We got a look at the slide deck of a startup that's raised $70 million to upend the way we pay for healthcare

The slide deck starts with Bind's logo and simple description: "On-demand health insurance." The meaning of that phrase the slides will soon elaborate on.

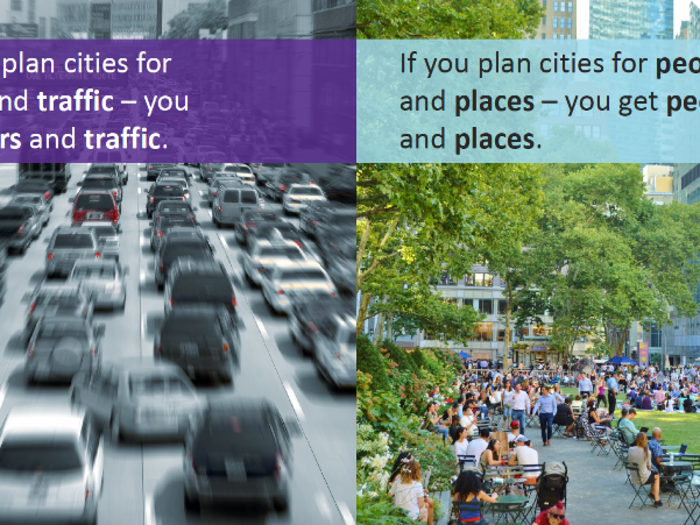

The first slide sets up the importance of planning. If you plan a city around roads and cars, that's what you get. Instead if you prioritize places for people, that's what you get.

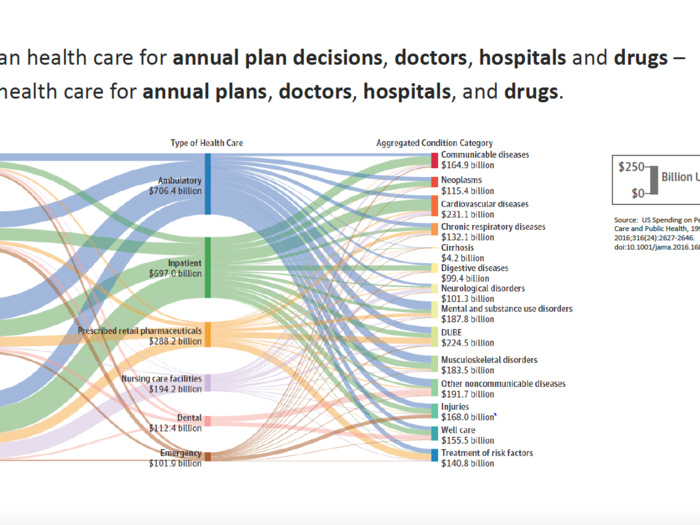

The same, the slides suggest, happen in healthcare. Right now, Miller said, health plans are set up to pay for doctors, hospitals, and drugs.

Instead, Bind's idea is to shift that thinking to discussing particular conditions and their treatments.

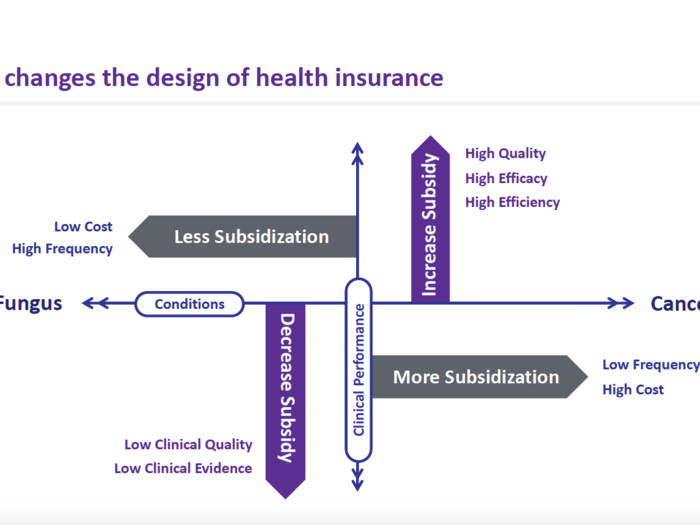

For more costly conditions to treat, like cancer, the plan would cover more of the healthcare cost. A more common condition, in this case toe fungus, might have less coverage on the plan.

"The bad thing about plans today they treat all services and all providers as the same," Miller said. "We're going to make subsidizations smart."

Coverage depends on what kind of treatment you seek out for a particular condition.

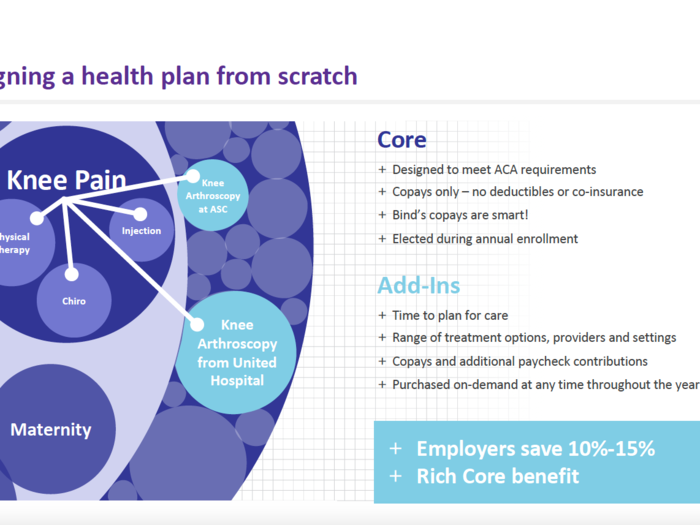

Take knee pain. Physical therapy might be covered under the core part of the plan.

But say you want to get a knee arthroscopy, a surgical procedure. You'd need to add on that coverage to your core plan, paying an additional amount.

The hope with this strategy is to help members try out less-invasive or lower-cost treatment plans first, ideally saving employers money, too.

"What we do is we're flexing how much coverage costs depending on what you used," Miller said.

Next, the slides queue up examples of that in practice.

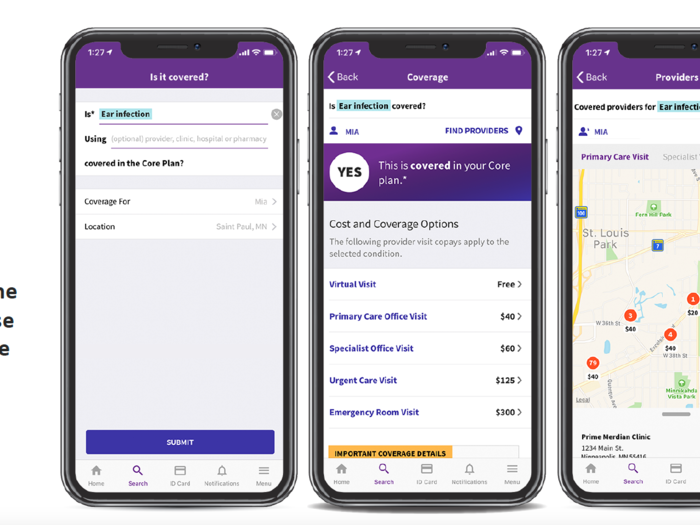

Say a Bind member is having some ear pain and wants to see a doctor about a possible ear infection. The member can search in Bind's app to see if that's covered under the core plan and how much a visit might cost depending on where they go. For instance, a virtual visit might be free while a visit to an urgent care center might cost the member $125.

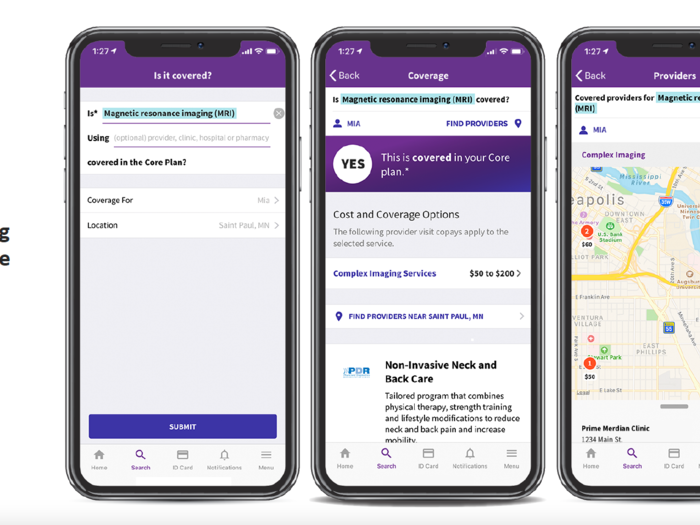

For members who need to get an MRI, the app can help them figure out what center might be the best to go to.

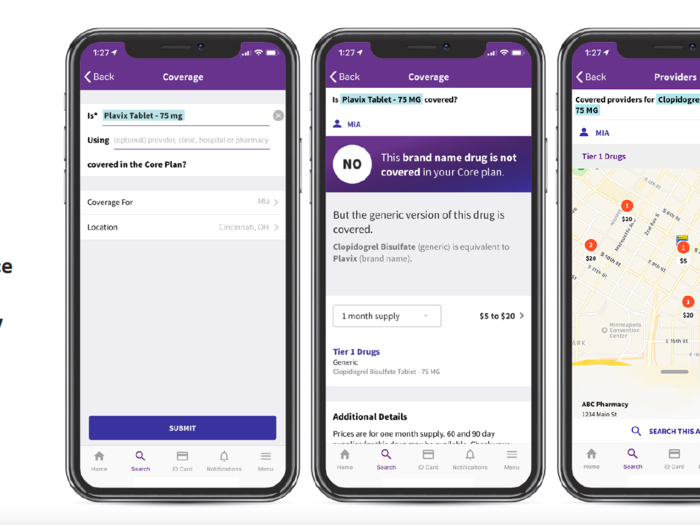

The same goes for prescriptions.

Should a member have a question about whether a branded prescription drug, like the heart drug Plavix, is covered, the member would see that he or she could be taking the generic version instead. A map lays out where he or she can pick up the drug at the lowest cost.

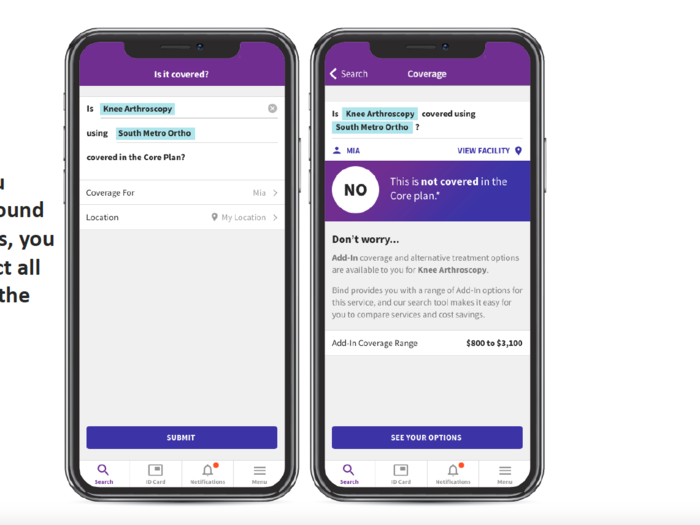

Here's where the add-on care comes in.

Say a member is interested in getting the knee surgery and wants to know what it would cost at a local medical center. The app can inform them that it's not a part of the core plan. Ahead of the surgery, however, the member can buy add-in coverage, giving a better sense of what their medical costs will be.

At that stage, the member is shown what is included in the core plan, such as physical therapy. The app can also inform the member if there's a cheaper add-in option.

As part of a typical health plan, an insurer isn't sure whether you're going to get a procedure at a facility that will hand them a $24,000 bill or a $6,000 bill. To make sure the plan has enough money to cover the more expensive place, it sets higher premiums.

Bind is betting that by giving its members a clearer picture of where a procedure is more cost-effective, members will choose that spot more often. That way, Bind doesn't have to set premiums to account for the procedure at a facility that costs $24,000. To do this, Bind puts to use data collected by other insurers.

"The reality is we couldn't have done what we have done today without the help of big data sets insurance have," Miller said.

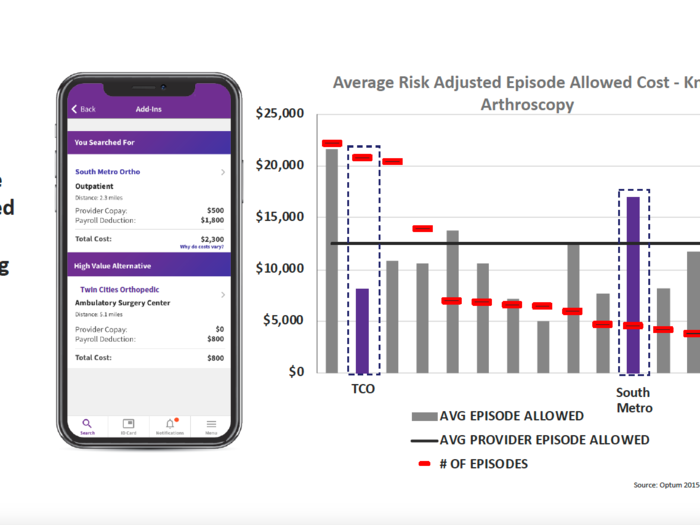

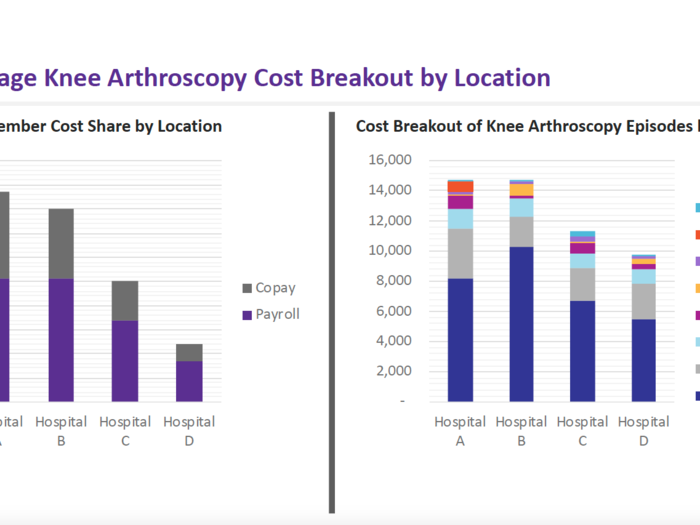

Here's another look at the costs that factor into a knee surgery at different locations. There's a lot of variability on what each place charges.

Bind then goes into how the insurer has performed since launching its first plans in 2018.

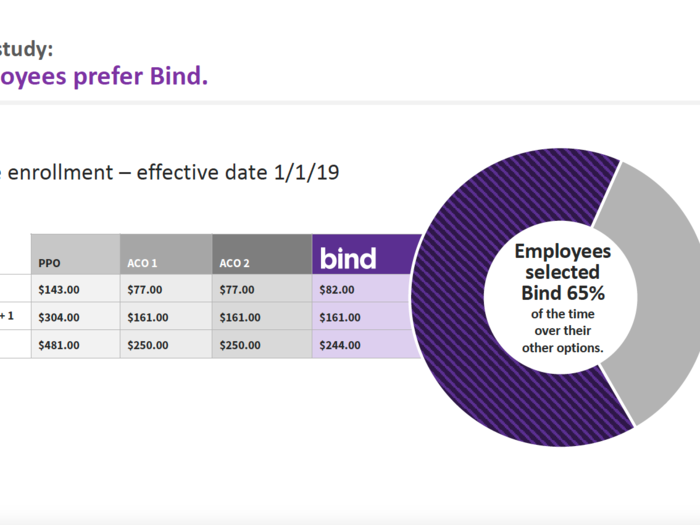

Here's a look at how Bind's premiums compared to other health plans an employer offered its workers.

A PPO, or preferred provider organization, plan came with $143 in premiums, while the Bind plan cost $82 a month. The price point, Miller said, is in line with a plan that would normally come with a high deductible. Bind plans don't have high deductibles.

In this instance, the employees picked the Bind plan 65% of the time over other insurance options.

And it seems that those who choose Bind's plans are using them.

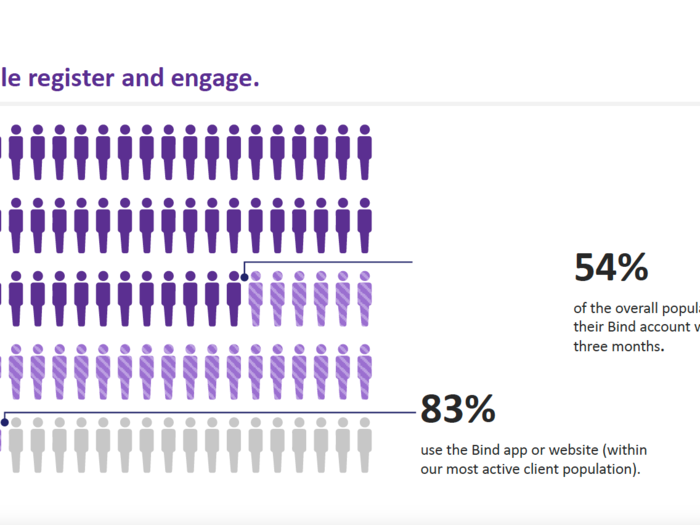

Because Bind requires members to interact more than standard health insurance does, it's important that they log in and use the app or website.

Across Bind's whole business, 54% of members activated their Bind accounts within the first three months, a number Miller said is growing as members start to need healthcare throughout the year.

With one particular employer, Bind noticed that 83% had used the app or Bind's website for their care.

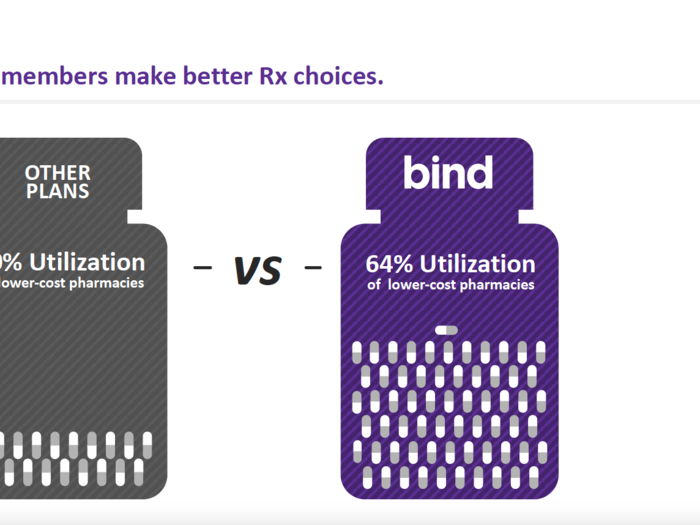

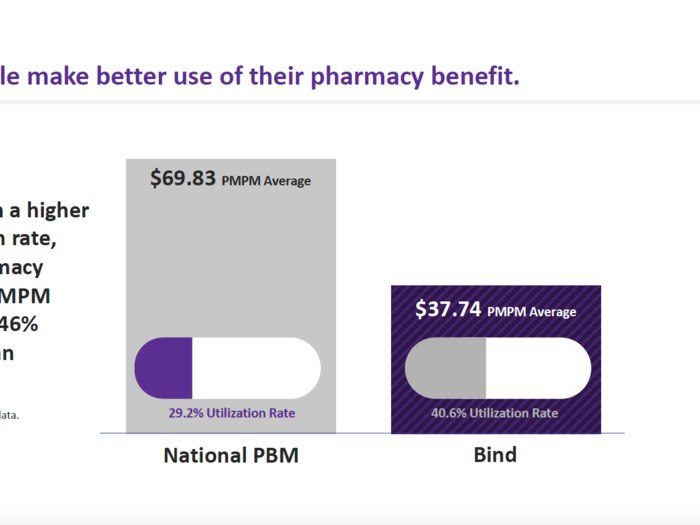

Bind also saw that its members were more likely to use a lower cost prescription compared to other health plans.

And while Bind members more frequently used their pharmacy benefit, the average per member, per month spending on the pharmacy benefit was roughly half of what traditional plans pay out in pharmacy benefit.

Bind also shows potential new clients how members rank Bind.

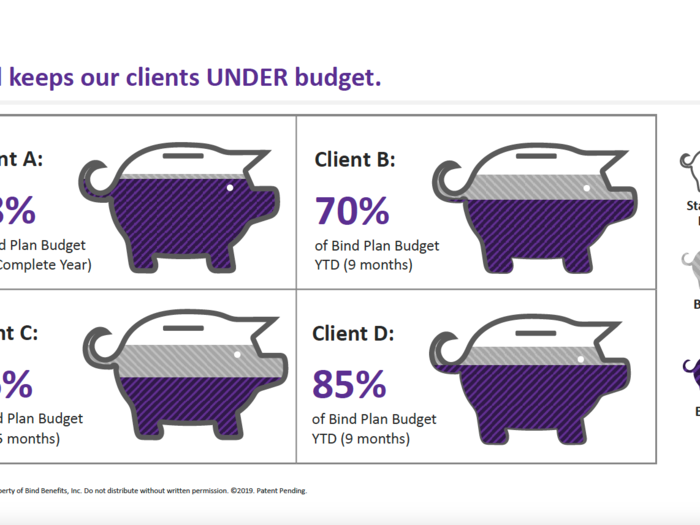

Next, Bind shows how it managed to keep clients' medical spending in check.

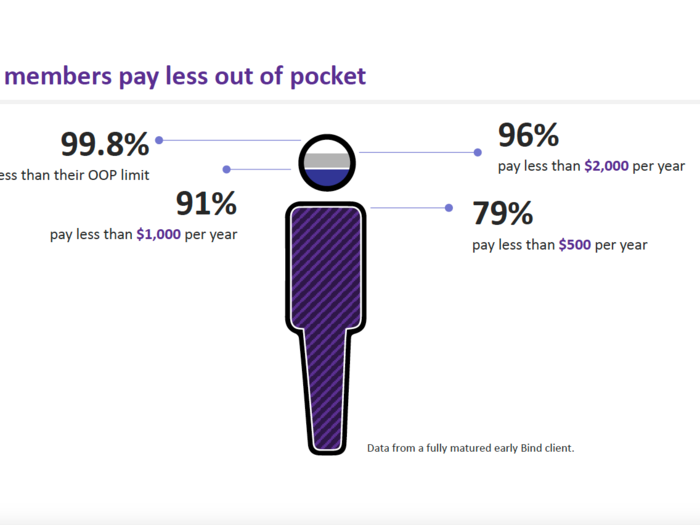

Here's how much members themselves tend to pay for their care. Bind says that 96% pay less than $2,000 each year in out-of-pocket costs, and 79% of the members from this early client paid less than $500 a year.

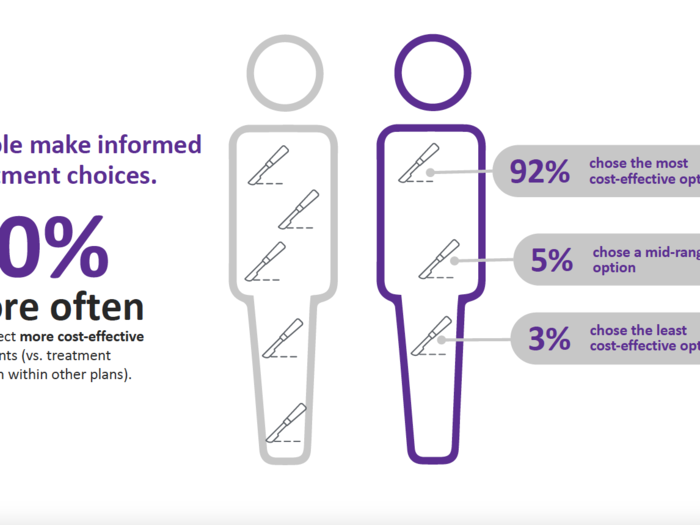

The members tended to pick more cost-effective treatments than they might have on regular plans as well.

With that, Bind signs off with a "thank you."

Popular Right Now

Popular Keywords

Advertisement