17 stocks about to rocket higher because of catalysts most investors are ignoring, according to UBS

Anadarko Petroleum

Citigroup

Ticker: C

Closing Price on 5/22: $71.08

UBS Price Target: $80 (+12.55%)

UBS View: "Citigroup shares have materially underperformed since 3Q17 and current valuations do not adequately capture gradually improving operating performance and continued capital optimization," said Saul Martinez. "Citigroup trades at just 1.15x TBV and 9.2x 19E earnings, discounts to all banks we cover."

Upcoming Catalysts: "In late June the Federal Reserve will announce the results of the stress test and approve or deny banks' capital plans for the 2018-2019 cycle. We expect Citigroup's capital plan to be approved, despite a tougher test this year and serve as confirmation of the bank's positive capital trajectory."

Source: UBS

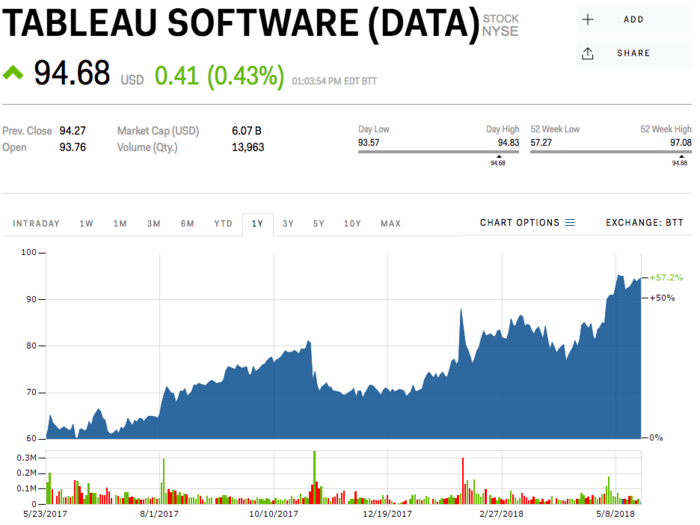

Tableau Software

Ticker: DATA

Closing Price on 5/22: $94.27

UBS Price Target: $114 (+21%)

UBS View: "Citigroup shares have materially underperformed since 3Q17 and current valuations do not adequately capture gradually improving operating performance and continued capital optimization," said Saul Martinez. "Citigroup trades at just 1.15x TBV and 9.2x 19E earnings, discounts to all banks we cover."

Upcoming Catalysts: "In late June the Federal Reserve will announce the results of the stress test and approve or deny banks' capital plans for the 2018-2019 cycle. We expect Citigroup's capital plan to be approved, despite a tougher test this year and serve as confirmation of the bank's positive capital trajectory."

Source: UBS

DowDuPont

Ticker: DWDP

Closing Price on 5/22: $67.47

UBS Price Target: $86 (+27.5%)

UBS View: "We believe current DWDP shares trade at a meaningful discount to the SOTP valuations for the DWDP SpinCos and present an attractive buying opportunity," said John Roberts. "We believe the company will be able to achieve >$3B in cost savings with potential further upside from combined growth opportunities."

Upcoming Catalysts: "Spinco separation progress and specifically New Dow (MaterialsCo) filing in 2H18, updates on synergy targets and capture, 2Q earnings."

Source: UBS

Ford Motor

Ticker: F

Closing Price on 5/22: $11.52

UBS Price Target: $15 (+30.2%)

UBS View: "We believe cycle risks is more than priced in as the stock is trading at 6.1x PE (9x historically) and 2.2x EBITDA (4.5x historically)," said Colin Langan. "Avoiding a decline in US sales and execution of the new CEO's strategic outlook should boost very low investor sentiment."

Upcoming Catalysts: "The company has recently started taking aggressive steps to address underperforming product lines including restructuring, product cuts, and partnerships and will be announcing action plans as ready. Investors seem to have deemphasized FY18 (low expectations are baked in) and are focused on LT strategy e.g. strategy color seen favorably by investors should help drive shares up."

Source: UBS

21st Century Fox

Ticker: FOXA

Closing Price on 5/22: $38.16

UBS Price Target: $48 (+26%)

UBS View: "We do not believe FOXA shares currently reflect the strong FCF generation potential of New Fox," said John Hodulik. "With affiliate revenues driving L/MSD EBITDA growth and a $1.5B tax shield, New Fox will have industry-leading FCF conversion, providing opportunities for value creation through a combination of debt reduction, accretive M&A and returning capital to shareholders."

Upcoming Catalysts: "Ruling on the AT&T/TWX trial is expected on June 12th. We believe the ruling will favor AT&T and be a positive catalyst for FOXA as Comcast is expected to make an all-cash premium offer* for FOXA's entertainment assets if AT&T/TWX passes regulatory approval."

*Comcast said Wednesday it was considering an all-cash bid for most of 21st Century Fox's assets to outbid Disney's previously announced offer.

Source: UBS

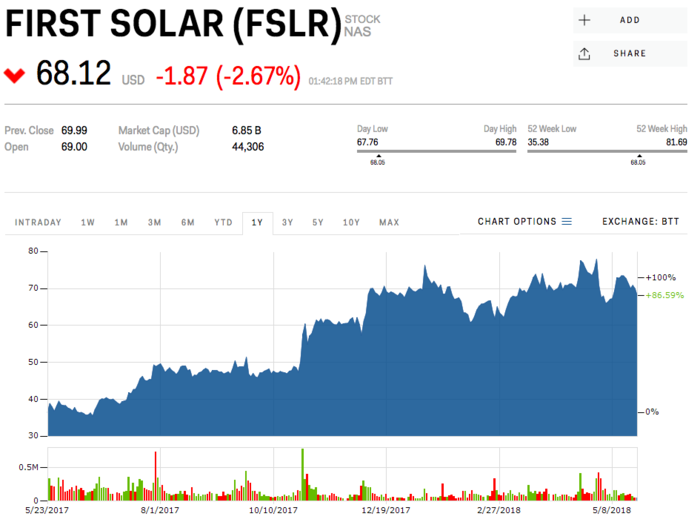

First Solar

Ticker: FSLR

Closing Price on 5/22: $69.99

UBS Price Target: $94 (+34.3%)

UBS View: "FSLR is our preferred name for exposure to solar module manufacturing," said Jon Windham. "We see the Series 6 module achieving a lower production cost relative to Chinese commodity modules, driving more sustainable earnings growth."

Upcoming Catalysts: "ITC announcement on import tariff exemption requests (late May); Growth in Series 6 bookings (2Q results); Malaysia factory ramping commercial Series 6 production (3Q18)."

Source: UBS

Halliburton

Ticker: HAL

Closing Price on 5/22: $53.24

UBS Price Target: $75 (+41%)

UBS View: "HAL is one of our top picks in 2018 given 1) its leading position in North America as the low-cost service provider, 2) earnings upside from pricing momentum, cost initiatives and lean cost structure, 3) global scale and earnings leverage in international markets, 4) compelling valuation, and 5) solid free cash flow, as well as a focus on returning capital to shareholders," said Angie Sedita.

Upcoming Catalysts: "Expected solid traction on incremental margins in Q2-18 with 'normalized' North American margins to reach 20% range by 2H-18, pressure pumping pricing momentum and announcements of contracts on new frac hp additions, International inflection as pricing slowly moves higher (late 2018) on steady activity gains)."

Source: UBS

Hatford Financial Services

Ticker: HIG

Closing Price on 5/22: $53.75

UBS Price Target: $64 (+19%)

UBS View: "We believe HIG's shares will re-rate to in line with peers (CB and TRV) following the sale of Talcott as ROE's continue to improve and it deploys the Talcott proceeds into accretive acquisitions and share buyback," said Brian Meredith. "Results will also benefit from continued improvement in personal auto and commercial lines underwriting margins, as well as more favorable loss reserve development."

Upcoming Catalysts: "Closing Talcott divestiture and announcing capital management plans."

Source: UBS

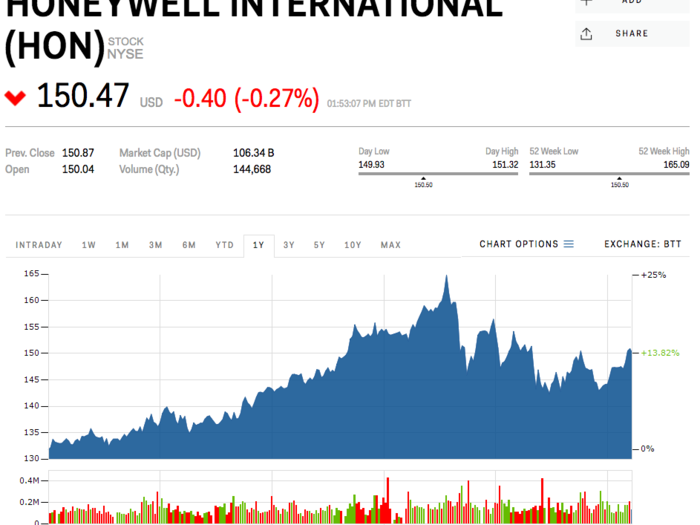

Honeywell

Ticker: HON

Closing Price on 5/22: $150.87

UBS Price Target: $180 (+19.3%)

UBS View: "We have followed Honeywell's turn-around and then turn-up over the last ~15 years under former CEO Dave Cote and his leadership team," said Steven Winoker. "Now, we believe HON is poised to take advantage of its cash position, step-up to growth and outperform under CEO Darius Adamczyk and his team. We believe HON is likely to beat 2018 targets given favorable end-market dynamics, robust growth initiatives, continued margin expansion (with high quality earnings) and tax policy benefits."

Upcoming Catalysts: "Completion of announced spin-offs of both Transportation and the Homes & Distribution business this year. HON is also sitting on up to $20B+ of potential capital deployment, which we expect to be positive catalyst."

Source: UBS

IAC InterActive

Ticker: IAC

Closing Price on 5/22: $148.70

UBS Price Target: $200 (+34.5%)

UBS View: "We believe IAC presents a favorable risk/reward from current levels based on our SOTP analysis," said Eric Sheridan. "Besides IAC's stakes in MTCH & ANGI, we view Vimeo as the key driver going forward, as we believe it has the ability to achieve higher than expected growth for longer than expected."

Upcoming Catalysts: "Quarterly earnings, Updates to ANGI/HomeAdvisor integration, Update on Dating on Facebook for Match Group, New product/service announcements for Vimeo, M&A."

Source: UBS

Lennar Corporation

Ticker: LEN

Closing Price on 5/22: $50.87

UBS Price Target: $92 (+81%)

UBS View: "We’re believers in the continuation of the overall housing cycle and Lennar’s specific opportunities with its recent acquisition of CalAtlantic, with the potential to reap the full $365 million of expense savings, and the improved absorption at the CalAtlantic communities," said Daniel Oppenheim. "We view LEN as particularly attractive, as it trades at just 1.1x 2019E book value, despite its above-average and rising ROE."

Upcoming Catalysts: "1) Fiscal 2Q earnings in late June will offer an update on the progress of converting the CalAtlantic communities to Lennar communities, and we expect upside to Lennar’s projection of 3% order growth in 2Q, and would expect expectations for orders in subsequent quarters to rise. 2) continued strength in overall industry trends, with strong pricing and low existing inventory likely seen with the April existing home sale release (May 24th)."

Source: UBS

Mondelez International

Ticker: MDLZ

Closing Price on 5/22: $39.43

UBS Price Target: $52 (+32%)

UBS View: "We’re believers in the continuation of the overall housing cycle and Lennar’s specific opportunities with its recent acquisition of CalAtlantic, with the potential to reap the full $365 million of expense savings, and the improved absorption at the CalAtlantic communities," said Daniel Oppenheim. "We view LEN as particularly attractive, as it trades at just 1.1x 2019E book value, despite its above-average and rising ROE."

Upcoming Catalysts: "1) Fiscal 2Q earnings in late June will offer an update on the progress of converting the CalAtlantic communities to Lennar communities, and we expect upside to Lennar’s projection of 3% order growth in 2Q, and would expect expectations for orders in subsequent quarters to rise. 2) continued strength in overall industry trends, with strong pricing and low existing inventory likely seen with the April existing home sale release (May 24th)."

Source: UBS

Marvell Technology Group

Ticker: MRVL

Closing Price on 5/22: $21.92

UBS Price Target: $38 (+73.4%)

UBS View: "We think MRVL is a Buy because the market is underestimating several key dynamics of the company For one, we think the management can unlock significant value post CAVM integration that the market is not factoring into estimates," said Timothy Arcuri.

Upcoming Catalysts: "FQ1'19 Financial Results (May 31, 2018); Completion of Cavium Acquisition (est. mid-2018)."

Source: UBS

Royal Caribbean Cruises

Ticker: RCL

Closing Price on 5/22: $107.51

UBS Price Target: $147 (+37%)

UBS View: "We are overweight the cruise sector with a Buy rating on RCL," said Robin Farley. "We believe Q3 will address many investor concerns - it will show pricing growth in the most core market even with high supply growth. Looking into the next 12 months, we see cruise demand growing, with supply growing in line with historical averages."

Upcoming Catalysts: "Cruise seller calls, Q2 earnings and more importantly Q3 earnings when cruise lines climb the wall of worry for the year."

Source: UBS

Targa Resources

Ticker: TRGP

Closing Price on 5/22: $48.53

UBS Price Target: $59 (+22%)

UBS View: "We continue to like TRGP as is presents one of best growth profiles in our coverage universe given its position in the Permian," said Shneur Gershuni. "PXD a top customer of TRGP has talked about the strength of its position in the Permian and the acquisition of Outrigger further expanded TRGP's footprint into the Delaware into a higher capital return area of the basin."

Upcoming Catalysts: "Asset sales in particular as it could help remove funding overhang; 2Q18 Earnings could illustrate operating leverage of new assets recently brought into service."

Source: UBS

United Continental Holdings

Ticker: UAL

Closing Price on 5/22: $69.99

UBS Price Target: $85 (+21.4%)

UBS View: "We continue to like TRGP as is presents one of best growth profiles in our coverage universe given its position in the Permian," said Shneur Gershuni. "PXD a top customer of TRGP has talked about the strength of its position in the Permian and the acquisition of Outrigger further expanded TRGP's footprint into the Delaware into a higher capital return area of the basin."

Upcoming Catalysts: "Asset sales in particular as it could help remove funding overhang; 2Q18 Earnings could illustrate operating leverage of new assets recently brought into service."

Source: UBS

Voya Financial

Ticker: VOYA

Closing Price on 5/22: $53.98

UBS Price Target: $63 (+17%)

UBS View: "Post the sale of the company's Closed Block of Variable Annuities (CBVA) and ongoing Annuities business, we view VOYA as a smaller version of Principal Financial (domestically) with stronger FCF generation given benefits from the DTA," said John Nadel. "The combination of organic growth, expense saves and robust capital management should result in VOYA's EPS growth outpacing most peers (25%+ in 2019), with ROE improvement to ~16%. We expect this to drive further re-rating to at least 11x P/E ex. the value of tax assets (vs. 9x our 2019E EPS on that basis now)."

Upcoming Catalysts: "1) The company expects to close the sale of CBVA in 2Q/3Q18. 2) Investor Day (capital allocation), 3) strategic Review of Individual Life business."

Source: UBS

Popular Right Now

Popular Keywords

Advertisement