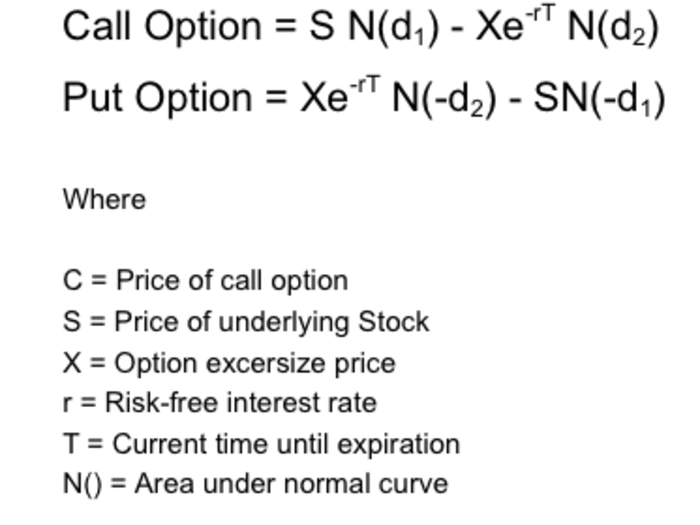

Black-Scholes Model: Applies theoretical physics when pricing options.

Source: Investopedia, Wikipedia

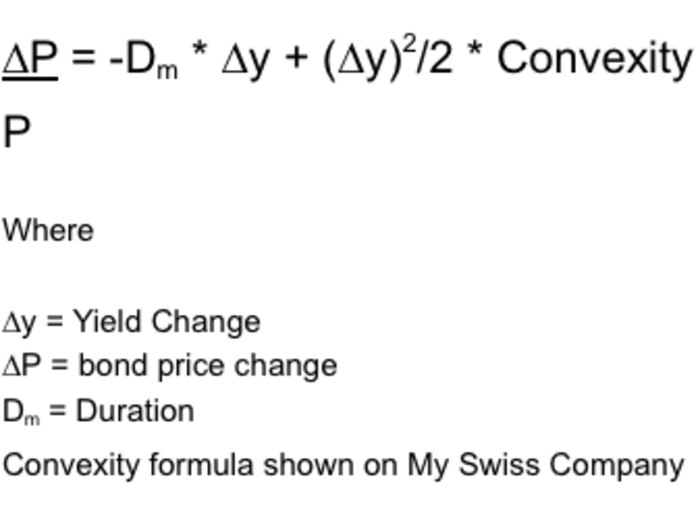

Duration With Convexity Adjustment: Duration is the average time until all cash flows from a bond are delivered. The convexity adjustment helps determine the change in price that is not explained by duration.

Source: Investopedia, My Swiss Company

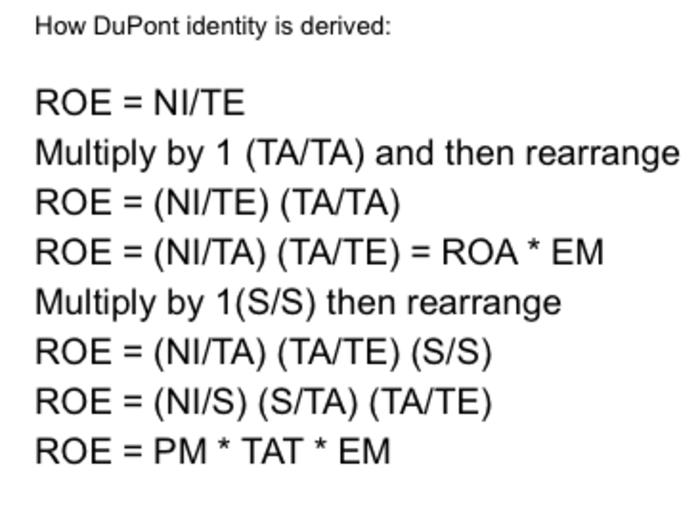

DuPont Identity Of Return On Equity (ROE): This breaks ROE into profit margin, total asset turnover, and financial leverage. It explains the operating efficiency, asset-use efficiency, and overall financial leverage of a company.

Source: Investopedia

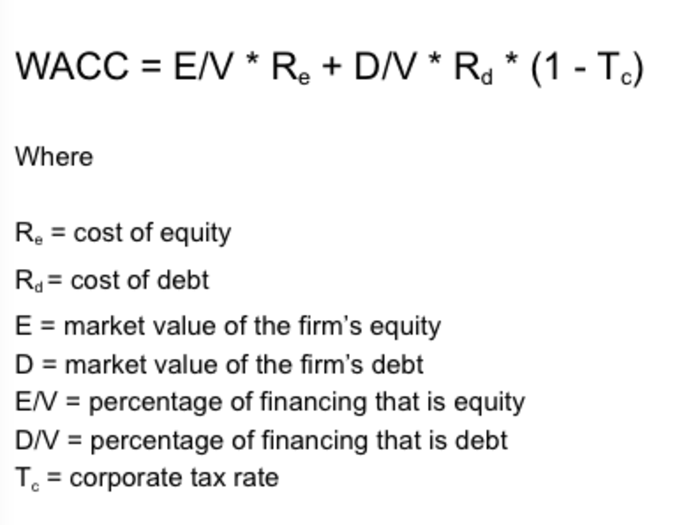

Weighted Average Cost of Capital (WACC): The firm's overall cost of capital considering all of the components of the capital structure.

Source: Investopedia

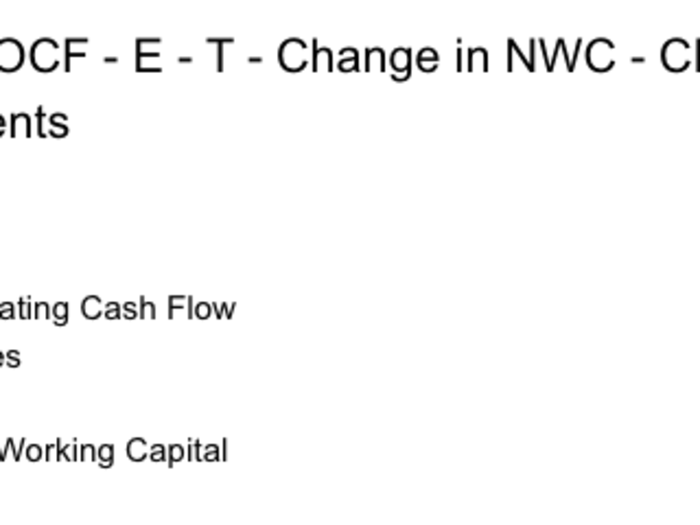

Free Cash Flow to Firm (FCFF): Measures firm's cash flow after paying expenses, taxes, and financing costs.

Source: Investopedia

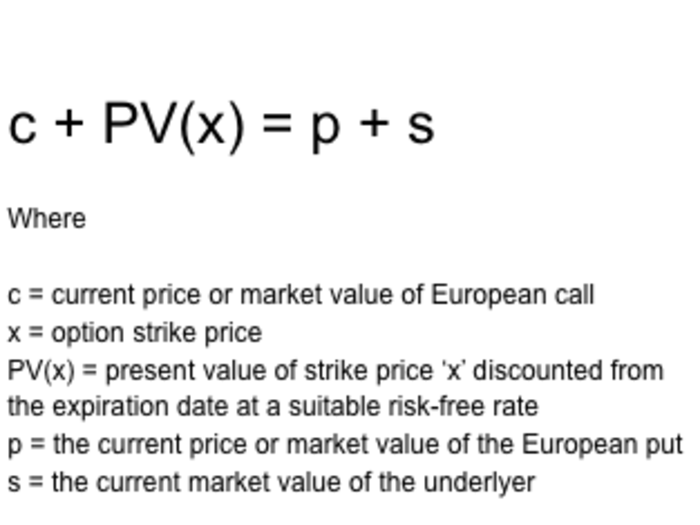

Put-Call Parity: Refers to the static price relationship between the prices of put and call options of an asset with the same strike price and expiration date.

Source: Investopedia, Risk Glossary

Variance of a Two Asset Portfolio: Measures the fluctuation of the returns of a portfolio with two assets.

Source: Investopedia, Fisher College of Business

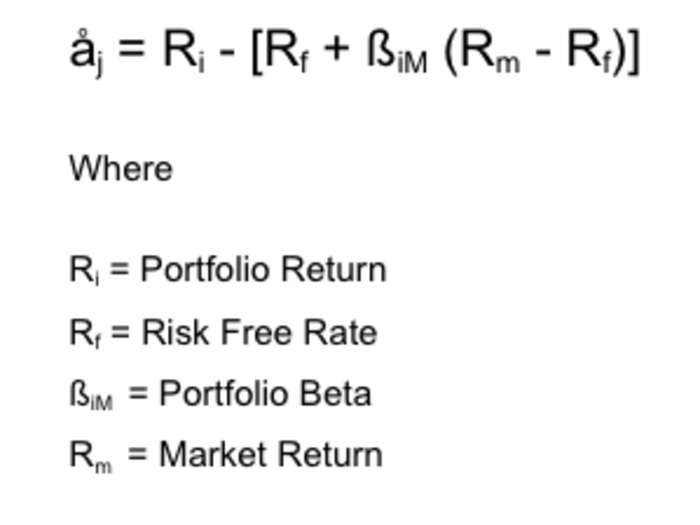

Jensen's Alpha: One way of measuring alpha, or the risk-adjusted return.

Source: Investopedia, Wikipedia

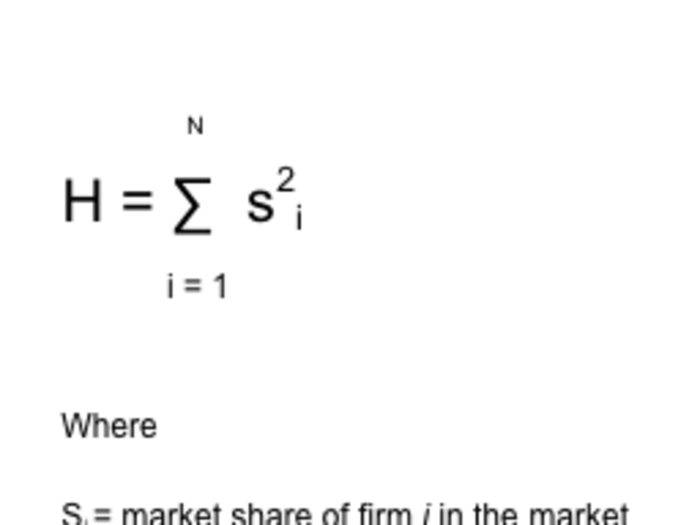

BONUS: The Herfindahl Index measures market concentration, and is used by regulators to determine whether a company has a monopoly on a market.

Source: Investopedia, Wikipedia

The CFA program isn't the only way to learn about finance.

Popular Right Now

Popular Keywords

Advertisement