The last 4 years of WeWork's pre-IPO financials show just how important cashflow is to the company's growth

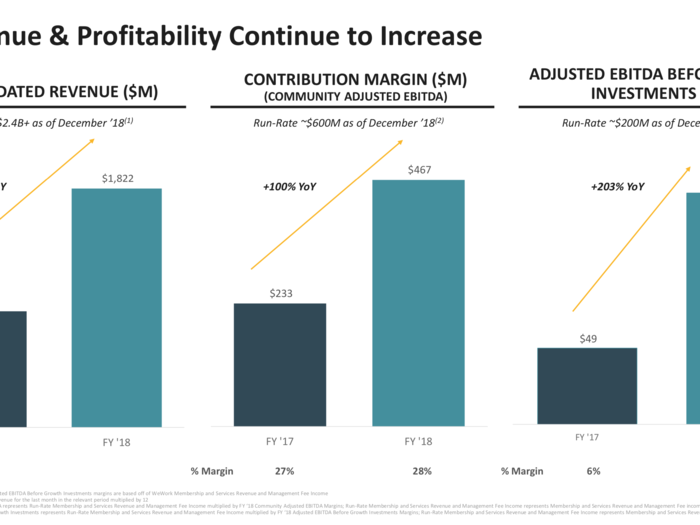

WeWork's 2018 financials: The company's revenue growth is impressive, and a huge portion of it comes from non-US territories.

WeWork uses its own definitions of profitability, "contribution margin" and "adjusted EBITDA before growth investments." These definitions are not standard.

The definitions exclude many of WeWork's ongoing costs. Crucially, they both only show "EBITDA" profits — or "earnings before interest, taxes, depreciation and amortization."

WeWork is not profitable on a standard accounting basis.

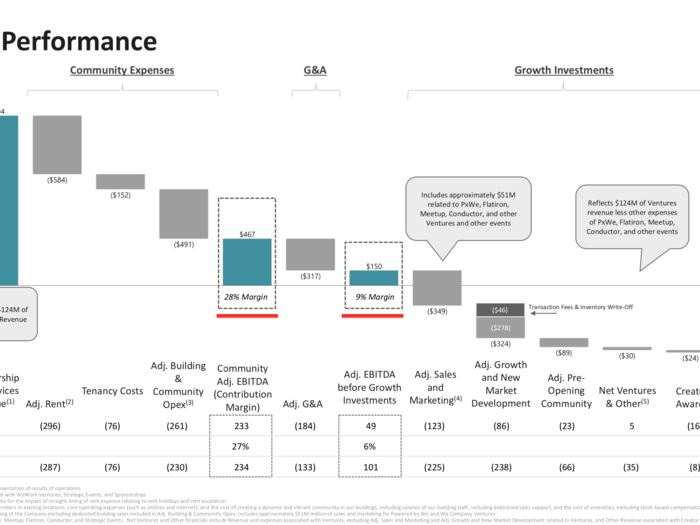

This diagram shows how those EBITDA margins are constructed.

The red lines show profits using WeWork's definitions, and at far right you can see that once other ongoing costs are factored in WeWork is not profitable.

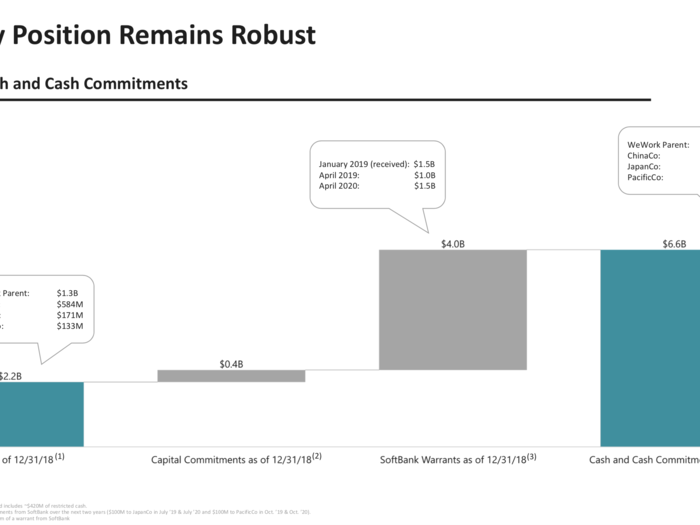

But WeWork isn't short of cash! It has $6.7 billion on hand.

This chart shows the major sources of WeWork's current cash position.

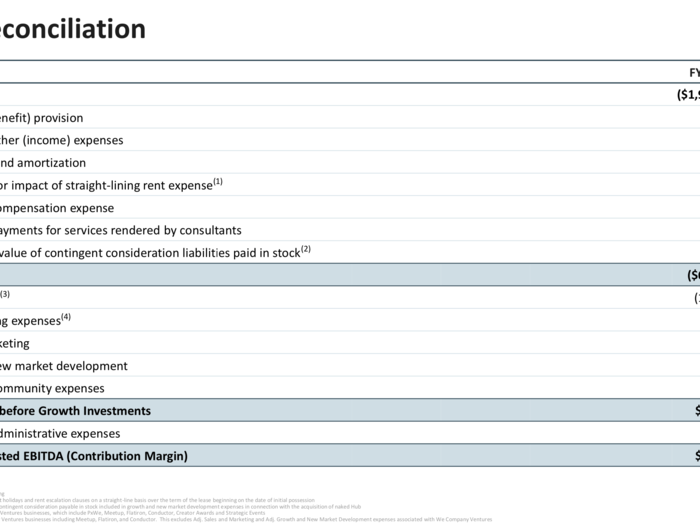

This grid shows how WeWork constructs its "adjusted EBITDA" margins. A lot of non-cash items are added back against the overall net loss.

Note that this is NOT an income statement and does not contain all the regular expenses you'd see on a normal income statement. In fact, many of those items in the top section under "net loss" are non-cash expenses being added back to create those margins.

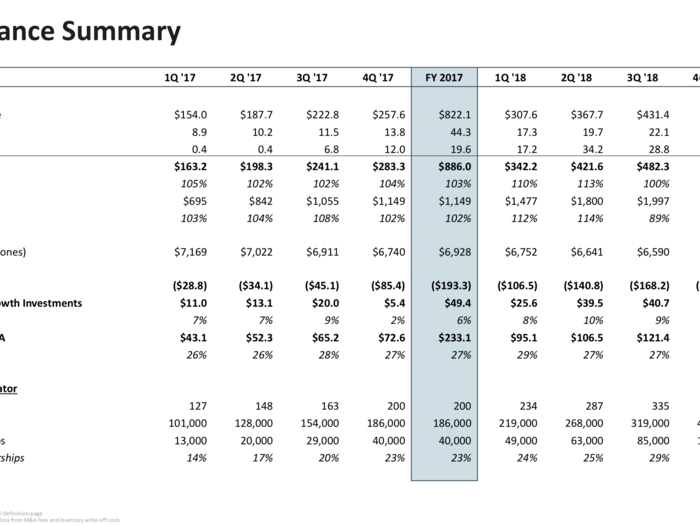

Similarly, this "Performance Summary" shows only revenues and margins — not cash expenses.

WeWork is a growing business, certainly. But this section does not show net profits.

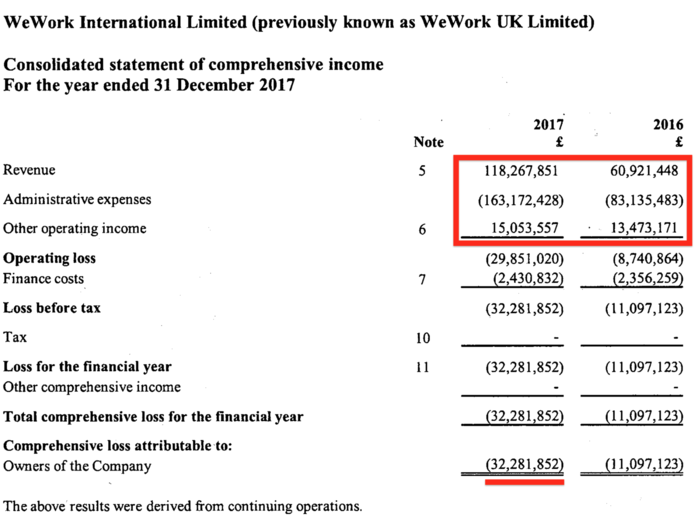

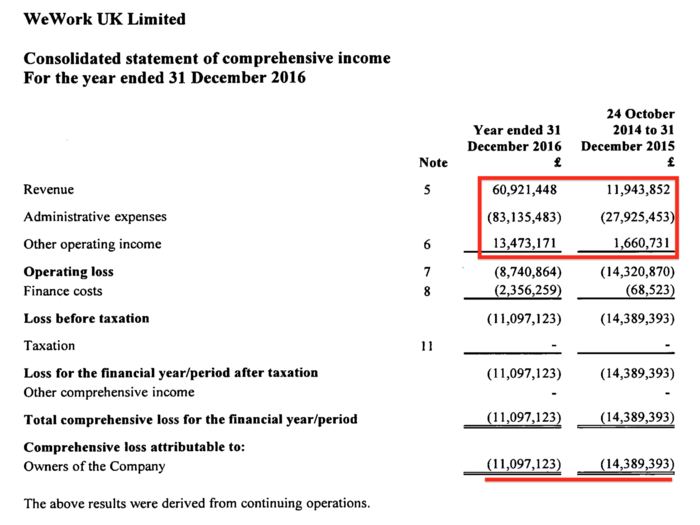

This is WeWork UK's income statement for 2017, the most recent year it has disclosed. In this year, the UK was 14% of WeWork's entire business. Note that WeWork's admin expenses far exceed its revenues, leading to a net loss on the bottom line.

WeWork spent £163 million building its business but only made £133 in revenues.

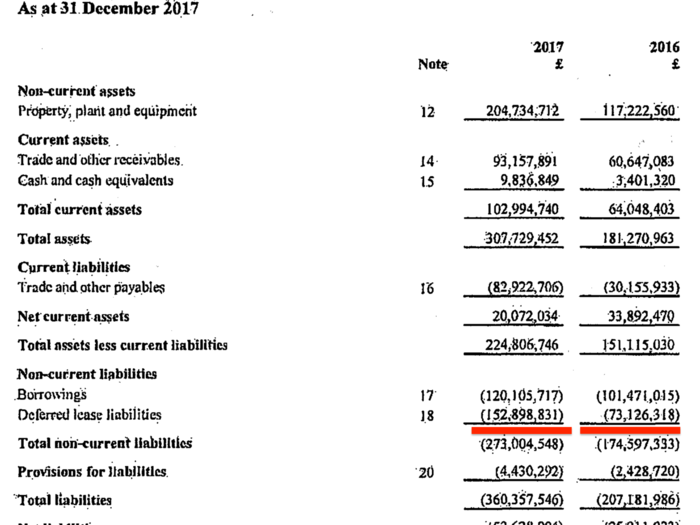

WeWork UK is carrying massive "deferred lease liabilities." These are buildings the company has leased, but the rent isn't due immediately — so WeWork doesn't have to pay it.

WeWork accrued £153 million in deferred leases in the same year its revenue was £118 million.

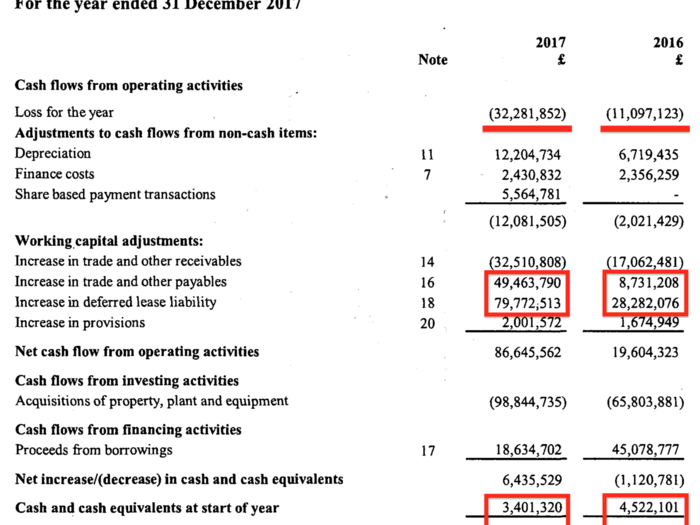

Here's how WeWork UK stays cashflow positive while making a loss: "working capital adjustments."

WeWork UK made a loss of £32 million in 2017. But at the same time, it was able to defer £49 million in trade payables and defer £80 million in lease payments. That saved cash offset the huge costs of running the business. The ultimate effect was that WeWork UK's cash position increased from £3.4 million to £9.8 million over the year.

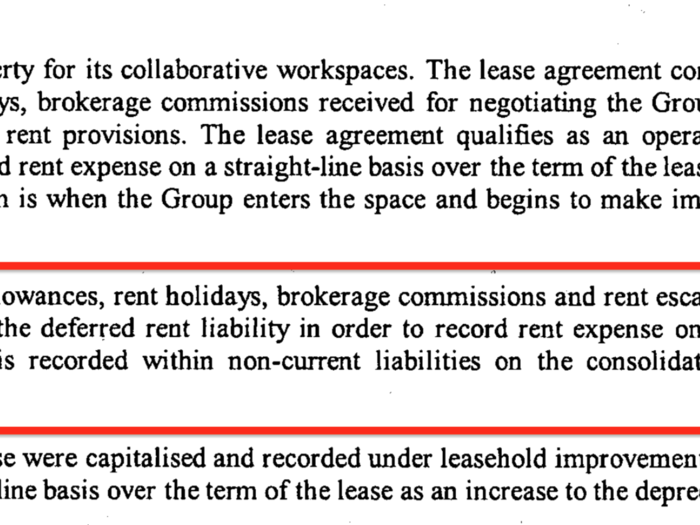

Here is where WeWork gets its credit: Landlords offer WeWork deferred rent payments or "rent holidays" if WeWork improves the buildings.

Those credits make the current carrying cost of WeWork's long-term leases much cheaper.

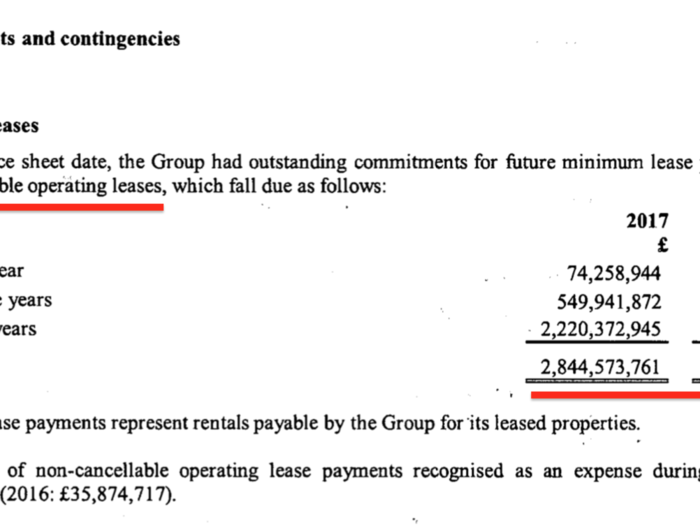

WeWork UK's total lease commitments are massive: £2.8 billion ($3.65 billion).

That's a huge commitment. The disclosures say the leases are "non-cancellable." Remember, the business only generated £133 million in revenues in the same year.

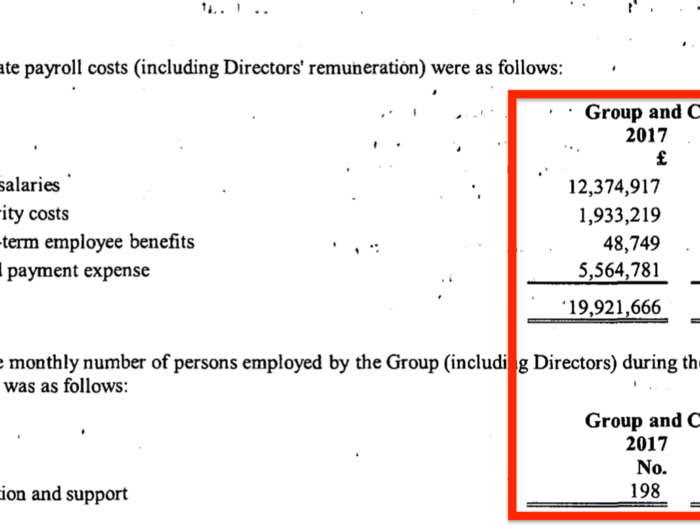

This is how many staff WeWork had in the UK, and how much they got paid.

Here are the WeWork UK income statements for 2016 and 2015.

Note again that admin expenses — lease costs, mostly — far outstrip the company's revenues. Again, that led to net losses on the bottom line.

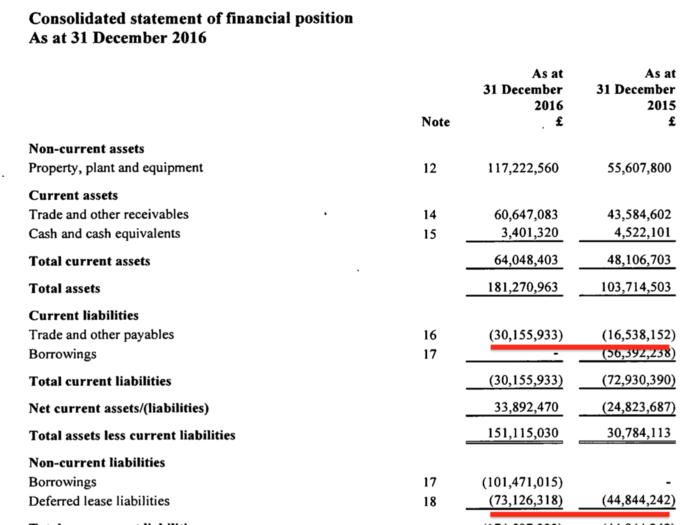

Here's the balance sheet for 2016 and 2015.

There are a total of £30 million in deferred bills and £73 million in deferred lease payments on the balance sheet for 2016.

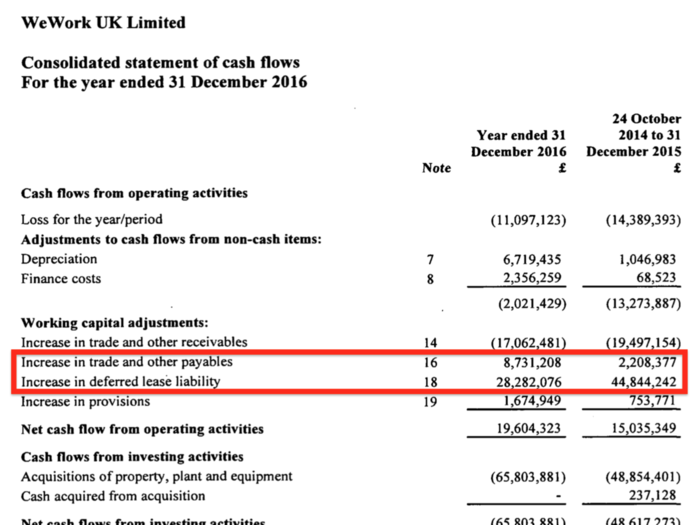

The cashflow statements for 2016 and 2015 show how much of those deferred bills WeWork UK was actually able to use.

WeWork UK recorded positive cashflow of £8.7 million from unpaid payables and £28 million in deferred lease payments. That was helpful — the company's revenues for the year were £74 million.

By the end of 2016, WeWork UK had £73 million in deferred lease liabilities.

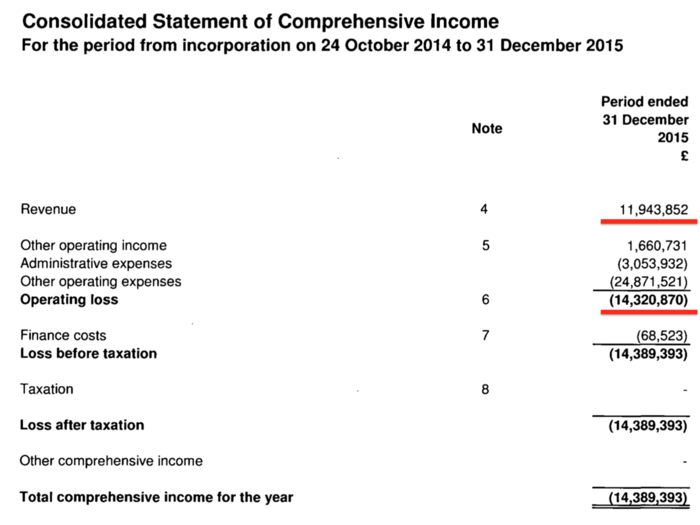

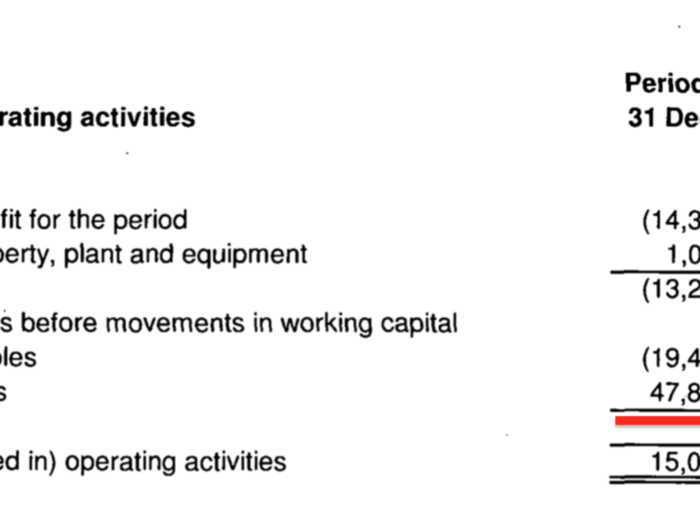

This is the earliest income statement WeWork ever filed in the UK.

There was revenue of £12 million but a loss of £14 million.

Even at this early stage, WeWork UK had already added £45 million in deferred leases to its balance sheet.

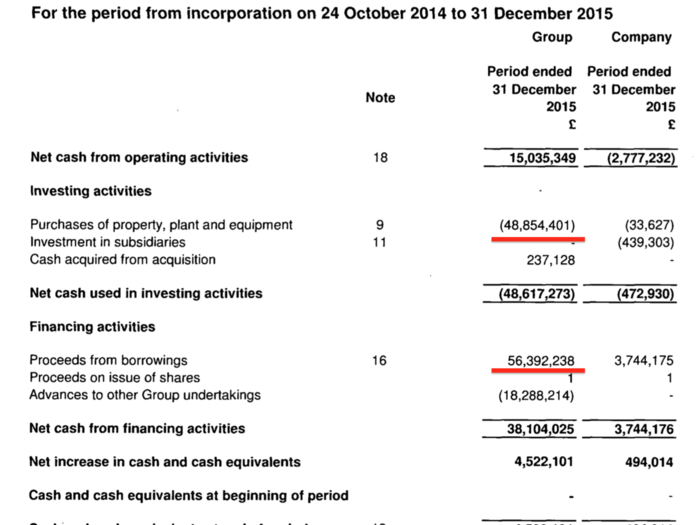

This early simplified cashflow statement shows that WeWork UK spent £49 million on leases to get the business rolling but borrowed £56 million to do that, probably from its US parent.

Here are the total deferred lease liabilities that resulted from that ... £45 million.

... and the business was helped along by £48 million in unpaid payables.

Even at this early stage, WeWork's business model was clear: cashflow was more important than making a profit, and getting various forms of credit for leases it signed would be a key financial driver of the company.

- Read more about WeWork's financials:

- WeWork reported its financials for 2018 and both its revenue — and losses — doubled

- WeWork documents reveal it owes $18 billion in rent and is burning through cash as it seeks more funding

- WeWork confidentially filed to go public

- The financials for $17 billion WeWork's UK unit show it doesn't make a profit ... yet

Popular Right Now

Popular Keywords

Advertisement