Mutual fund risks: Here is how you can reduce them

May 26, 2015, 08:30 IST

Advertisement

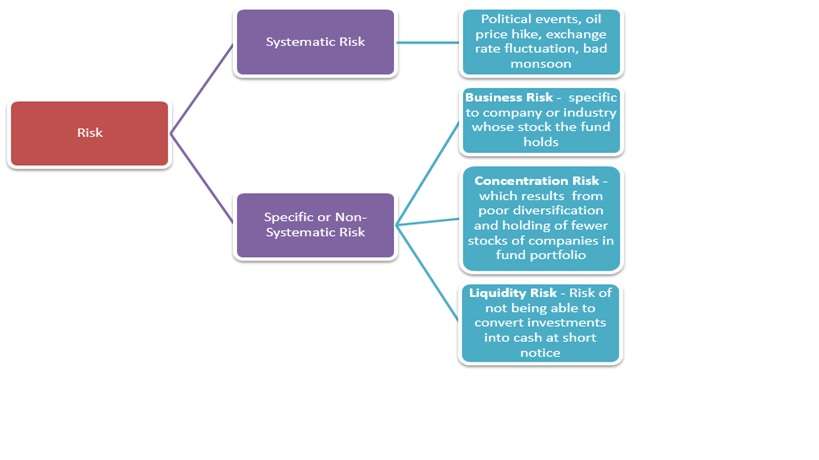

This warning that is written on all mutual fund investment documents and websites, just like they write warnings on cigarette packs, yet mutual fund investors ignore this caution primarily because people like you or me are not generally aware of the risks involved in mutual funds. This article would cover various market risks involved in mutual fund investments and also share tips on how you can reduce them.Types of risks The market risks are of two types. One type is of market risks are the ones that you, as an investor, can do nothing about. These are called systematic risks; these could be political factors, exchange rate fluctuations or even bad weather. Contrary to what you may have heard, these are difficult, if not impossible to predict or avoid. The second type is of risks are those that you can manage by diversification strategies. Generally, in a mutual fund, these risks are taken care of by your fund manager but you should be aware of them nonetheless. We can categorize them further into three broad types: business risk, concentration risk and liquidity risk.

· Business risk: A sudden strike in the auto sector is an example of business risk. Poor financial performance of a company is another example. A fund manager mitigates this by diversifying across companies and sectors.

· Concentration risk comes in when a mutual fund invests too large a proportion of its money in a single stock or sector. Sector funds, by definition, suffer from concentration risk because they invest in a single sector.

· Liquidity risk arises if a fund cannot quickly convert its investments into cash, either in response to a redemption demand by investors or as part of portfolio rebalancing. Mutual funds investing in small cap stocks face this risk.

Advertisement

What can you do about this, now that you know?

Be careful while picking mutual funds. Ensure that you invest in large well-diversified equity funds. If you invest in specific sector or small/mid cap funds, do it with full knowledge of attendant risks.

In our experience, mutual fund managers do a good job of managing risk. The biggest risk to an individual investor investing in mutual funds comes from faulty investment practices. And there is a lot you can do about it.

Reduce risk by reducing mistakes

Investing by definition involves exposing yourself to ‘risk’. The best you can do is: minimize risk. Having decided to invest via mutual funds, and not directly into stocks, is step 1 of minimizing risk. You are saying, “Let me entrust the task of investing to people more capable than me, and who do it fulltime”.

But most investors still make lots of simple errors while investing in mutual funds. Let’s look at common errors, so can you avoid them.

Advertisement

1. Investing with expectation of very high returns

In an earlier section we talked about what the long-term expected returns from various asset classes are. However, we continue to see investors choose investments with expectation of unreasonable (40-50%) returns. This is just not going to happen and in an attempt to generate that return, you are likely to be misled into investing in funds that have shown a temporary blip in performance.

Look at returns of funds over a minimum 5 year period. A 2-3% outperformance for equities and a 0.5-1% outperformance in debt funds is the best you can expect and you should be aware of that.

2. Investing without understanding of underlying investments

You already know that all mutual funds are not the same. Depending on which asset class and category of assets they invest in, you will get different returns with different behaviours. Debt funds offer lower but steadier return. Equity funds offer higher but more volatile return.

Taxes saving funds (ELSS) are essentially equity funds and have the same return and risk profile.

Advertisement

With this course, you should have enough knowledge to understand how the returns from a specific type of mutual fund will vary.3. Investing in NFOs “at par” or funds with “low” NAV

Some investors believe lower the NAV (Net Asset Value) of a fund, the better value it provides. In other words, a fund with an NAV of Rs 20 is “cheaper” than another with an NAV of Rs 30. This belief is, perhaps, a mistaken application of the value-investing principles of equity investing.

So, often such investors invest into a New Fund Offering (NFO) at par value or Rs 10, thinking they are buying value.

But as you already know, from this course, that it makes no difference whether the NAV of a fund is high or low. In fact, older funds, with a longer track record, will always have high NAV and you are better off choosing those rather than a new fund with lower NAV but no track record.

4. Investing for “dividends”

Advertisement

We often see advertisements by mutual funds declaring dividends. Some investors are misled by these and think higher dividends reflect good performance. In the case of mutual funds, dividend declaration is nothing more than a book entry. Dividends are not interest but repayment of capital. Therefore the fund’s NAV falls to the extent the dividends are paid out to its unit holders. In fact, a growth option where you withdraw the money when YOU need it is better for you from a tax perspective.Conclusion

Understanding market risk is important, but if you have chosen the asset class that best meets your objectives, you can trust the fund manager to manage the market risk for you.

As an investor, you should focus on things you can control which are: Choosing the right mutual funds; following the correct process for investing; and reviewing your investments every year.

(About the author: This article has been contributed by Sanjiv Singhal, CEO, scripbox.com.)

(Image credits: www.economictimes.com)