I tried out Dave, the Mark Cuban-backed app that just raised $100 million and wants to kill bank overdrafts. My feelings are mixed.

Here's what the app looks like on my iPhone. Dave is also available on Android.

Dave is not only the name of the app. It's also the name of the cartoon bear who guides you through the app.

I am usually a skeptic, but I found Dave's ursine avatar to be a cute way to guide a user through the app. The whole app has a clean, cartoon style and is easy to navigate, and Dave's instructions are clear and conversational. There's just something calming about a cartoon bear, even if it's telling you that you're about to run out of money.

I had significant issues getting Dave to communicate with my bank, Chase. This may be my bank's fault.

It took me four separate attempts and 15 minutes to connect my bank. Dave's support page has a few troubleshooting suggestions, but eventually Chase was able to connect without me having to turn off any security features with my bank account. I have had issues with Chase connecting to other services, so it may have been an issue with my account. Still, I was frustrated.

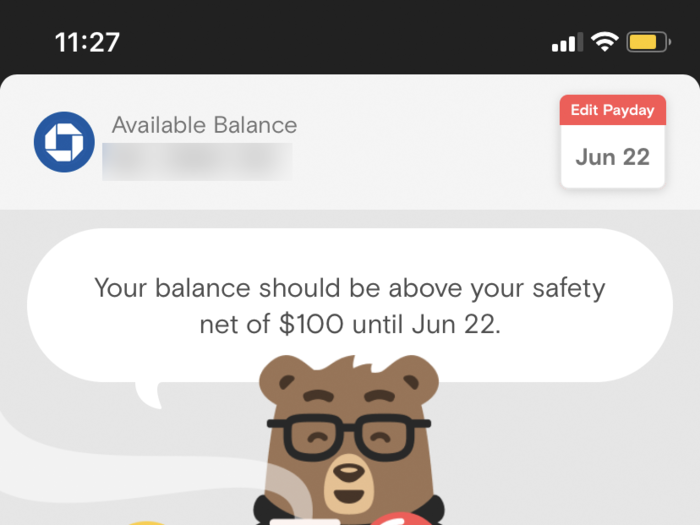

Dave's homepage is central command for its financial forecasting features.

My personal favorite feature is on the homepage of the app. Like a traditional banking app, Dave shows your current account balance. Unlike traditional banking apps, it actually calculates what your lowest account balance will be before your next paycheck.

It forecasts by analyzing the schedule and average size of your paychecks and recurring payments (rent, credit card, utilities). This number is right in the center of the screen, in bigger font than your actual account balance, highlighting it so that it remains top of mind. The page also breaks down which recurring payments are expected to be withdrawn before your payday.

This feature seems simple enough, but I found there to be a calming effect to knowing exactly how much money I actually would have before payday. Now that I've experienced it, I am shocked that my normal Chase app doesn't have any features similar to this (neither did Chase's now-defunct mobile app Finn).

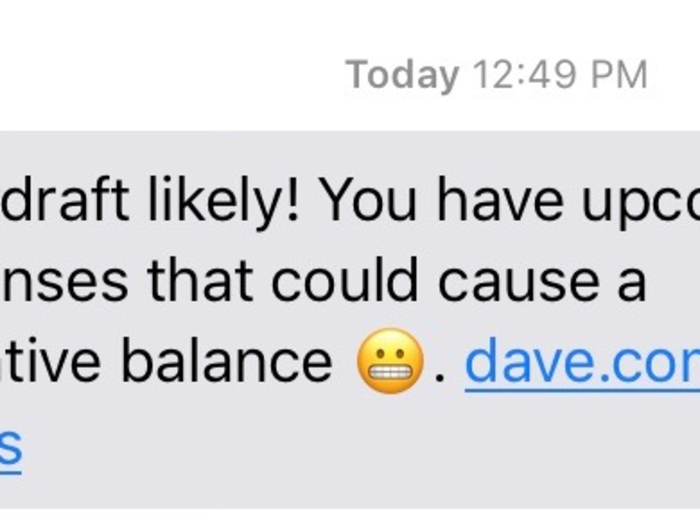

Dave's notification feature that warns of potential overdrafts works very well.

I moved some money out of my bank account to trigger Dave's low-balance notification feature. Within three hours, I received a text that my upcoming expenses will put my balance in the red. Even if I wasn't checking Dave actively, this notification feature could keep me from having to pay costly overdraft fees.

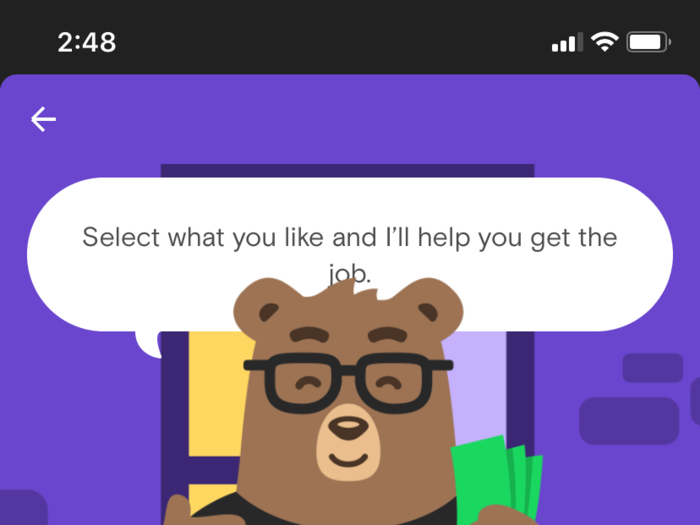

Dave's homepage also connects you to gig-economy jobs in case users consistently find themselves coming up short before payday.

This simple feature, conceptually, could keep users from having to live from payday advance to payday advance. A link on the homepage directs the user to a list of 10 different gig-economy jobs, such as a Lyft driver. Depending on what they want to do or are able to do, they can select as many of these jobs as makes sense. Dave then sends the user personalized links to apply to each company by text and email.

I could see this feature eventually growing, but right now, it just feels like an under-baked gig-economy job board.

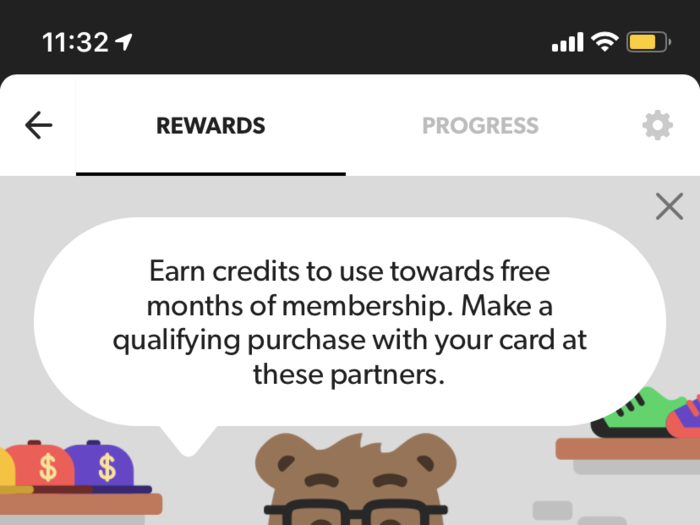

Dave offers a rewards feature, which allows you to waive the $1 monthly fee.

Dave, unlike its largest overdraft-fighting competitor Earnin, has a monthly fee of $1. To counteract this, they allow you to earn free months by making purchases at their partners with your linked debit card.

I work in Manhattan's financial district, and saw at least a few vendors that were close by. I imagine that it may be harder to use this features outside of a major city. With such a low cost for the service, I wouldn't consider this a make or break issue for Dave.

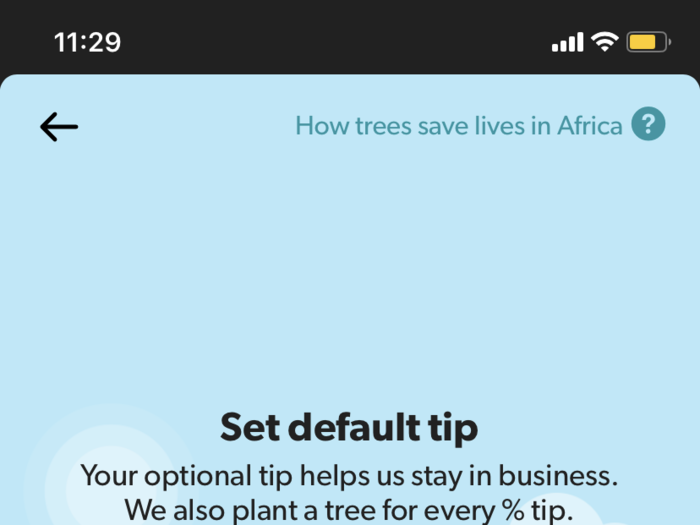

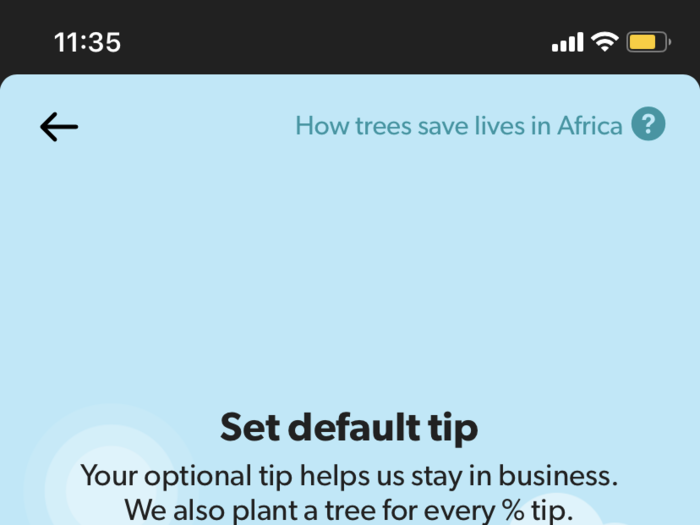

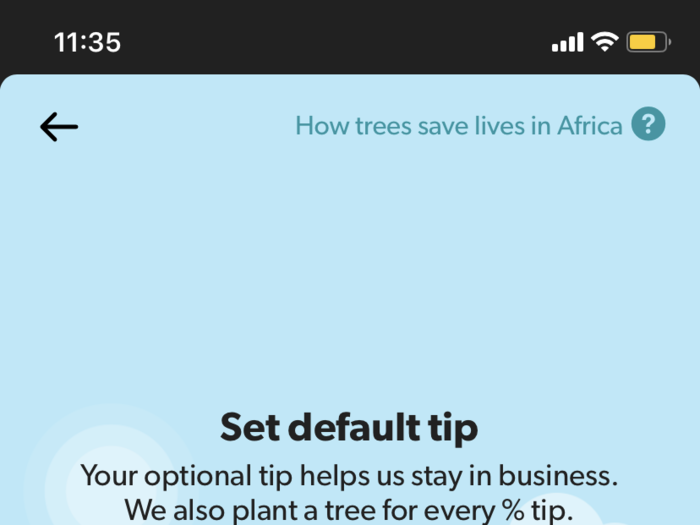

In settings, you can chose what your default tip percentage is. This is where I began to have some qualms with the app.

The app defaults to a tip of 10% of the amount being requested. At first glance, that may not seem like so much money. With a maximum tip amount of $75, the total cost is only $7.50, substantially less than an overdraft fee would be. However, if you compare to payday loans, and think of the tip like an interest rate, this amount does not seem so attractive. Let's say you decided to borrow $75 dollars a full 13 days before payday. With a 10% tip, that $7.50 is the same as a 280.76% APR, putting it well in line with typical APRs for payday loans.

Of course, the tip is voluntary and is a one-time fee that doesn't compound interest. For that reason alone, it has an advantage over payday loans. But as you'll see, the app has multiple strategies to get you to leave a tip. This makes sense, as the company relies on tips to make money.

One strategy is visible on this page and appeals to users' charitable nature. The app plants one tree for every percent given in a tip, and if you're interested enough, will explain how these trees help save lives in Africa.

If you change your default tip to 25%, you can see there are many more trees in the background, and Dave looks even happier holding his shovel.

A 25% tip on that same $75 advance ($18.75) for 13 days would be equivalent to a whopping 701.92% APR.

With a 1% tip, there's only one tree in the background, and Dave's smile turns into a decidedly less happy smirk.

A 1% tip on that same $75 advance ($0.75) for 13 days would only be a 28.07% APR. That's significantly lower than most payday loans.

With no tip, the background has become a desert. Dave, holding a dead plant, looks clearly upset.

For someone who is paying close attention to their finances, its easy enough to avoid these visual cues and do whatever is most responsible. It's also easy enough for a user to give a tip that translates to a too-big APR. I'd recommend that any Dave user figure out the equivalent APR to their tip before using the app.

I set my default tip to 0%. When I went to get an advance, I noticed that my default tip was back at 10%. After some further investigation, I found out that the lowest default tip allowed is actually 1%.

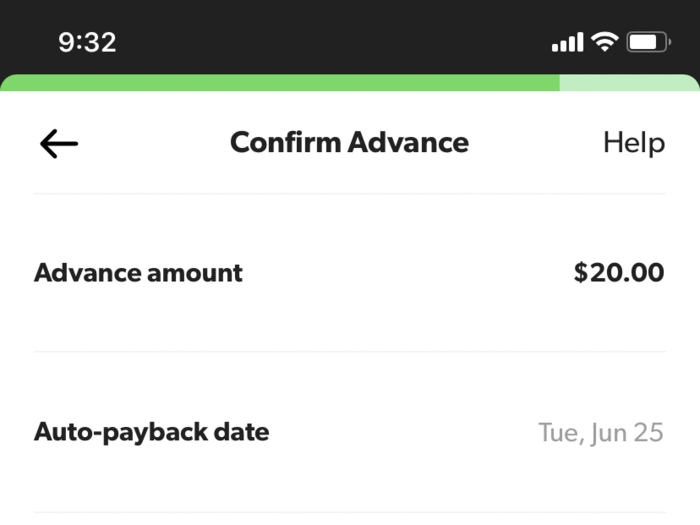

Actually setting up an advance was very simple, and everything went according to plan.

The maximum I could advance myself was $20, as I had just started a new job and didn't yet have paychecks that Dave could use to verify my ability to pay back. This should be front of mind for any user starting a new job or between jobs. Also, if you're paid irregularly or make commission, it might be harder for Dave to confirm your ability to pay back an advance.

I had the option of waiting to pay back until the Friday of the next week, but chose a quicker turnaround. This length is increased to the next payday once the user has a verified paycheck and can take out larger amounts in advance.

The user also has the option to expedite the delivery of their advance for $2.99. I chose the free method, and still received my advance next business day (Friday AM to Monday).

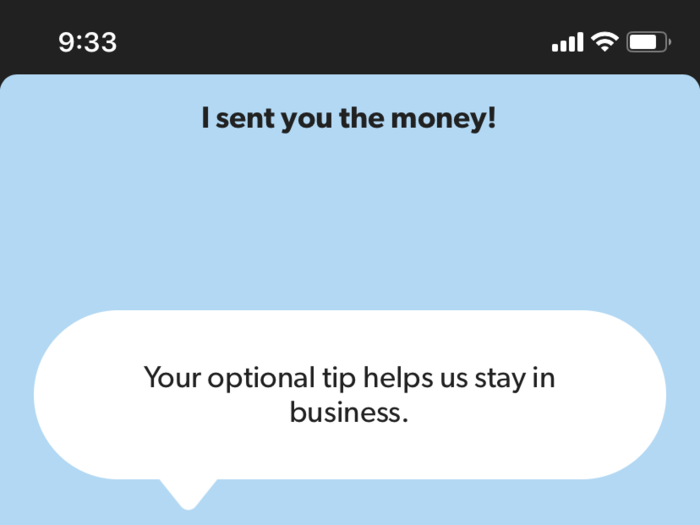

The user selects the tip after they have submitted their advance.

This page makes no mention of trees being planted for each percentage tipped, and doesn't have the same manipulative imagery as the pages to set default tip amounts. Still, I had to manually insert a tip amount of 0%.

Overall, the process went well, and I received my money and had my money taken out of my account without a hitch. As long as the consumer is mindful of their money, and careful to not tip too much, Dave is a useful app.

Popular Right Now

Popular Keywords

Advertisement