Here are Goldman Sachs' top 10 market themes to watch in 2020

1. The beta view: Growth stabilization

2. Relative value: Tactical upside in cyclicals but quality is still on top

Goldman said that "with the notable exception of US equities, the 'up in quality' theme performed remarkably well across most markets in 2019." However, for 2020, the bank is still skeptical about "down in quality" theme, saying that it's unsure the theme can "get traction on a sustained basis."

"The growth reacceleration that our economists envision is certainly a welcome development from a sentiment standpoint, not least because it would further reduce recession concerns," the strategists said.

They added: "But we think it will likely fall short of reviving mid-cycle optimism: a key ingredient to boost the appetite for low quality segments."

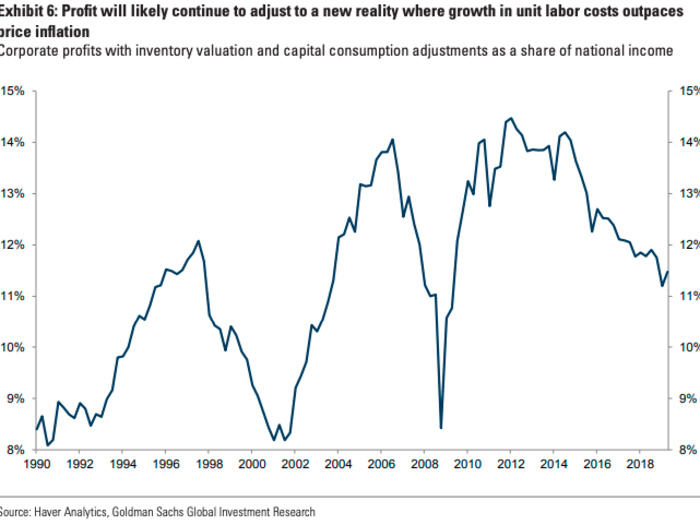

3. Earnings: Adjusting to flatter growth, with an eye on taxes

The bank lays out three key sub-themes for corporate earnings next year:

- While there will be a rebound, the path beyond that will be flatter and more subdued.

- A "more muted earnings growth environment" is likely to create situational pockets of risk in the credit market, especially for firms with low credit ratings.

- There will be considerable legislation risk for many areas of the stock market, especially leading up to the 2020 election.

Further, in reference to the chart above, Goldman said the following:

"While earnings growth is likely to rebound in 2020, the forward trajectory will be much flatter by post-crisis norms, as profits adjust to a new reality where growth in unit labor costs outpaces price inflation."

They continued: "This rather lackluster outlook for corporate profitability has fueled concerns over the broader macro outlook."

4. Rates: Baby bear market

Goldman said that in the 1990s bond yields rose "sharply" after mid-cycle adjustments from the Fed but after this year's rate cuts the strategists only expect a "mild upside" due to "muted global inflation pressures and on-hold central banks."

In reference to the chart above, the bank added: "Inflation in the US CPI Index has averaged 2.0% over the last 15 years, so a bigger break-out would imply that markets see future inflation higher than that in the recent past and/or that the inflation risk premium has moved up."

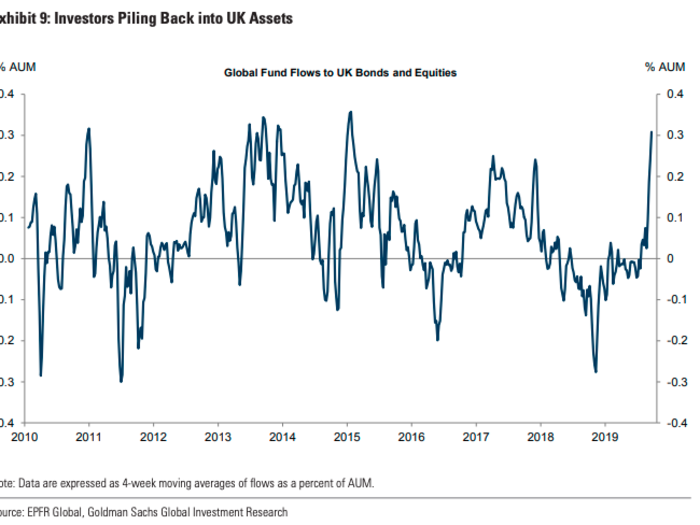

5. FX: A tale of two Dollars

"Normally the dollar weakens when global growth turns up and risk appetite improves," said the Goldman strategists. "But we think solid US growth and soft activity in China will prevent a big sell-off for now. "

When it comes to the pound, the firm expects it to appreciate as investors cover long-held underweight positions.

In reference to the chart above, Goldman said the following:

"Progress toward a Brexit deal resulted in a sharp rally in the Pound in October, likely on the back of short-covering by real money investors."

They added: "We think there is room for these flows to continue if the election results in a clear path forward for the Brexit process, making the Pound our preferred G10 FX long for Q1 2020."

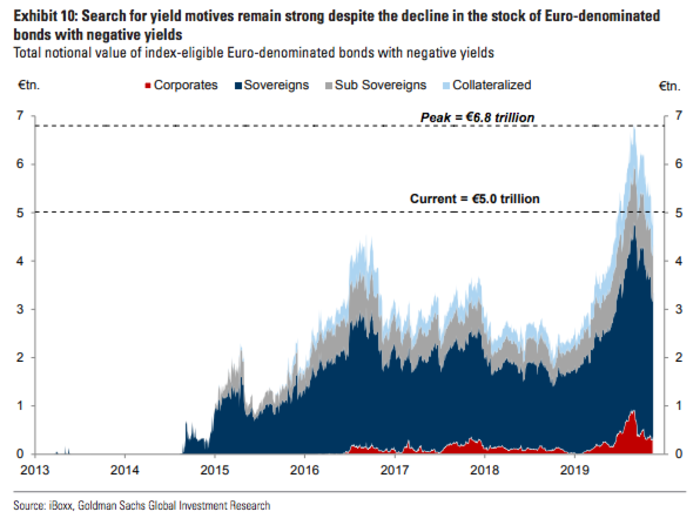

6. Europe: Don’t fight the ECB

In reference to the chart above, Goldman said the following: "Given still-strong search for yield motives and barring further growth weakness, we expect that carry will likely be the dominant component of expected returns."

The firm also mentioned that on a sovereign basis, it prefers Italy to Portugal.

7. China: When policy is doing just enough

The bank expects China's slowdown to continue in 2020, and says the manner in which this occurs will depend on the ongoing trade war with the US.

In reference to the chart above, Goldman said: "While the policy reaction function is firmly in reactive mode, support should still be forthcoming in order to limit downside risks, for instance if trade and industrial activity show no recovery from their recent trough."

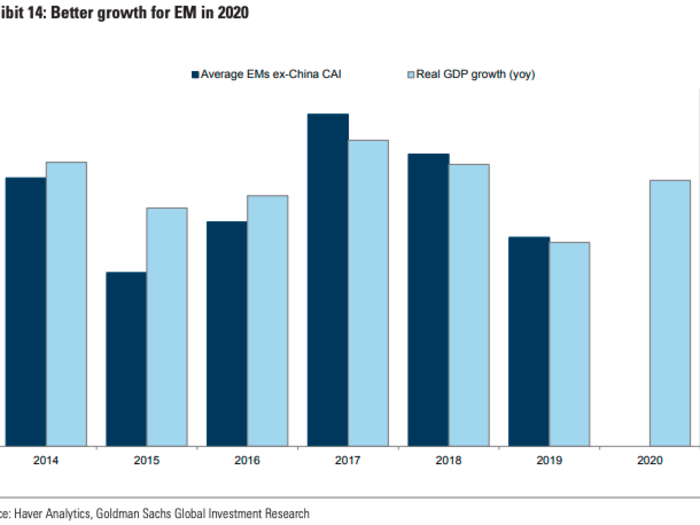

8. EM: Better growth, moderate returns

Goldman says it expects positive returns for emerging markets in 2020. In reference to the chart above, the firm said the following:

"The good news is that this cumulative easing in domestic financial conditions, continued low oil prices, and a better external growth picture in the US and Euro area in the year ahead, should allow EM growth to bounce up off the mat, especially if we see a more stable period in US-China trade tensions," the strategists said.

9. Commodities: Over-built, over-levered and over-polluted

Goldman said it expects oil prices to "remain stable and commodity forward curves to remain anchored near cost support."

The firm also laid out three key sub-themes in 2020:

- Deleveraging through a reduction of debt

- Consolidation of the old economy

- De-carbonization

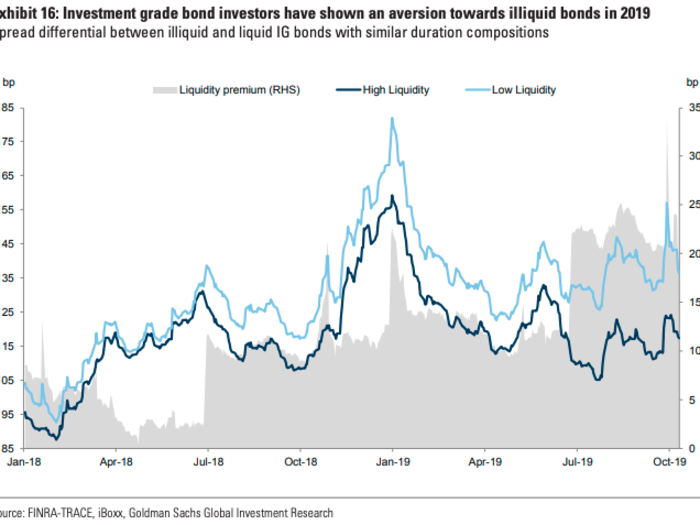

10. Market liquidity: The unknown known

"2019 has delivered fresh reminders of the fragility of fixed income markets' microstructure," the bank said in the note adding that in its view "the post-crisis deterioration in market liquidity conditions remains a major source of vulnerability for investors."

With that established, Goldman said that demand for illiquid risk will likely remain subdued, similar to how it's been throughout 2019.

In reference to the chart above, the firm said: "In the investment grade corporate bond market, investors have also shown a high level of risk aversion towards illiquid bonds, despite declining risk premia."

They continued: "The illiquidity premium in the investment grade market has been widening throughout the year, even as overall spread levels have tightened."

Popular Right Now

Popular Keywords

Advertisement