Capital gains tax rates: How to calculate them and tips on how to minimize what you owe

- The capital gains tax rate applies to profits on investments.

- If you owned an asset for over one year before selling, it's a long-term capital gain and taxed at a reduced rate.

- Investing in tax-advantaged accounts, donating appreciated stock, and using capital losses can help you minimize or even avoid capital gains taxes.

Capital gains are profits. Specifically, the profits you make from selling capital assets, such as stocks, bonds, real estate, and other investments and collectibles.

When you sell a capital asset at a price higher than its "basis," you're generally required to report a capital gain on your federal income tax return. Basis means the asset's purchase price, plus any money you reinvested or put into improving it.

The tax rate you'll pay on capital gains can be lower than the rate you'll pay on other types of income, such as salary or profit from a business. But the amount you'll pay depends on how long you held onto the asset before selling it.

Let's examine how the capital gains tax rate actually works for individuals.

What is the capital gains tax rate?

Actually, there are two capital gains tax rates, reflecting the two types of capital gains: short-term and long-term.

- You have a short-term capital gain if you hold an asset for one year (365 days) or less.

- You have a long-term capital gain if you hold an asset for longer than one year.

The clock begins ticking on the day after you buy the asset, up to and including the day you sell it.

Short-term capital gains don't benefit from a special tax rate

Short-term capital gains are taxed at ordinary income tax rates, up to 37%. The rate you'll pay depends on your filing status and total taxable income for the year.

To illustrate, say you are a single taxpayer in 2020 with wages of $85,000, short-term capital gains of $10,000, and claim the standard deduction ($12,400). Your taxable income is $82,600 ($85,000 + $10,000 - $12,400), putting you in the 22% tax bracket for 2020.

However, you don't pay 22% on all your income, only income over $40,125 (the top of the 12% tax bracket). You calculate your tax as follows:

- 10% of the first $9,875 of income: $988

- 12% of the next $30,250 of income: $3,630

- 22% of the last $42,475 of income: $9,345

For your 2020 tax return (filed in 2021), your tax bill is roughly $13,963.

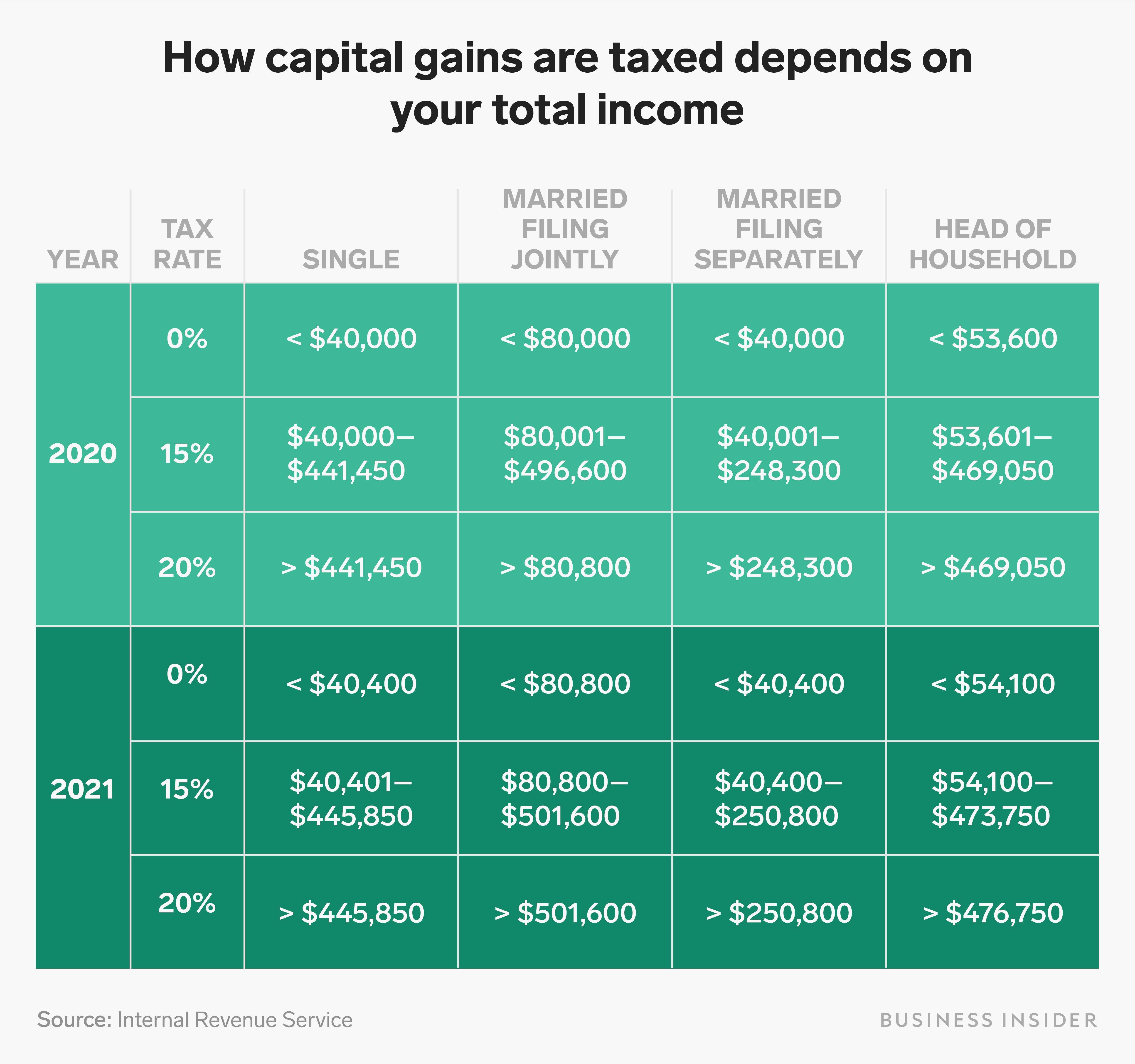

Long-term capital gains are taxed at preferential rates

If you manage to hold onto your investment for more than one year (365 days), you can benefit from a reduced tax rate on your capital gains. Long-term capital gains are taxed at preferential rates, up to 20%. The rate you'll pay depends on your filing status and total taxable income for the year.

Returning to the earlier example, say your $10,000 capital gain qualified for long-term treatment. Your total taxable income is still $82,600. However, your tax calculation is different.

Your ordinary income is $72,600 ($85,000 of wages less your $12,400 standard deduction). You are still in the 22% tax bracket, and calculate your ordinary income tax as follows:

- 10% of the first $9,875 of income: $988

- 12% of the next $30,250 of income: $3,630

- 22% of the last $32,475 of income: $7,145

For long-term capital gains, you fall into the 15% tax bracket, so you calculate your long-term capital gains tax as 15% of $10,000: $1,500.

For 2020, your tax bill is roughly $13,263.

Having your capital gain taxed at long-term rather than short-term rates results in $700 of tax savings.

The net investment income tax on capital gains

Capital gains taxes aren't the only ones investors have to worry about, though.

The net investment income tax (NIIT) is a separate tax, but it can impact the tax you pay on capital gains as well as other types of investment income.

The NIIT imposes a 3.8% tax on the lesser of your net investment income or the amount by which your modified adjusted gross income (MAGI) exceeds a certain amount.

Investment income includes:

- Distributions from annuities

- Interest

- Dividends

- Capital gains

- Income from passive activities

- Rents

- Royalties

The total of your investment income is reduced by any deductions related to investments, such as investment interest expense and expenses related to rental property or royalties, to arrive at net investment income.

The NIIT only applies if your MAGI exceeds the threshold amount for your filing status. Those thresholds for 2020 are:

- $200,000 for single filers and head of household

- $250,000 for married couples filing jointly

- $125,000 for married couples filing separately

If your income exceeds the threshold, you calculate NIIT on Form 8960 and file it along with your Form 1040 tax return.

How to avoid capital gains tax

There are several ways to minimize or even avoid capital gains taxes.

1. Hold on to assets for more than one year

Whenever possible, hold onto your investments for more than a year, so they qualify for long-term capital gains rates.

2. Invest in tax-advantaged accounts

Tax-advantaged accounts, such as IRAs and 401(k)s, allow your investments to grow on a tax-deferred or even tax-free basis. You don't have to pay capital gains on any sales within these accounts in the year they occur.

With a traditional IRA or 401(k), you'll pay taxes when you take distributions from the account. No tax is due on Roth IRA distributions, as long as you've followed the withdrawal rules.

3. Take advantage of the home sale exclusion

When you sell your home, you get to exclude a certain amount of profit from the sale from your taxable income. That limit is $250,000 for single filers and $500,000 for married couples filing jointly. To qualify, you must have owned the home and used it as your primary residence for at least two of the last five years. You can take advantage of this exclusion once every two years.

4. Use capital losses to offset capital gains

When to sell a capital asset for less than your basis, you have a capital loss. You can use those losses to offset capital gains. If your capital losses are greater than your capital gains, you can use up to $3,000 to offset ordinary income. Any remaining losses can be carried forward and used to offset capital gains in future tax years.

5. Donate appreciated assets

Feeling philanthropic? Rather than selling stock, paying taxes on the capital gains, and then donating cash to your favorite charity, consider donating the stock directly to the organization. This strategy can reduce your tax bill in two ways.

First, you can avoid the capital gains tax you would have owed if you sold the stock. Second, if you itemize deductions, you can claim a charitable deduction for the donated stock's fair market value.

The financial takeaway

Taxes shouldn't be your sole concern when deciding when and where to invest. However, knowing how capital gains are taxed and taking advantage of a few tax-saving strategies can help you reduce the bite of capital gains tax and keep more investment profits in your pocket.

Consult with a financial or tax professional who can help you manage your investments and make a plan for selling appreciated assets in a way that makes the most sense for you.