Generally, borrowers can do very little other than prepaying a part of the loan (if they have surplus cash) to reduce the interest burden or increasing the EMI (if they can afford it) to reduce the tenure and therefore, the overall interest paid.

However, some experts believe home loan seekers and existing borrowers looking to switch lenders can consider experimenting with some out-of-the-ordinary home loan schemes. Such loans, which are linked to an overdraft facility, are offered by SBI, HSBC and Standard Chartered, among others.

"Such schemes can prove to be very useful, but the borrower needs to understand the product’s workings carefully before going ahead," says Vipul Patel, director of mortgage advisory firm Home Loan

|

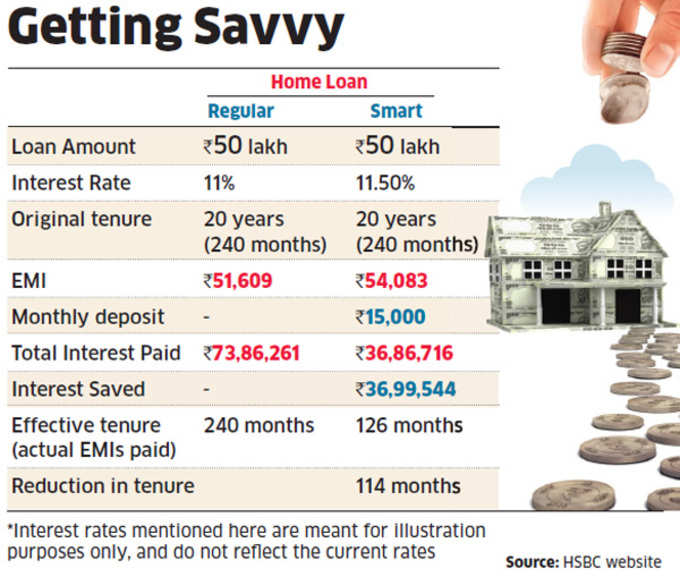

Unlike regular home loans which are standard offerings, features of these products vary with each bank. The only thing that is common among them is the home loan is linked to an overdraft facility. Any surplus money (apart from EMI) you deposit into the account will reduce the principal outstanding (only for the purpose of calculating interest), thus reducing your interest outgo.

You can also withdraw the surplus amount parked in the account, if required, though you may have to pay the applicable transaction charges per withdrawal. Again, it depends on the bank's policy."The deposits into the account actually offset the interest payable for that many number of days and, as a result, reduces the loan tenure as also the interest paid over the term of loan. This is more tax-effective as interest saved (

"You need to carry out a cost-benefit analysis to ascertain whether a simple part pre-payment is better than depositing surpluses," says VN Kulkarni, chief credit counsellor, Abhay Credit Counselling Centre. Instead, it might be wiser to go for banks that charge an

Simply put, you will benefit from these products, primarily if you direct all your savings into this account and are confident of parking a surplus. That means, it is not going to help if you are stretched for paying the basic EMI itself.