This couple retired at 43 to travel Europe full time on $18,000 a year - here's the spreadsheet that helped them get there

1. Variables

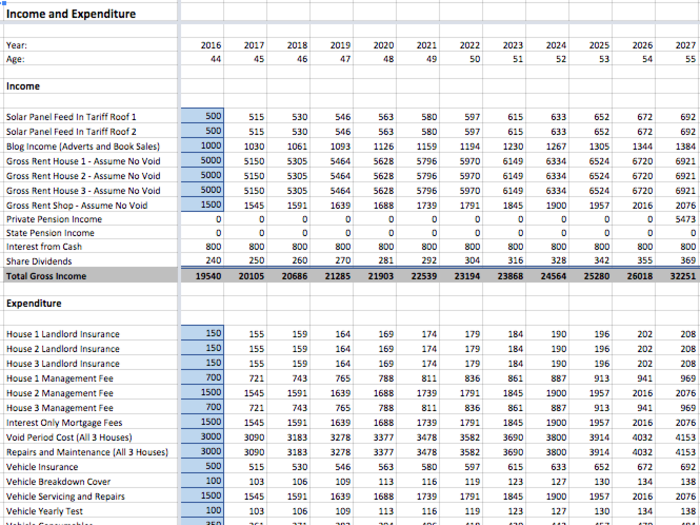

2. Income and expenditure

This spreadsheet, which lists their income and expenses, represents the viability of retiring early, Jason said. The row labeled "variance" at the bottom indicates what should be left from income streams after paying living expenses.

The numbers here are for example purposes only, and don't reflect the Buckleys' own finances.

"On our version of the spreadsheet the numbers are green, but they only turned green once we'd built up enough passive income and reduced our costs," Jason said. For example, last year their expenditures were £7,000 (~ $8,554) below their income, part of which came from "one-offs" like selling a car.

"We could easily get our costs down to less than £10,000 (~ $12,200) a year doing this, but we'd miss out on too much," Jason said.

The Buckleys have 11 years until their private pensions — essentially the UK version of a 401(k) — will start paying out. The amount will increase when they reach age 67, although Jason says they'll only be eligible for partial state pensions, comparable to social security in the US.

To cover expenses prior to that, they've invested in residential property, shares, and roof-mounted solar panels, which generate government-paid feed in tariff payments. To maintain passive income from the rented-out properties, the Buckleys pay local management agents to service their tenants.

Jason and Julie are UK residents, so the national health service will cover any costs related to health, Jason said.

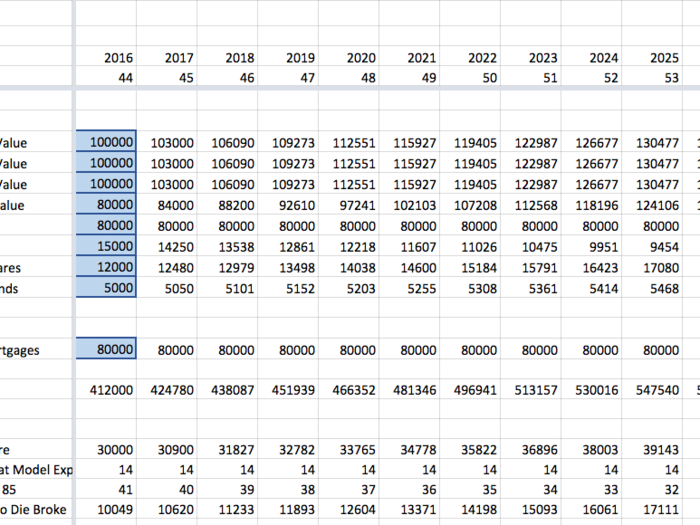

For both this sheet and the next, the Buckleys include estimations through age 85 in the year 2057.

3. Net worth

This spreadsheet represents how much the Buckleys would have in cash if they sold everything they own and paid off all liabilities. The model at the bottom shows how many years they could live for if they "liquidate everything and just started burning through the cash."

But, Jason said, for the next decade they plan to restrict themselves to just living on the cash flowing from investments and ignore any capital or market increases in the value of properties, pensions, and shares.

"At some point we'll need to increase our spending rate significantly in order to ensure we die broke, as we have no children to leave money to," Jason said. "In other words, instead of taking a 'pay cut' when we hit 'retirement age,' we'll get a pay increase."

If you're aiming to achieve early retirement, Jason and Julie suggest educating yourself financially and putting your plan on paper, tracking spending and cutting all unnecessary costs, and investing.

"As your costs come down, and income from your investments gets re-invested in more investments, at some point you will experience the bewildering and joyful moment when your wealth starts to spiral upwards," Jason said. "At that point your freedom is all but inevitable."

Popular Right Now

Popular Keywords

Advertisement