The last quarter of 2014 was a correction phase wherein the Smart Phone market declined by 4% while the Feature Phone market plummeted by approximately 14% over Q3 2014.The overall mobile phone market stood at 64.3 million units in

The study conducted by

Feature Phone to Smart Phone migration trend is clearly visible. Smart Phones formed a healthy 35% of the overall mobile business in Q4 2014, which is up by 13% from a year ago i.e. Q4 2013.

“Smart Phone vendors are quick in gauging the consumer demand for 4G handsets. In percentage terms, 4G handsets are still in single digit. But vendors who are not yet ready with the 4G portfolio are likely to miss the next wave of Smart Phone growth story.” says Karan Thakkar, Senior Market Analyst, IDC India.

Shipment contribution from vendors like Asus, Microsoft and

“In the current market scenario there is a drive in demand for products pitched with high specification at low price points. This trend is likely to continue over the next 4 to 6 quarters, post which consumers are expected to turn back to the handset vendors who charge premium for quality,” added Thakkar.

Micromax: The brand witnessed an inventory correction in Q4 2014 owing to high inventories pumped into the channels during the previous quarter.

Intex: Intex did not feature in the top five Smart Phone vendor list until Q3 2014, but the swift pace at which brand has clinched on to 3rd spot is commendable. The retail presence of the brand has seen more than a twofold increase. Focused product launches and media advertisements worked well for the brand.

Lava: Lava has slipped to the 4th spot. However, the brand remains consistent and stable with a good amount of visibility of its distributors.

Xiamoi: Xiaomi’s “online only” strategy has paid off well. Q4 was the first complete quarter for the brand. Even with minor hiccups like temporary ban on a particular handset model, the brand made it to top 5 Smart Phone vendor list.

The overall mobile phone market shrank by 11% qurter on quarter. The steep fall can be attributed majorly to the feature phone category. While Karbonn did not make it to the top five vendor list in Smart Phone category, it continues to remain strong in the Feature Phone segment.

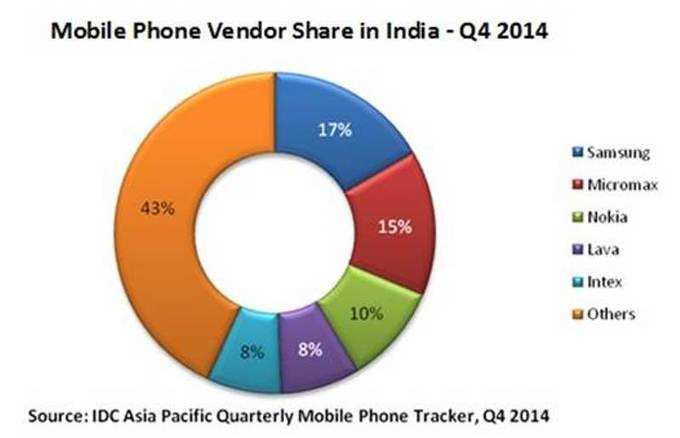

A quick look at the overall vendor share shows the strong presence vendors have in the feature phone market to make it in the top five list at an overall level.

IDC further anticipates a sluggish Q1 2015. However few global vendors which were in the inventory correction phase until now are likely to exhibit big shipment numbers starting Q1.

“Operators are gearing up for 4G network rollout. For vendors and ecosystem partners, greater emphasis on 4G enabled handsets at competitive price points will be the order of the day. End-users’ desire to upgrade and keeping abreast with the latest technology, will continue to drive a strong growth for the Smart Phone market in CY 2015,” says