These 5 charts show how Uber and Lyft compare financially as they fight to win the ride-hailing race

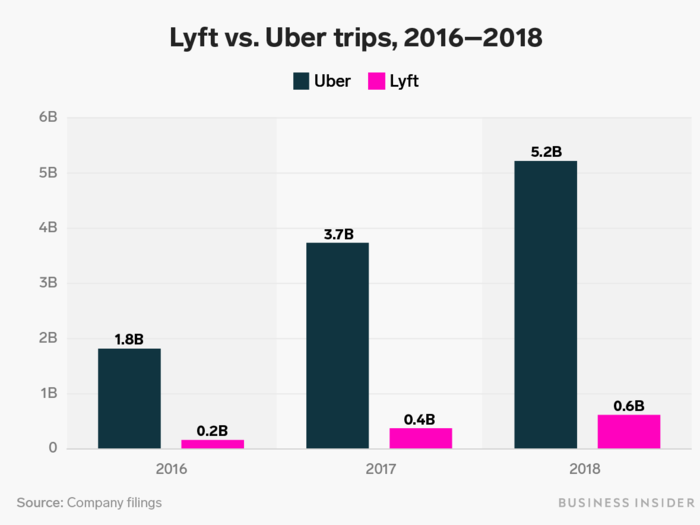

The data show that Uber is, as expected, still much larger than Lyft.

In terms of total rides, that gap is even bigger.

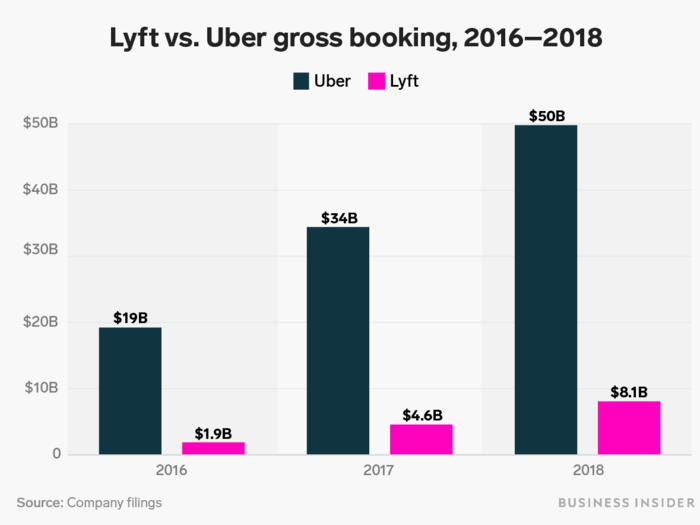

Those two metrics blend to give us what the companies call "bookings."

In a nutshell, gross bookings is the total Uber or Lyft charge from riders, before paying drivers, which is easily one of the biggest expenses for both companies. They both calculate the exact bookings line slightly differently (Uber includes Uber Eats, for example), but for showing directionality, it's a useful metric to investors.

"Our long-term valuation framework for Lyft assumes that the company achieves a 31.4% bookings share by 2029 (vs. an estimated 14.9% share today)," D. A. Davidson's White said in his initiation report.

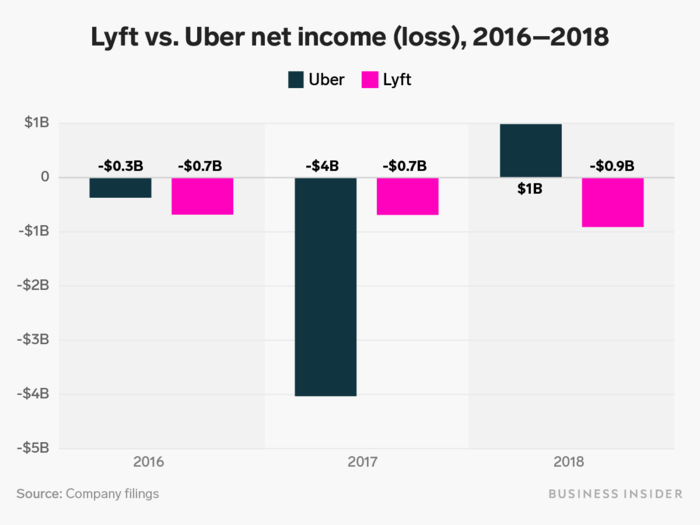

Uber has turned a profit.

Lyft, however, warned investors in its IPO filing that it might never make a profit. Since trading began at the end of March, shares of Lyft have fallen more than 26% from their first prices.

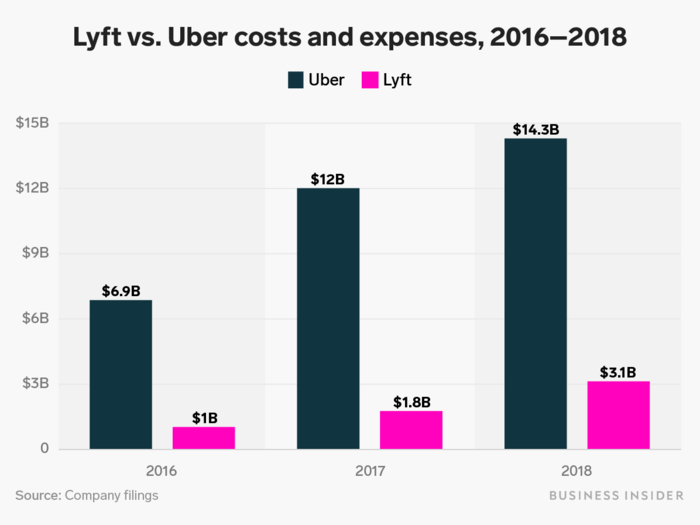

One of the most important lines: costs

Revenue, of course, is meaningless without knowing what costs a company has to spend that income on.

"We believe there could be continued pressure on LYFT shares while investors wait for Uber's roadshow and dig further into the full financial metrics," Daniel Ives, an analyst at Wedbush, said in a note to clients this week. "In our opinion the battle for market share will be balanced going forward. "

Popular Right Now

Popular Keywords

Advertisement