How America's Credit Reporting System Gets Away With 40 Million Mistakes

In a controversial new '60 Minutes' segment, Steven Kroft, an award-winning investigative journalist in his own right, has tried for two years to correct an erroneous line on his credit report.

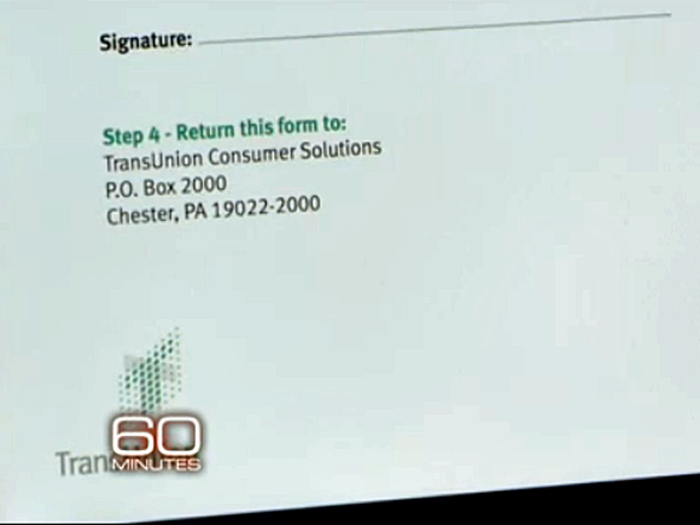

Like most consumers who call the 800 number on credit reporting agency websites, he spent 15 minutes on the phone with a representative from India and was told to fill out a dispute online.

The problem with asking consumers to file complaints electronically –– or often by snail mail –– is that they're rarely reviewed by the agencies themselves.

A Consumer Financial Protection Bureau report found that of more than 32 million disputes filed by consumers in 2011, CRAs only fielded about 15 percent in-house.

Read the full CFPB report here.

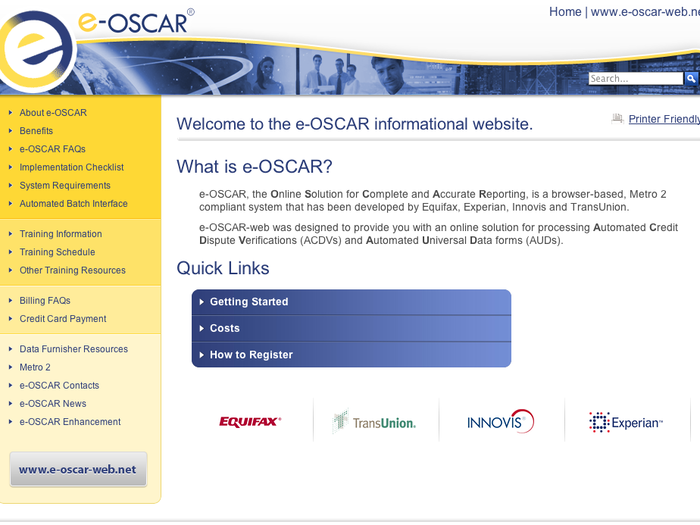

The agencies send the lion's share of disputes off to an automated system called eOSCAR, which in turn passes them off to whichever creditor is responsible for the alleged error.

eOSCAR labels disputes with one of two codes depending on their content and just 26 percent of disputes are sent to creditors with any sort of extra information.

Here's the problem with eOscar: It's not equipped to handle supplemental documentation consumers might send to back up their claim.

60 Minutes tracked down three former dispute handlers from Experian's headquarters in Santiago, Chile.

Not only did they handle 90 cases per day, but they were never allowed to call or email the consumer involved. "Mostly, we took for granted the word of the bank," said Rodolfo Carrasco. "If the bank said, 'Hey, this guy owes $100,' so it is.

But the numbers don't lie. According to the FTC, between 20 million and 40 million consumers could have errors on their credit reports that could hurt their credit score.

Read the full FTC report here.

Experian is tight-lipped usually but blasted the report Monday, saying it "does have procedures where its agents can and do question dispute responses directly with data furnishers."

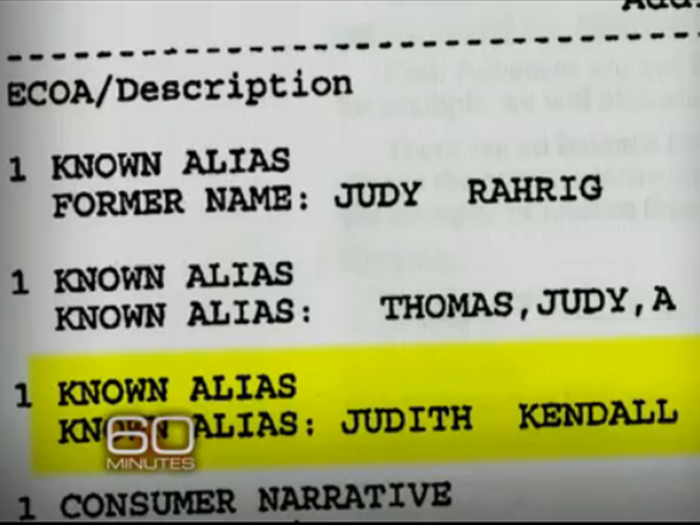

Kroft interviewed one consumer, Judy Thomas, who spent six years trying to convince credit reporting agencies that her identity had been stolen. She kept a clean paper trail and still had to take her case to court to get the issue resolved.

Like Thomas, an erroneous credit report could send consumer FICO scores –– the score most widely-used to determine credit worthiness –– spiraling. She couldn't get a car loan, co-sign her children's' student loans, or refinance her home while she disputed her claim.

Then she discovered the reason for the confusion: Her bank had received a different credit report than the one she got from CRAs. This often happens when CRAs issue reports to creditors and can be difficult for consumers to prove if banks are unwilling to reveal their report.

Turns out the bank's report showed another name for Thomas –– one she never went by. CRAs don't independently verify data supplied to them by creditors, including verifying whether their supposed customers actually do business with them.

She's not alone. Colorado grandmother Sandra Cortez made headlines in 2012 when she was detained at a car dealership after her credit report mistakenly flagged her as a suspected Colombian narcoterrorist.

Cortez's story was first reported by The Columbus Dispatch in Ohio. The state's Attorney General, Mike DeWine (right), told CBS he's opened his own investigation into credit reporting errors.

State attorneys general are one of the main lines of defense for consumers who strike out with CRAs or creditors, other than the FTC and CFPB. A pricey alternative: Hiring a private attorney to fight your battle in court.

"[These credit bureaus] would rather pay a verdict of $1 million than to actually go in and change the policies and procedures that they have," consumer protection attorney Sylvia Goldsmith told 60 Minutes. "That's much more expensive to them."

!["[These credit bureaus] would rather pay a verdict of $1 million than to actually go in and change the policies and procedures that they have," consumer protection attorney Sylvia Goldsmith told 60 Minutes. "That](https://staticbiassets.in/thumb/msid-21361454,width-700,height-525,imgsize-305400/these-credit-bureaus-would-rather-pay-a-verdict-of-1-million-than-to-actually-go-in-and-change-the-policies-and-procedures-that-they-have-consumer-protection-attorney-sylvia-goldsmith-told-60-minutes-thats-much-more-expensive-to-them-.jpg)

There are a slew of "free" credit reporting sites out there. Read the fine print. Freecreditreport.com is owned by Experian and charges $19.99 per month for a membership.

Transunion runs Truecredit.com, which asks users to sign up for a paid membership to access their 'free score.'

The site consumers really need is www.annualcreditreport.com. From there, you can check your reports from all three agencies for free once per year. You can also dispute items online as well.

No error is too small to report. "If I have a credit score of 619 and I report an error and it goes up to 620, then that one point was meaningful," says John Ulzheimer, CEO of Smartcredit.com.

Good credit is hard to come by...

Popular Right Now

Popular Keywords

Advertisement