4 reasons it will take a long time for US home supply to meet the extraordinary demand, according to BofA

Ben Winck

- The housing market is on its way to normalization, but it'll take a while, Bank of America said.

- Demand is holding strong, but price pressures are intensifying and building costs are up.

- Here are four signals that it will take a while to balance out the market, according to BofA.

The housing market will normalize, but Bank of America advises against holding your breath about it happening soon.

The market has been running red hot for roughly one year. The Federal Reserve's March 2020 rate cuts dragged mortgage rates to historic lows and spurred a nationwide buying spree. Sales accelerated, but builders failed to keep up. By the end of 2020, the US home supply sat just above record lows.

Building activity has picked up somewhat this year, but Americans' outsize demand is still handily exceeding the national supply. And it's unlikely that the two will balance out anytime soon, Bank of America economists led by Michelle Meyer said Monday.

The recent dip in existing home sales is only the start of a "long journey" to restore market equilibrium, according to the team. A handful of trends suggest that while the market is set to cool, buyers will outstrip sellers for the foreseeable future.

Here are the four signals that point to a prolonged recovery for US home supply, according to the bank.

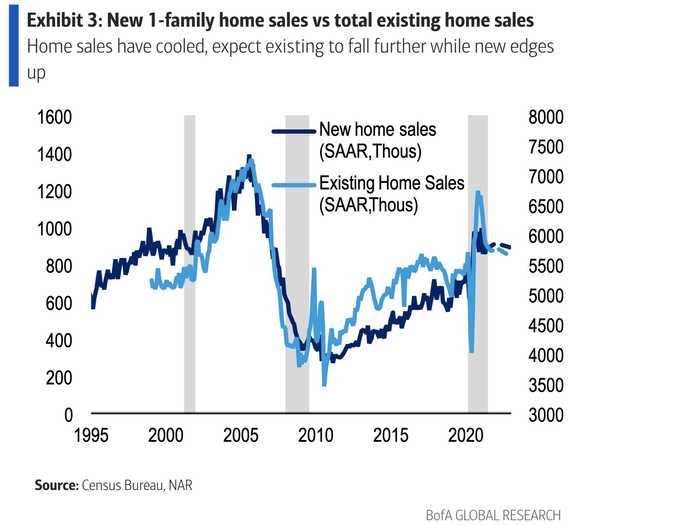

1. Demand is holding strong

While sales of previously owned homes have slowed, demand seems to be shifting elsewhere. Sales of new homes plateaued in April compared to a continued decline for existing home purchases. Home starts also remained elevated in April, suggesting demand for new construction is on the upswing.

Risks for existing home sales skew to the downside as tight inventories and soaring prices cut into affordability, BofA said. But that decline could easily be offset by buying elsewhere in the market.

"New home sales may grind higher as these supply challenges funnel demand towards new construction," the team said.

Homebuilding data support such a demand shift. Housing starts declined in April, but the bank expects the reading to be a bump in the road as building accelerates. Permits have also remained elevated. Taken together, the trends point to "robust underlying demand for new residential construction," the economists said.

2. Affordability pressures intensified

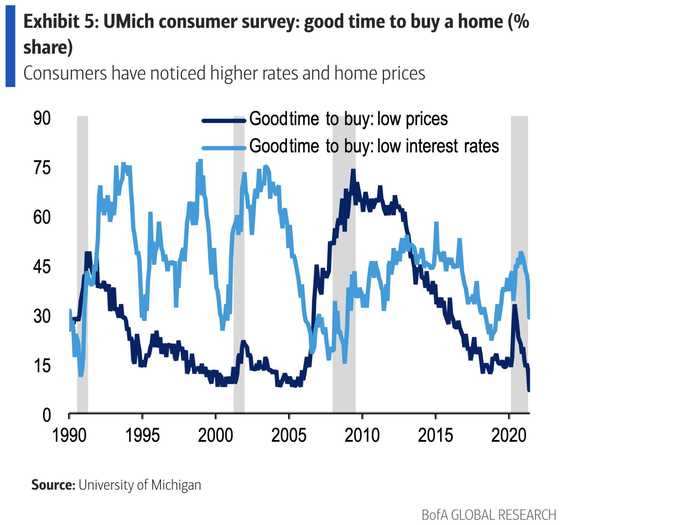

It's likely that market demand needs to fall for supply to catch up, but surveys suggest buying plans are nosediving rather than steadily declining.

The University of Michigan's May consumer sentiment survey found just 7% of Americans said it was a good time to buy due to low prices. The share of people saying it was a good time to buy due to low interest rates fell to 29%. That share is set to drop as the economy recovers further and rates climb

Separately, Fannie Mae's national survey found the share of respondents saying it was a good time to buy fell to -1%, the lowest level since 2010.

The plunge in buying attitudes butts heads with a surge in homebuilder sentiment. The National Association of Homebuilders' housing index sits at its highest levels since at least 1985.

With discouraged buyers listing affordability as the main barrier to homeownership, it may take some time before builder optimism and rebounding construction can alleviate price pressures.

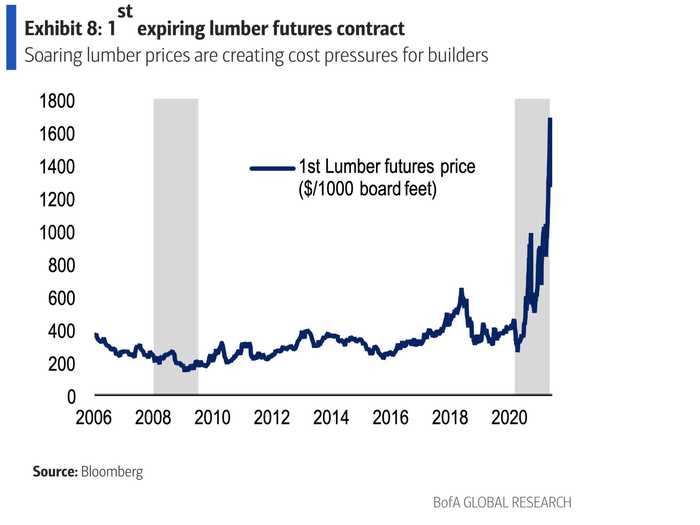

3. Sky-high costs are hindering construction

The homebuilding rebound isn't a certainty. Although builders are the most optimistic they've been in decades, soaring costs are slowing attempts to shore-up supply and cut down on price growth.

Lumber is perhaps the largest driver. Prices surged through April and May to a peak of $1,686 per 1,000 board feet. Though the rally has reversed somewhat, futures prices are still hovering at about $1,400. That compares to pre-pandemic levels of $400.

All told, the lumber rally added nearly $36,000 to the average new home price from April 2020 to April 2021, BofA said.

The leap is also affecting what kinds of homes are being built. Contractors are focusing on building higher-priced units where elevated materials costs are better offset by selling prices.

The share of homes selling for less than $300,000 dropped to an all-time low of 27% in April. Meanwhile, homes that sold for more than $500,000 made up 26% of sales, the highest since 2002.

4. There's plenty of progress to be made

Perhaps the biggest obstacle to normalizing the market is the size of the supply-demand gap. The imbalance is most simply summarized by home-price inflation, which has risen to its fastest levels since the mid-2000s bubble.

BofA sees price growth easing as construction bounces back. Yet the team's projections still see elevated price inflation lasting through 2022. The S&P CoreLogic Case-Shiller price index will end the year at 12% before falling to 6% next year, the economists said. That compares to a pre-pandemic norm of about 5%.

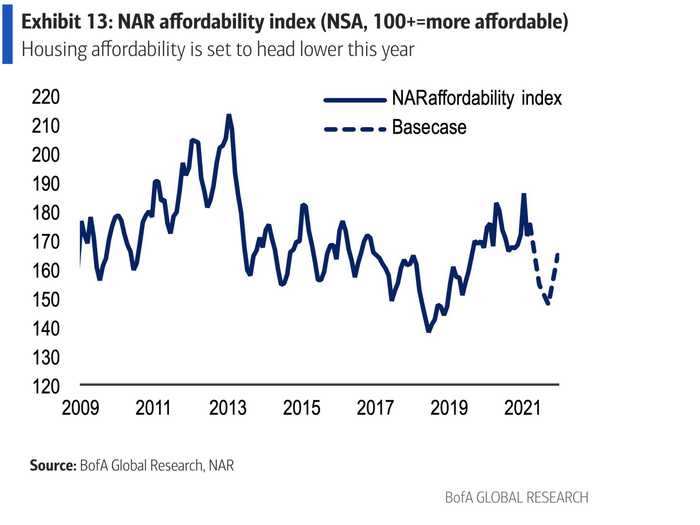

Separately, BofA expects affordability to fall even further before reversing course. The National Association of Realtors' affordability index will tumble throughout 2021 as stimulus that lifted incomes during the pandemic dries up. Rising rates will also cut into affordability just as builders look to balance out the market, the team said.

READ MORE ARTICLES ON

Popular Right Now

Popular Keywords

Advertisement