A Tsunami of money could be headed Tesla's way in the next year - and that's bad news for the bears

Despite Tesla's wild ride in 2018, the stock is flat.

Reviews of the Model 3 have been mostly positive.

I drove the Model 3 earlier this year and thought it was terrific. Other reviewers have been similarly impressed.

There have been some complaints about build quality, but there were complaints about build quality for the Model S and Model X when they first launched. And the majority of Model 3 buyers, panel gaps and other manufacturing issues aren't going to register — as long as the car serves up its Tesla-ness, looking cool and high-tech, owners will be delighted.

Even if stuff goes wrong, I suspect Tesla will continue what I like to think of as its infinity warranty and fix any and all problems.

Counter to what some Tesla super-enthusiasts believe, the company isn't going to take over the world. But if it continues to sell vehicles that customers adore, for the most part, the cash flow won't just increase, it will become very dependable.

Elon Musk is important, but is he really great?

Tesla often cites "great man risk" in its financial filing, addressing the possibility that losing Musk would be a disaster for the company.

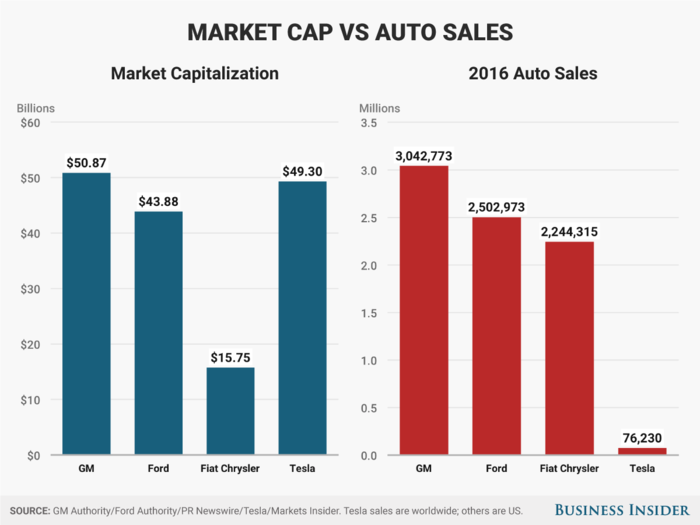

Musk just signed on for another 10 years, and the Tesla board has tied his pay package to a $650-billion market cap (it's just over $50 billion now), so his departure probably isn't imminent.

Folks who are exceptionally passionate about Tesla have a hard time separating Musk from the company — an investment in Tesla is a stake in Musk, the argument goes. And while that might have been true in Tesla's seat-of-the-pants early years, the company is 15 years old. If it can actually hit 250,000-500,000 in yearly Model 3 production and maintain Model S and X at 100,000, it's cash-flow pattern will be like any other significant automaker.

The business won't be about vision — it will be about balancing production against demand and trying to figure out to convert a gross-profit margin to a net margin.

This is why Musk's out-there conduct over the past six months hasn't really dented Tesla's stock price: he matters, but in the big picture, he isn't the entire company, which now has over 30,000 employees.

The Tesla machine now runs on its own.

Once they overcome their cash issues, carmakers can be very durable as businesses.

There haven't been many new car companies created in the past few decades; Tesla is pretty much the only one with major ambitions that's survived and prospered.

Little startups have risen and fallen, but all the big players have hung in there. Even the bankruptcies and bailouts of General Motors and Chrysler required the one-a-century obliteration of the US auto market — annual sales plunged from 17 million to 10 million in a year — and a credit crisis during the Great Recession.

Before that, dozens of global car companies rode out recession after recession. Even struggling automakers, such as Mitsubishi, have avoided being completely wiped out.

True, the companies all have better economics and more scale than Tesla. But Tesla is getting there. Again, if Tesla can stabilize its balance sheet, it will find that its relative domination of the luxury electric-car market is a big plus.

Tesla's pitch of it being a Silicon Valley tech company will also fade as it operates, beneficially, more like an automaker. Car companies aren't creamed overnight like software firms are; automobiles are big and expensive and designed to last for decades.

Software is cheap, if not free, and ephemeral. Excuse the esoteric pun, but much of Silicon Valley is a castle of sand, financially. Car companies are fortresses of iron.

When Tesla starts to build new factories, it will be investing in a multi-decade framework, a strategy that's justified in an industry where some plants built in the early 20th century are still operating. Take Ford. The company is 115 years old and made it through two world wars.

Or don't take Ford. Take Toyota: 80 years old, a giant that rose from the ashes of a world war.

Car companies are very, very tough customers.

Tesla trades on news, but eventually it will trade on fundamentals.

Tesla shares can swing up and down pretty wildly, but a lot of that action can be attributed to how much news the company generates, compared to the rest of the auto industry.

The recent obsessive focus on Model 3 output is a good example. Nobody in the "normal" car business pays any attention at all to production, unless for whatever reason big supply-demand mismatches development, leading to well-understood maneuvers around inventory and pricing.

Since the beginning of the year, however, Tesla-watchers have been keeping track of seemingly every single Model 3 that has rolled off the assembly line.

Tesla's unenthusiastic opposition to a possible unionization effort at its Fremont factory has also garnered outsized attention. Fremont was a union plant when it was jointly operated by GM and Toyota in the 1980s. It's reasonable to assume that it could go union again, given that California isn't a "right to work" state (all the new car factories that have been built in the past few decades have all been constructed in the US South, and none have been organized by the United Auto Workers).

It's no mystery, either, what a unionized Tesla would look like: the UAW would use the template contract it negotiated with the Detroit Big Three the last time around.

But the Tesla unionization effort is clearly going nowhere. It doesn't matter how you feel about organized labor — this is just a fact. Compare Fremont with Volkswagen's plant in Chattanooga, where a unionization effort failed in 2014. Back then, the effort moved through all the usual stages prior to the vote. Tesla may or may not be discouraging collective bargaining, but a serious unionization push hasn't managed to take shape yet.

So that news should obviously be discounted, at least until the organizers make better progress (which they might, as Tesla's business becomes more solid and sustainable).

A lot of hopes and dreams are invested in Tesla, so small fluctuations in sentiment can have major effects. Confidence and panic live side-by-side. But if Tesla can get hundreds of thousands of additional cars on the road, the signal will become louder and the noise will quiet. The company will become more boring. But serious investors will have fundamentals to concentrate on.

Popular Right Now

Popular Keywords

Advertisement