Netflix (NFLX) has run off with the market with its revenue growth over the past couple of years. One can attribute the company's success to power plays like creating critically acclaimed proprietary television shows including House of Cards and having a heavy focus on converting existing customers onto its streaming video platform from its original DVD-rental by mail service. Analysts expect NFLX to pull off another period of growth this quarter.

While the expectations for this quarter from the Buy-Side are in-line with the Wall Street consensus, if you look 1 quarter into the future things get grim quickly. On January 7th Morgan Stanley downgraded the stock on fear of overvaluation and increased competition to its video-streaming service from the likes of Hulu Plus, Amazon(AMZN) Prime Instant Video, and HBO Go. Additionally the FCC guidelines for what we know as net neutrality have recently been struck down by the court. This opens the door for Internet Service Providers to charge variable pricing to businesses and individuals based on the quantity and type and type of data consumed online. Streaming online video is a data intensive activity and Netflix could be required to relinquish a significant part of its profit margin.

Netflix is expected to report FQ4 2013 earnings after the market closes on Wednesday, January 22nd. The information below is derived from data submitted to the Estimize platform by a set of Buy Side and Independent analyst contributors.

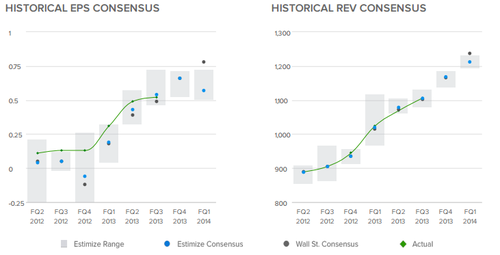

The current Wall Street consensus expectation is for NFLX to report $0.66 EPS and $1.166B revenue while the current Estimize.com consensus from 46 Buy Side and Independent contributing analysts is also expecting $0.66 EPS and $1.166B revenue.

Over the previous 6 quarters the aggregate profit consensus for Netflix from analysts on Estimize.com was more accurate than Wall Street 5 times.By tapping into a wider range of contributors including hedge-fund analysts, asset managers, independent research shops, students, and non professional investors Estimize has created a data set that is up to 69.5% more accurate than Wall Street, but more importantly it does a better job of representing the market's actual expectations. It has been confirmed by an independent academic study from Rice University that stock prices tend to react with a more strongly associated degree to the expectation benchmark from Estimize than from the Wall Street consensus.

The magnitude of the difference between the Wall Street and Estimize consensus numbers often identifies opportunities to take advantage of expectations that may not have been priced into the market. In this case, we're seeing no difference whatsoever between Wall Street and Estimize forecasts, which is unusual.

Over the past four months the Wall Street consensus trend for EPS has increased from $0.47 to $0.66 while Wall Street revenue expectations have increased from $1.102B to $1.166B. The Estimize EPS and revenue consensus have increased this quarter with EPS going from $0.51 to $0.66 and revenue increasing from $1.105B to $1.166B.

The distribution of estimates published by analysts on Estimize range from $0.52 to $0.71 EPS and $1.136B to $1.185B revenues. We're seeing a smaller distribution of estimates this quarter for NFLX than normal. The size of the distribution of estimates relative to previous quarters often signals whether or not the market is confident that it has priced in the expected earnings already. A narrower distribution signaling the potential for less volatility post earnings, a wider vice versa.

If you look out to the next quarter, FQ1 2014, the consensus forecast from Estimize is much lower than Wall Street's. This is reflective of decreasing analyst sentiment and has likely been affected by the net neutrality ruling and fears of increasing competition to Netflix's streaming video service.

The analyst with the highest estimate confidence rating this quarter is WallStreetBean who projects $0.71 EPS and $1.170B in revenue. Estimate confidence ratings are calculated through algorithms developed by our deep quantitative research which looks at correlations between analyst track records and tendencies as they relate to future accuracy. WallStreetBean, who is ranked 9th overall among over 3450 contributing analysts, is expecting Netflix to beat the Street and Estimize on both the top and bottom line.

The consensus from Estimize seems to be that Netflix will report solid quarterly earnings on Thursday, but the future may not be as bright as Wall Street analysts have projected.

The future of net neutrality and increased competition are valid and substantial concerns. Simultaneously Netflix's DVD rental by mail service is being converting to streaming video subscriptions, which puts more of Netflix's eggs in 1 basket which is going to come under enormous pressure. Investors believe that shrinking or shutting down that cog of the company's business could backfire.

On the other hand, the more optimistic are looking forward to NFLX's further expansion to overseas markets. In 2013, NFLX was available in most European countries and has only recently expanded to the Netherlands. Eyeing bigger and greener pastures, NFLX knows that expansion into international markets is crucial. However, the bigger question that looms is how well will the online streaming video service perform in the US this year?

Get access to estimates for Netflix published by your Buy Side and Independent analyst peers and follow the rest of earnings season by heading over to Estimize.com. Register for free to create your own estimates and see how you stack up to Wall Street.