Tesla is a battleground stock. Here's where major Wall Street analysts stand right now.

Adam Jonas

Ryan Brinkman

Firm: JPMorgan

Price target: $200

Rating: Underweight

"The now clear incongruence of CEO outlook statements with official company guidance may hurt the perception of management commentary, eroding investor confidence and potentially placing additional pressures on the shares," Brinkman said in report dated April 4.

Itay Michaeli

Firm: Citi

Price target: $273

Rating: Sell/High Risk

"Though Tesla bulls might look past the Q1 Model 3 miss (also given recent intro of $35k version), the S/X numbers will likely spark some legitimate demand & company margin concerns, particularly given the risk for some incremental cannibalization from the recently introduced Model Y," Michaeli wrote in a note to clients on April 4.

Ben Kallo

Firm: Baird

Price target: $465

Rating: Outperform

"The Model S and Model X are luxury electric vehicles with significantly more range than many

of their competitors," Kallo wrote in a note to clients last week.

David Tamberrino

Firm: Goldman Sachs

Price target: $210

Rating: Sell

"While we believe TSLA has developed a lead relative to OEM peers with respect to electric vehicle technology, we believe its operational execution has been more challenged and see its competitive lead waning as other companies launch more models and EV incentives phase out for TSLA ahead of that competition," Tamberrino wrote in a note dated April 4.

Joseph Spak

Firm: RBC Capital Markets

Price target: $210

Rating: Underperform

"Tesla reported total 1Q19 deliveries of 63k, 31% below 4Q18 levels and versus RBC/FactSet consensus of 71.7k/76k," Spak wrote in a note to clients last week. "We believe the results are disappointing across the board and estimate that this could potentially translate into a ~$1bn+ revenue miss."

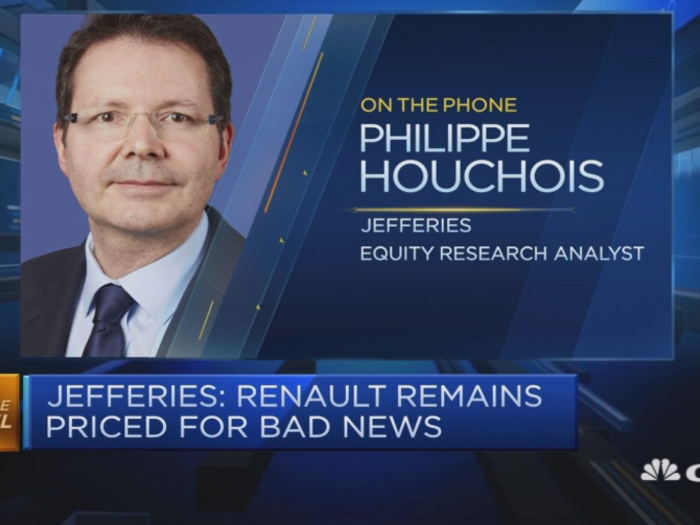

Philippe Houchois

Firm: Jefferies

Price target: $450

Rating: Buy

"Tesla reported 63k vehicles delivered and 77.1k produced, 12% and 8% below JEFe respectively," he wrote in a note last week. "The miss is on S/X, which disproportionately hurt profitability."

Colin Langan

Firm: UBS

Price target: $200

Rating: Sell

"Given the volatility, we are vigilant for the next positive catalyst; however we don't see one near term," he told clients on Monday. "While growth may reaccelerate in Q2, we forecast it will still fall short of guidance & consensus."

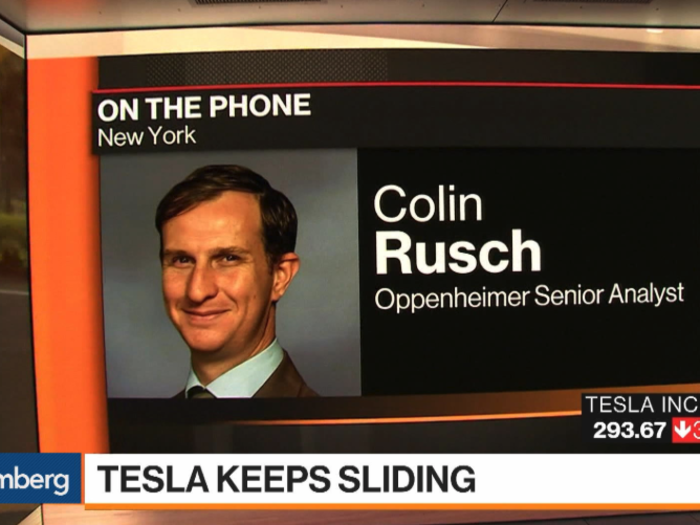

Colin Rusch

Firm: Oppenheimer

Price target: $437

Rating: Outperform

"We anticipate bulls will look through 1Q19 weak deliveries, pointing to weak global auto demand and a reiteration of FY19 guidance," Rusch told clients last week. "We maintain our positive bias, waiting for full financials when the company reports later this month."

Dan Ives

Firm: Wedbush

Price target: $365

Rating: Outperform

"We maintain our OUTPERFORM rating as we still firmly believe in our long term Tesla demand EV thesis despite this near-term turbulence, however we are lowering our price target from $390 to $365 to reflect lower deliveries and a higher chance of capital raise now on the horizon," he told clients last week.

Popular Right Now

Popular Keywords

Advertisement