How grad schools became the hidden culprit behind America's student-debt crisis

More people go to graduate school than they did a decade ago — but the degree has gotten more expensive.

Graduate-student borrowers made up more than half of the $1.3 trillion student-loan debt recorded in 2016.

In 1992, 45% of advanced-degree households comprised the national $41.5 billion student-loan-debt total (in real 2016 dollars); in 2016, 51% of advanced-degree households comprised the $1.3 trillion in debt, according to "Inequality and Opportunity in a Perfect Storm of Graduate Student Debt," a working paper by James Pyne and Eric Grodsky.

More graduate students are enrolling in master's programs, borrowing more when they do, and completing them, according to Pyne and Grodsky.

Federally subsidized student loans have higher interest rates for graduate students than for undergraduate students.

Graduate student loans work differently than for undergrads.

For one, graduate students receive less financial aid, particularly from federal, need-based Pell Grants. Many low-income students who relied on this type of funding to pay for undergrad will have to take out debt for grad school, according to US News & World Report.

Plus, graduate-student loans have higher interest rates, as well as a higher borrowing limit than undergrad aid. Loan limits can even reach over $200,000 for students in certain health fields, US News found.

Since graduate students attend school later in life, many have higher rent to pay and families to provide for — factors that make paying for school more difficult, according to NPR.

"If graduate students aren't paying off all their interest on time, then their debt can really add up," NPR's Cardiff Garcia said.

Still, graduate students can pay off their loans more easily because they get high-paying jobs after their programs.

While graduate students may shoulder more of the loan burden, they tend to pay off their loans after getting jobs.

People with graduate degrees are less likely to default on their loans than those who never graduated undergrad. Drop-outs with low debt levels tend to default due to their inability to find a high-paying job without a degree, writes MarketWatch's Jillian Berman.

But those high-paying jobs aren't always the path to wealth they once were.

As of 2018, 37-year-old orthodontist Mike Meru owed $1,060,945 in student loans, the Wall Street Journal reported — a small sum compared with the $2 million loan balance he's expected to face in two decades.

Meru pays about $1,590 a month — 10% of his monthly income, but not enough to cover the interest. At this rate, his debt grows by $130 a day, according to the Journal.

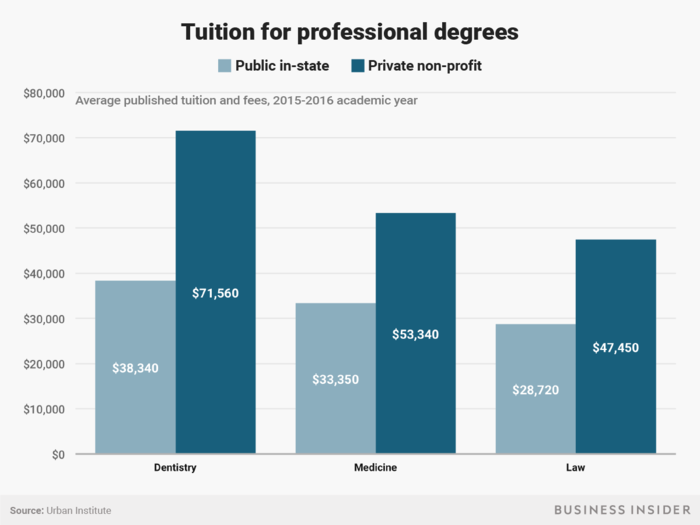

As the graph above shows, dental school is the most expensive professional-degree program in the US. During the 2015-16 school year, private nonprofit dental schools charged on average more than $71,000, while public in-state dental schools charged about $38,000, according to the Urban Institute.

Average tuition for private medical schools charged $53,240, and public in-state medical schools charged $28,720. Law-school tuition isn't far behind. Private law school cost $47,450 on average in 2016, and public in-state tuition was nearly $19,000 less.

While dentists, doctors, and lawyers make six-figure salaries, many have student debt that outweighs their income. Though dental school has the highest price tag on average for a professional degree, dentists aren't the highest-paid professionals. The median-earning dentist in the US makes $151,440 a year, and the median-earning physician makes at least $208,000, according to the Bureau of Labor Statistics.

Popular Right Now

Popular Keywords

Advertisement