I became a millionaire in 10 years without picking stocks, and here are the questions people ask

I became a millionaire in 10 years without picking stocks, and here are the questions people ask

I became a millionaire in 10 years without picking stocks, and here are the questions people ask

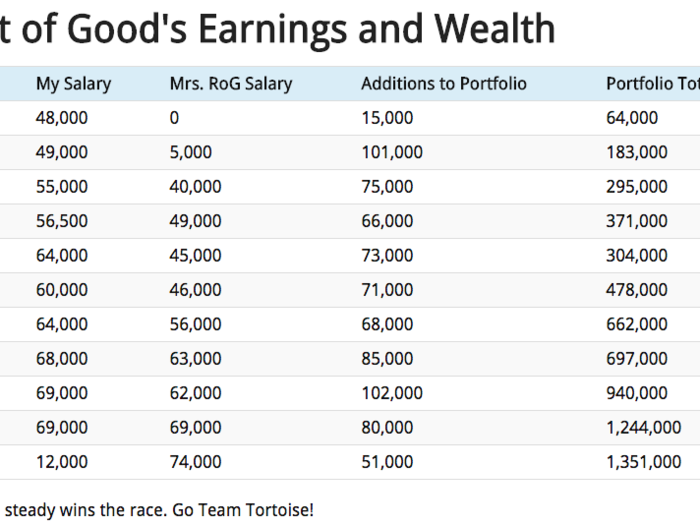

How can you save $75,000 on a $95,000 salary?

Some commented that the annual salaries don't make sense compared to the "Additions to Portfolio" shown in the table. Take 2006, for example. We made $95,000 yet managed to add $75,000 to the portfolio. Not included in our $95,000 combined salaries were 401k matches of maybe $8,000 (records are fuzzy here) plus another $8,000 to $10,000 in profit sharing into my Employee Stock Ownership Plan. I treated the 401k matches and ESOP contributions as "additions to portfolio" but they aren't included in our salaries since I didn't want to give an inflated sense of how much we actually made at pretty ordinary jobs (for those with college degrees in engineering or business).

In 2006, our combined "grossed up" salaries including the 401k matches and ESOP contributions were closer to $115,000 (again, my records are fuzzy beyond the straight salaries). This means we spent about $40,000 between payroll taxes, income taxes, and living expenses. $40,000 is a lot more realistic for all that compared to $20,000 if you just glance at the table!

Nationally, the median household income is somewhere around $50,000 to $60,000 per year. In other words, we were living a lifestyle just a little below median while enjoying salaries and benefits significantly more than the median (but still comfortably middle class ,I would argue).

Regarding taxes, we paid very little due to some hard core tax planning efforts, three kids, and plain old luck. In the last year that both of us worked, our combined incomes were just under $150,000 yet we only paid $150 in federal income tax. We maxed out 401k's, IRAs, and an HSA. As a government employee, I also had access to a 457 and a pension plan so I was able to contribute and deduct another $20,000 beyond what most employees can.

If you think what we did is impossible, just remember that North Carolina is still accepting new immigrants from other states, and the state government continues to hire people all the time. However, I would suggest working for a different employer if top pay is a priority!

I became a millionaire in 10 years without picking stocks, and here are the questions people ask

Does our lifestyle suck?

One Business Insider commenter, Nutjobmoron, said: "Also, what is his life of 'retirement' like now. He can only afford to get up, sit on the couch and eat pasta. No golf, no boating, no beemer and no expensive steak dinners."

Another commenter answered Nutjobmoron very eloquently:

The fact that he doesn't have a boat, or go golfing or drive a beemer is the exact reason he is able to do this. Might not be the life you want, but it is the life he has and he seems super happy with it.

But you're right — dude gets to spend time with his family and travel whenever he wants, doesn't even have to go to work every day. Such a loser.

That sums it up well. We didn't spend money on all that stuff which allowed us to save tons toward our financial independence.

We don't own a boat and probably never will. Preferring to rent instead of own, we do go on a cruise (a very big boat) once or twice per year. The past two years we've taken multi-week international vacations including a two and a half week road trip to Canada last year and a seven week trip to Mexico this year. Leaving the couch and my plate of pasta was required for all of these trips. We did eat quite a bit of steak dinners while on these trips.

I acknowledge it's impossible to dine at fancy steakhouses every night, own a yacht, a fleet of late model German imports, and a mansion while living on $30,000 to $40,000 per year. But that lifestyle was never our goal and isn't something we would get a lot of value out of anyway.

Our 15-year-old Hondas run very well. Our house is perfect for our family of five and in a convenient location. We budget enough to allow some pretty crazy travel (considering that we have three kids). We also enjoy the freedom of not needing to work.

I became a millionaire in 10 years without picking stocks, and here are the questions people ask

Accessing retirement funds before age 59.5

One commenter asked how we will withdraw from our investment portfolio in our 30s when there's a penalty for withdrawals before age 59.5.

Our strategy involves a number of different sources of funds with different tax treatment.

We have a taxable brokerage account with over $300,000 in it that will cover the first ten or so years of early retirement living expenses.

While we are spending down our brokerage account, we are setting up a Roth IRA Conversion Ladder. It's a method to convert funds in a Traditional IRA to a Roth IRA. Five years after the Roth conversion, it's possible to withdraw the amounts converted, penalty-free. By the time we deplete our brokerage account in around ten years, we should have at least a few years of living expenses sitting in our Roths ready to be withdrawn as necessary.

In addition to the taxable brokerage account and the Roth IRA Conversion Ladder, we have two other sources of penalty free funds. We have two years of living expenses in a 457 account that can be withdrawn penalty free any time. We also have $60,000 in a health savings account that can be withdrawn at any time to pay for medical bills.

This took some planning to set up, but it's going to allow us to live off our various investment and retirement accounts for the next several decades until we hit age 59.5 and all the early withdrawal penalties disappear.

If you have more questions, I regularly write about how we manage our money on my website, Root of Good.

This post was originally published on Root of Good.

Popular Right Now

Advertisement