These 7 charts show the effect of Trump's trade war on the US economy - and why a big slowdown is looming

GDP growth is slowing, but it doesn't look like recession is likely.

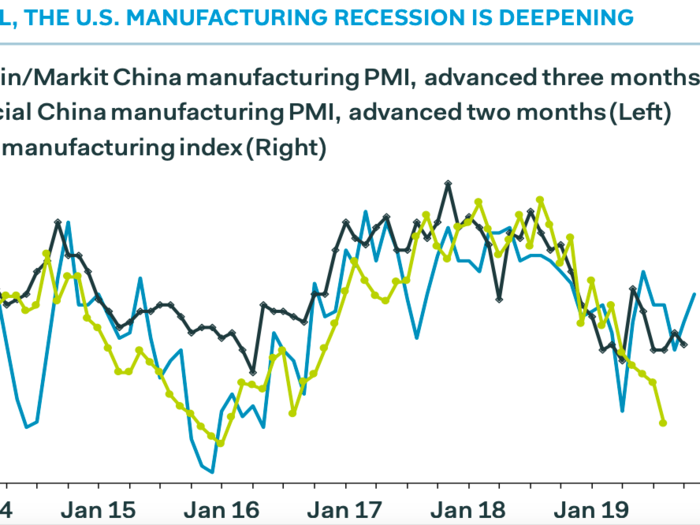

Manufacturing is struggling.

At the start of this month, data showed that factory activity dropped unexpectedly. ISM data showed that the purchasing managers index in August fell to 49.1. The contraction came as a result of the drop in demand due to the trade war, but it was still a shock that ISM data showed that manufacturing activity dropped to below 50 as it's a signal of a slowdown.

Smaller businesses aren't investing in the future because of uncertainty.

To add to this data from smaller businesses showed that Main Street is investing less in the future, with data from the National Federation of Independent Business showing that business optimism among smaller businesses fell to 103.1 — a 1.6 point fall. With more uncertainty about the future, America's smaller businesses are feeling the heat of Trump's battle with China.

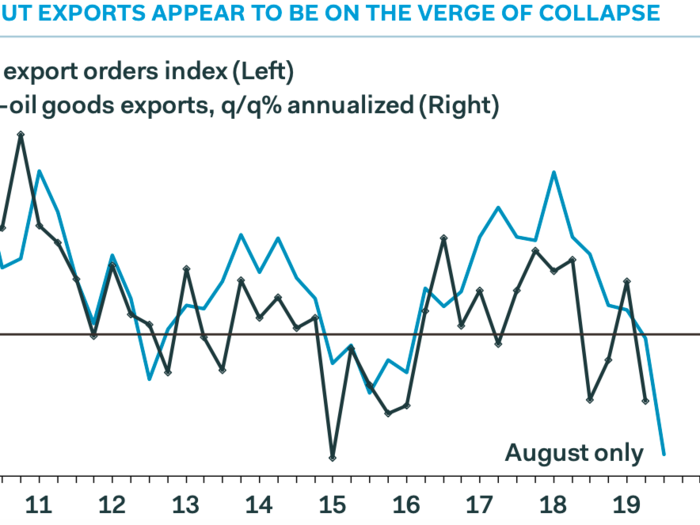

Exports are falling rapidly.

China is one of the major trading partners of the US — meaning that exports have suffered massively because of the trade war. As a result, smaller businesses and industrial production have both suffered a knock-on effect.

Pantheon said: "The intensification of the trade war is now hammering both exports and business confidence." And: "Exports appear set to plunge."

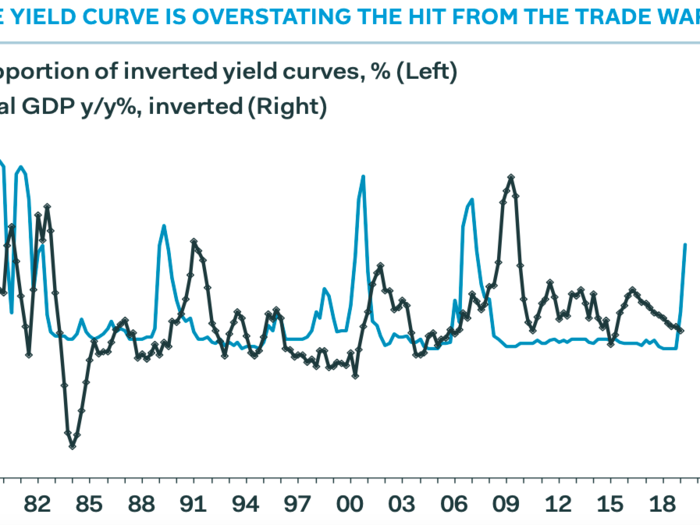

The yield curve is inverted.

Possibly the most talked-about indicator of recession in recent months, the yield curve, inverted in July — signalling that we could have a recession within the next year. But with GDP trending upwards, Pantheon says it doesn't look ominous just yet.

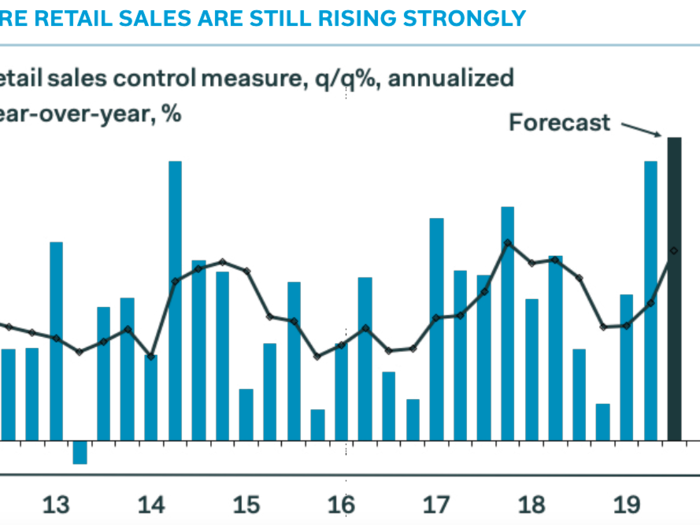

Retail is bucking the trend.

Despite pressure, retail sales have remained strong and forecasts show this is set to continue. However, through other indicators, Pantheon says this might not last.

"Consumption will slow as the tariffs depress real income growth," said the research firm, adding wage growth remains subdued.

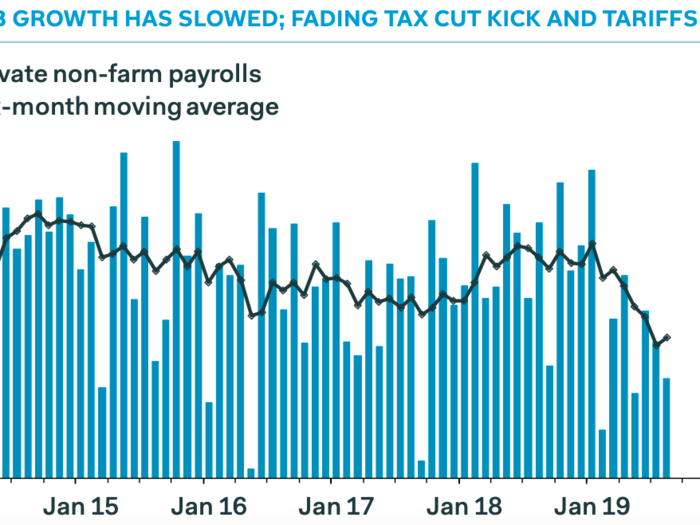

Jobs are taking a hit.

Nonfarm payrolls came in way below expectations this month, as 130,000 jobs were added to the US economy in August, compared to the 160,00 expected. Pantheon at the time warned that this is just the start and that by late fall growth could slump.

"Employer surveys and other data suggest that job growth is on course to slow to just 50,000 or so by late fall," said Pantheon Macroeconomics. "This implies that unemployment is likely to start creeping higher, and we expect layoffs to start creeping up too."

Popular Right Now

Popular Keywords

Advertisement