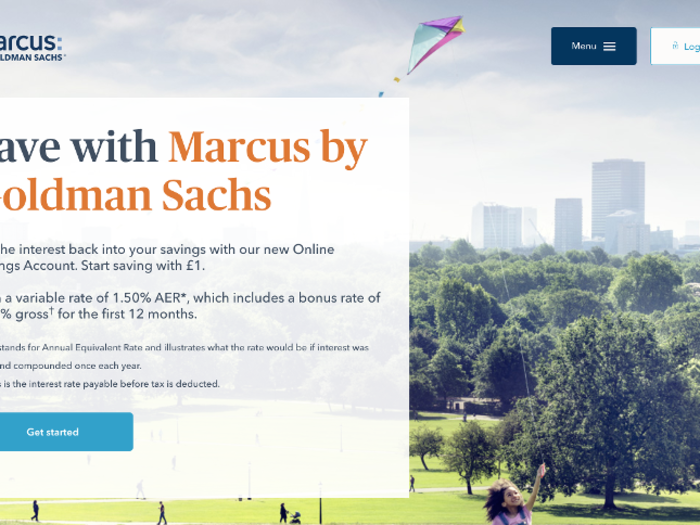

We tried Marcus, the new service that lets Brits bank with Goldman Sachs for as little as £1 - here's what we thought

Besides the backing of one of the financial world's most recognisable names, what stands out most about Marcus' savings account is its interest rate — 1.5%!

Signing up for Marcus is a pretty straightforward process.

Marcus has no physical presence, so sign up must be done online. Given that the accounts are targeted at millennials, that's probably not going to be much of an issue for prospective customers.

I set my account up on Marcus' launch morning in the UK, and the whole process took less than 15 minutes. I had some of my savings in the account in less than 30 minutes.

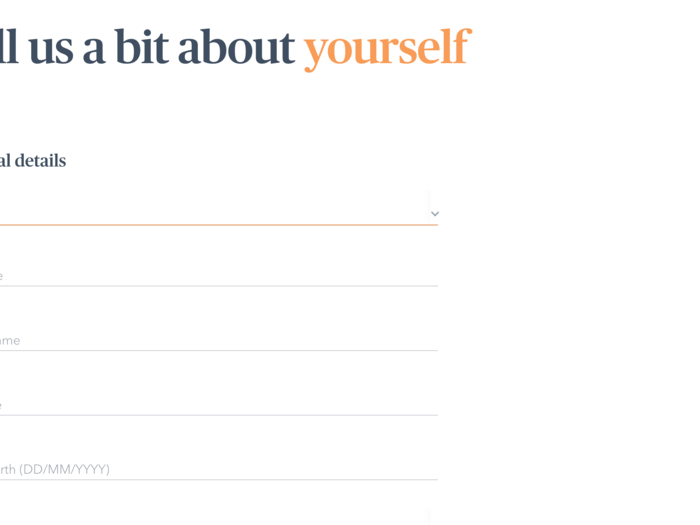

First up, you'll have to give Goldman Sachs a bit of information about yourself. Name, date of birth etc, but also some more unusual details including your job and salary bracket.

Salary info isn't generally required to set up a non-credit based banking product, but there's no indication that Marcus has excluded anyone from opening an account based on their salary. Goldman Sachs told This Is Money that the info gathered is "part of our anti-money laundering controls."

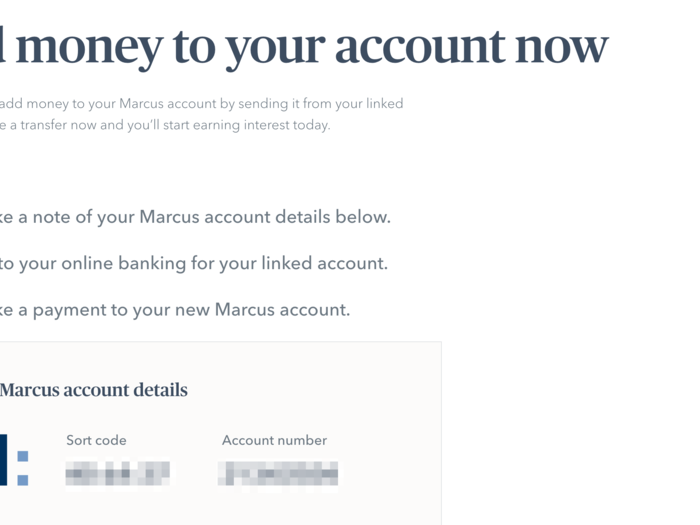

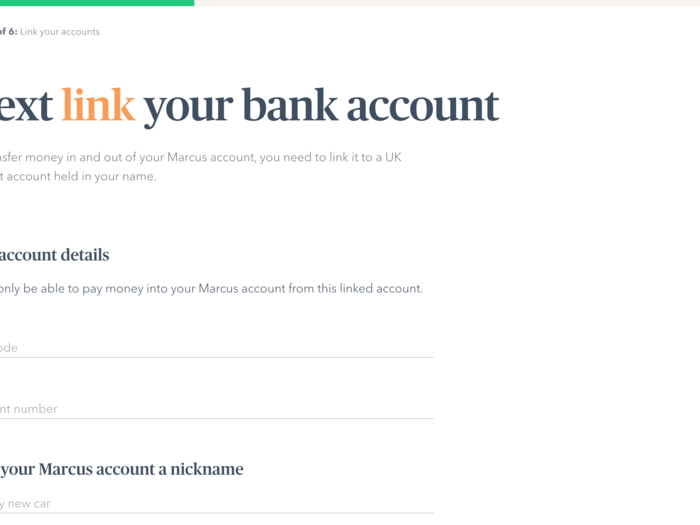

Once you've entered your details you'll need to link Marcus to another bank account.

The account you link to Marcus is the only one into which you'll be able to withdraw money. This feature is a pretty simple but it's a clever way of preventing theft, as there is literally no other means of withdrawing money other than putting it into the linked bank account, which you own.

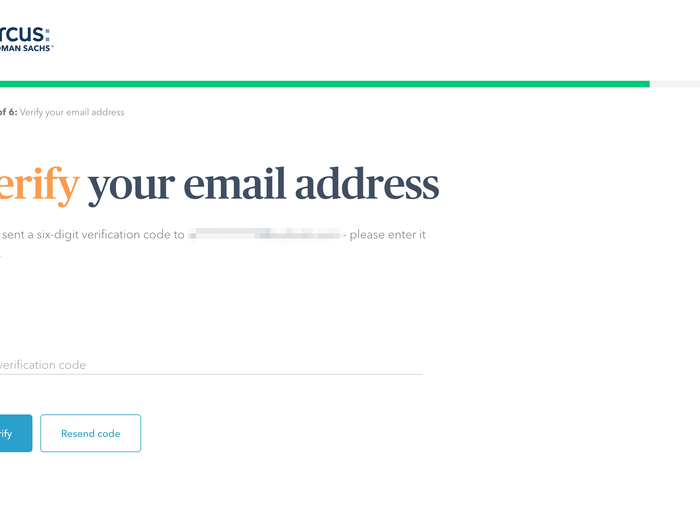

After you've linked an account, you need to set a password and PIN to protect the account, as well as verify the email address you've linked to your Marcus account. Once again, it was all very straight forward.

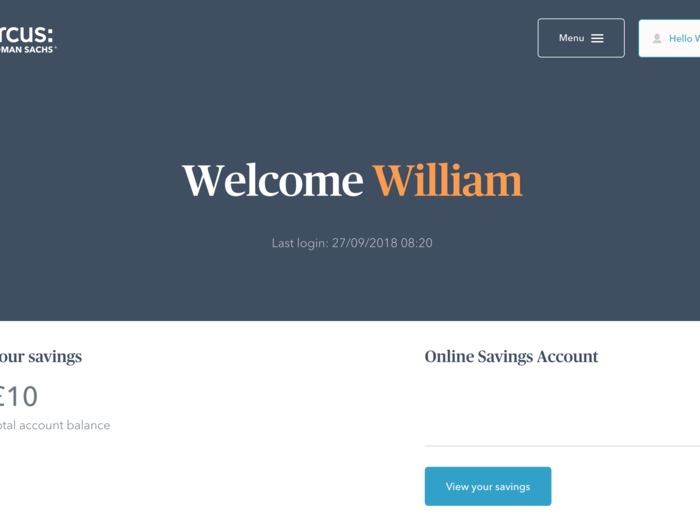

And with that, you're a Goldman Sachs customer!

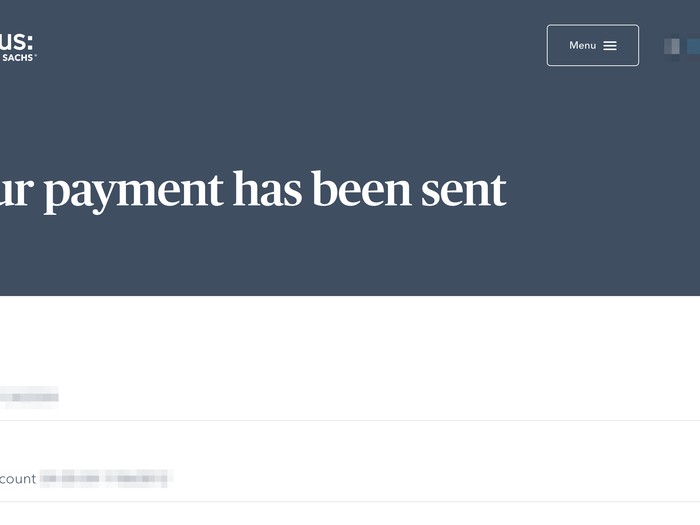

Transferring money to and from the account is a very simple process, and admirably quick.

Over the first few days of using my Marcus account, I made several transfers and most were cleared within 10-15 minutes. Transfers out were particularly speedy, ending up in my current account in seconds.

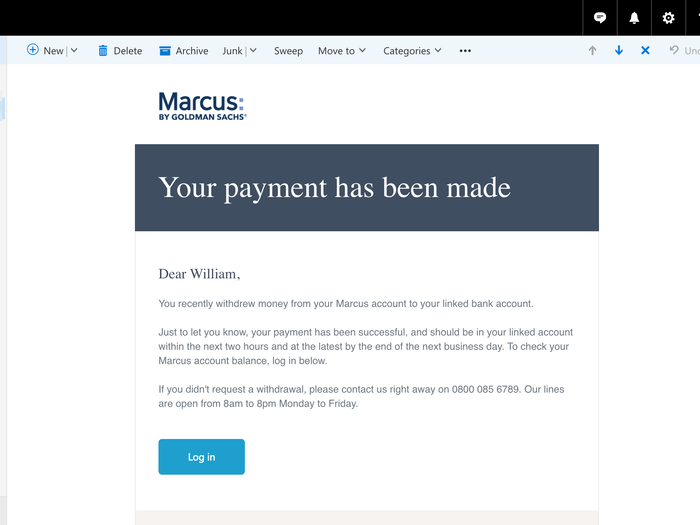

A nice feature of Marcus is that you receive an email every time you make an outbound transfer, adding another layer of security to your account.

One potential downside is that despite being entirely online, it does not yet have an app of any sort.

Users wanting to check their balance or make a transfer on their phone or tablet need to use a browser-based web page to do so. This is potentially frustrating for some users, but I used the mobile interface numerous times and it was a perfectly smooth, if basic, experience.

Simplicity is one of the defining features of Marcus. It lacks any bells and whistles. The only features available when logged in are as follows: viewing, printing or downloading your transactions, withdrawing money, viewing your profile, and a guide to moving money using the account. It's all you need, but users looking for a savings account with lots of features might be left disappointed.

CONCLUSION

As a savings account, you're not going to be using Marcus on a day-to-day basis, but it's good to know when you do, the account is well laid out, and easy to use.

If you want a savings account with lots of features, and a physical branch to visit, Marcus isn't going to be for you. But if you just want a functional account with a very good interest rate, its a solid choice, and a decent addition to the UK retail banking landscape.

Popular Right Now

Popular Keywords

Advertisement