Learn everything you need to know about personal finance from 11 simple sketches

Your financial plan can be as short as a single page.

You can't make one, though, until you've pinpointed why you care about money.

Why is money important to you? It's a simple question, but it's not always easy to answer.

It's also a question that feels more appropriate for a therapy session, not financial planning. However, this question helps reveal your values.

Those values then become the checkpoint for your financial plan because you can't make a plan if you don't know why you're planning.

Plus, without knowing your "why," financial decisions can feel incredibly complex. But once you have your answer, you gain the clarity to know which strategies will work best for your particular situation.

Saving without a purpose isn't going to work.

When you plan a trip, you decide where to go first.

Then, you weigh your travel options, like whether to fly or drive. After all, driving won't get you to Paris if you're starting in New York.

You need to use the same logic with money. Yes, you may want to save money, but for what purpose?

Your one-page plan reminds you of "why" you're saving money, helps you weigh the different options, and makes it easier identify the best path for getting you where you want to go financially.

Your net worth is your starting point for everything you want to accomplish.

Where do you stand financially? You're not alone if you don't know the answer. But you need this information to make other financial decisions.

Luckily, finding the answer only requires some simple math and a piece of paper. You're going to create a balance sheet.

On the left side, list all your assets in detail: bank accounts, the fair market value of your home, and any savings.

On the right side, list all your liabilities: credit card debt, mortgages, and school loans. Then, add up all your assets and subtract your liabilities. You now know your net worth.

A budget tells you how much money you have to spend the way you want.

Budgeting and flossing: both insanely important, super simple, and for many of us, nonstarters.

There's a reason for that. Many of us view budgeting as a punishment. Plus, we think it's boring, and we're sure we already know how we're spending our money (or we don't really want to know).

But budgeting isn't about punishing ourselves, and it's not just about tracking numbers. When we budget, we build awareness, and awareness helps us know if our spending leaves us with enough money for the things that matter most.

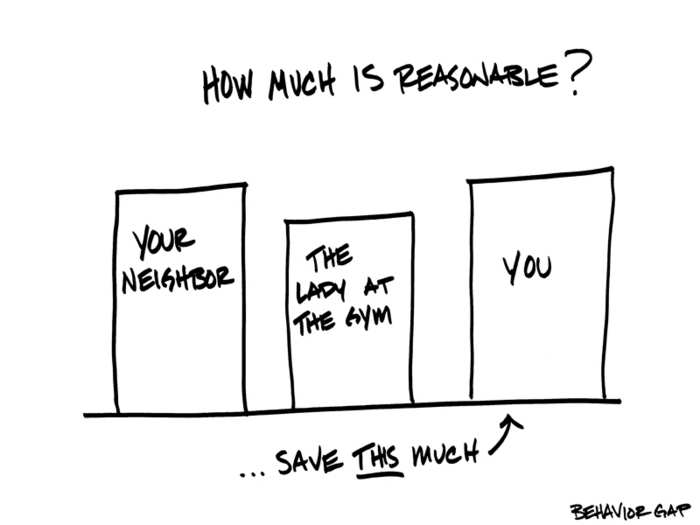

There's no single answer to how much you should save.

When it comes to saving money, people get hung up on the number.

Should you save 15% of your paycheck? Five percent? Twenty percent? The number matters less than you might think.

Start with saving as much as you reasonably can. Your definition of reasonable may not match your neighbor's and that's O.K.

Instead of stressing about a random percentage, focus on what you can save given your commitments. What's reasonable in your thirties probably wasn't reasonable in your twenties.

Giving yourself permission to save reasonably means continuing to save for the future without denying yourself the things that keep you healthy, happy, and sane today.

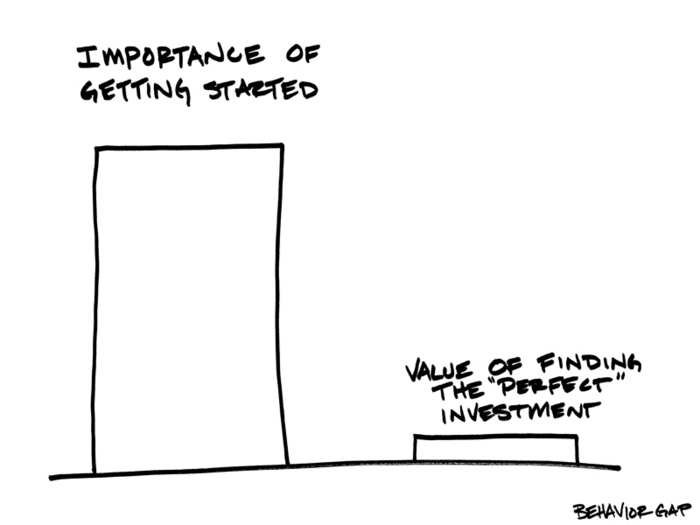

It's never too late to get smart with your money.

It's never too late to start saving or investing.

Maybe you never started saving because you were paying down debt. Maybe you never started investing because you were searching for a "perfect" investment.

Whatever the reason, what matters most is starting now. Stop dwelling on what you didn't do in the past and focus on what you can do today. Stop waiting for perfect.

Instead, start by saving as much as you reasonably can. Spend less than you earn, and don't lose money. You'll be better off tomorrow than you are today, and even better the day after that.

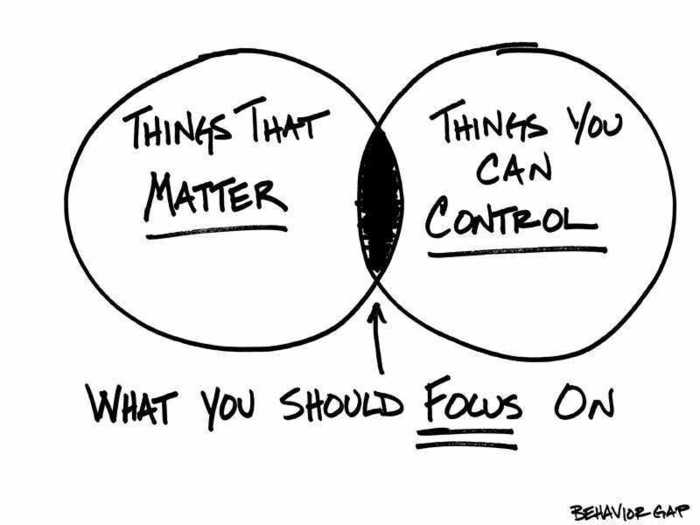

It doesn't matter what everyone else does.

People forget something incredibly important when they invest: It doesn't matter what everyone else is doing.

The only investing goal that matters is yours. But that doesn't seem to stop us from comparison shopping. When in doubt, return to your one-page plan.

Do your investments still support your "why?" If the answer is "yes," what everyone else is doing loses some of its urgency.

Even if the answer is "no" and you need to make changes, your neighbor's portfolio still doesn't matter. The best investment decisions are about your goals and not anyone else's.

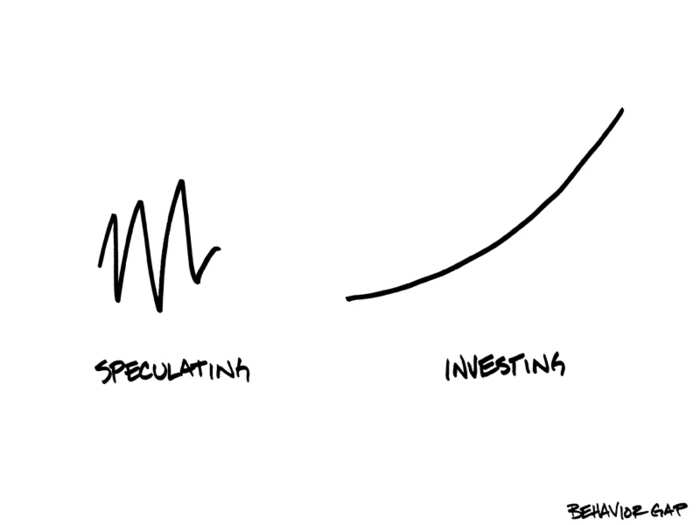

Investing is NOT the same as speculating.

When people talk about investing, they often confuse it with speculating or trading. This confusion isn't surprising.

The financial entertainment industry has convinced us that investing success depends on predicting what the markets will do next. But predicting the markets is easier said than done.

As a result, we end up frustrated, even scared, by what we "think" is investing. In reality, investing is about what we want to happen in the long term, not what happens day to day. Investors get to ignore the market's daily or even weekly performance.

Speculators, however, can't help but lay awake at night and worry what will happen tomorrow.

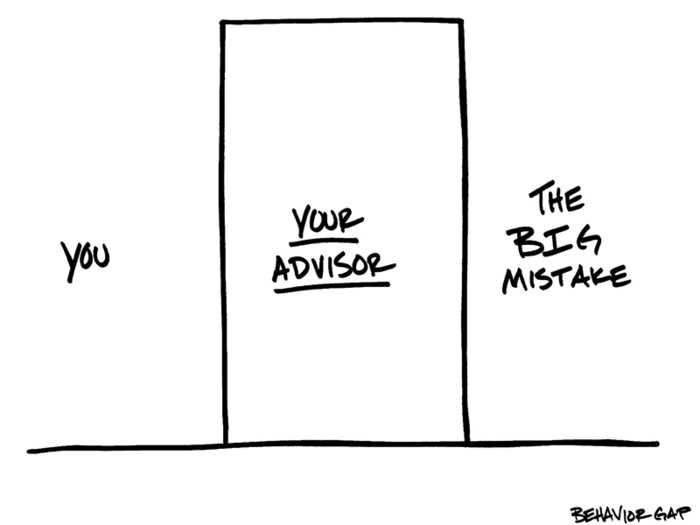

If you have a financial adviser, it's their job to stand between you and your big mistake.

At some point, investors will face what I call the "Big Mistake."

It's otherwise known as buying high and selling low. The Big Mistake isn't uncommon. When the market drops, our instinct is to sell now and stop the pain. When the market shoots up, we tell ourselves it's time to buy, buy, buy.

However, our odds of avoiding the Big Mistake go up dramatically when we have an adviser standing between us and a decision we'll regret.

Advisers get us off the emotional roller coaster and remind us of all the reasons why we shouldn't buy high and sell low.

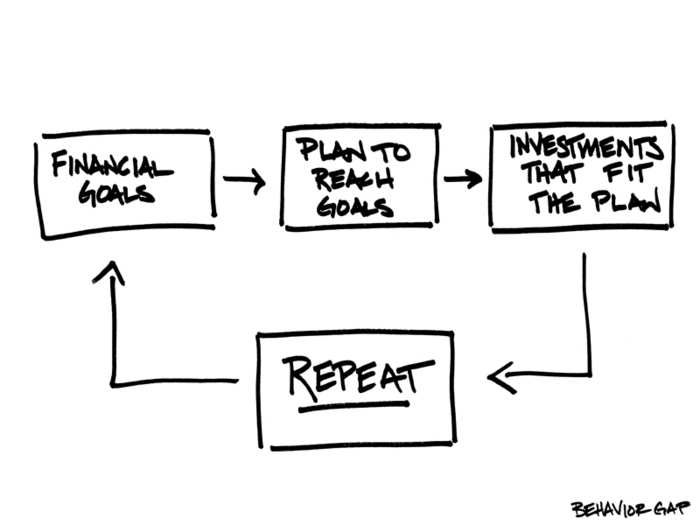

Setting up a financial plan minimizes the errors you can make.

Unless you got really lucky in the DNA lottery, the biases you're born with will inevitably threaten your ability to make good financial decisions. But that doesn't mean you're doomed.

It does mean, however, that you need a repeatable system with guardrails in place to keep on track. Start with your goals. Then, based on where you want to go, build a plan that gets you there.

Finally, pick investments that fit the plan.

Just remember: Life will happen, things will change. You'll need to repeat this process, but it will ensure that you behave better than everyone else.

Popular Right Now

Popular Keywords

Advertisement