It's starting to look like Tesla has turned a corner on its latest crisis

The Model 3 is on the road.

Tesla can start to hype Model 3 variants — and talk more about forthcoming vehicles.

We've been hearing about the Model 3 for years, but now the car has arrived and, over time, it should settle into Tesla's version of predictability, which is to say nothing that resembles the predictability of the rest of the industry.

We've already witnessed the announcement of the high-performance, all-wheel-drive version of the car, stickering at almost $80,000. Look forward to new styles and different flavors, as well as assorted subplots about software updates. This is how Tesla drives its story forward: lots and lots of newsbytes.

On the horizon, Tesla has four new projects to captivate the masses and the markets: the new Roadster, with its Formula-One-car level acceleration; the Tesla Semi; a possible pickup truck; and the Model Y compact crossover.

The Model 3 and its ongoing struggle will soon become water under the bridge. Such was the case with the Model X, a much-scrutinized and debated vehicle that launched in 2015 and has now been chugging long for a few years, bringing in massive amount of revenue for Tesla (well-equipped Model X's can top $150,000).

The Model X is now integrated with a production system at Tesla's Fremont factory that can reliably build about 25,000 of both vehicles combined every quarter. It's gone from high-drama, crisis-state production hell to something nobody ever talks about anymore, its relative success drowned out by Model 3.

Model 3 could continue to throw up problems, but the Tesla story will shift to new stories in late 2018 and early 2019.

Capital raises and debt funding.

Musk has declared that Tesla won't need to raise money in 2018 and will be profitable in the second half of the year.

Even if we take him at his word and Tesla can somehow avoid spending the roughly $3 billion it has in cash on hand and doesn't tap out its lines of credit or have to borrow from SpaceX, that doesn't mean Tesla won't raise money in the future or post money-losing quarters.

With Tesla's stock price at historically quite high levels, it makes the most sense to raise money by selling new shares. I don't know why they haven't done it already. But that's Tesla's business.

The company has a lot of spending ahead of it. It's Fremont, CA factory is maxed out on capacity, the Roadster and Semi have to be developed and built, and a new plant in Shanghai, China needs to be funded.

Automakers typically bankroll this long-term stuff with debt. A new factory, for example — and Tesla's China plant should be wholly owned by the carmaker, as China has adjusted its joint-venture rules — will be around for decades, so using debt to find the investment allows companies to use the magic of inflation to reduce that financial burden over 20 or 30 years.

Tesla isn't in a great position to sell bonds at the moment: a 2017 offering was successful, but Tesla's debt is junk-rated, not investment-grade. Its equity is the opposite, but the company doesn't want to sell $1 billion- $2 billion at a clip and continually dilute existing shareholders. Obviously, if shares surge past $400 at some juncture, selling equity will become more tempting.

Musk might also sell a big chunk of Tesla to a major outside investor, somebody like China's Tecent, which took a 5% stake in 2017.

Regardless, Tesla's current austerity program isn't likely to last.

Bears are running out of arguments.

The bull case for Tesla is simple: the company doesn't die, gets bigger, makes more money, and maybe someday starts generating consistent profits, vindicating the over-$50-billion market cap.

The bear case is trickier and requires a constant influx of new reasoning. The big money — Musk owns 20% and institutional investors such as Fidelity make up the other major shareholders — is staying put. If there were a justification for a massive sell-off, the Model 3 debacle would have presented it, but the stock hasn't tanked.

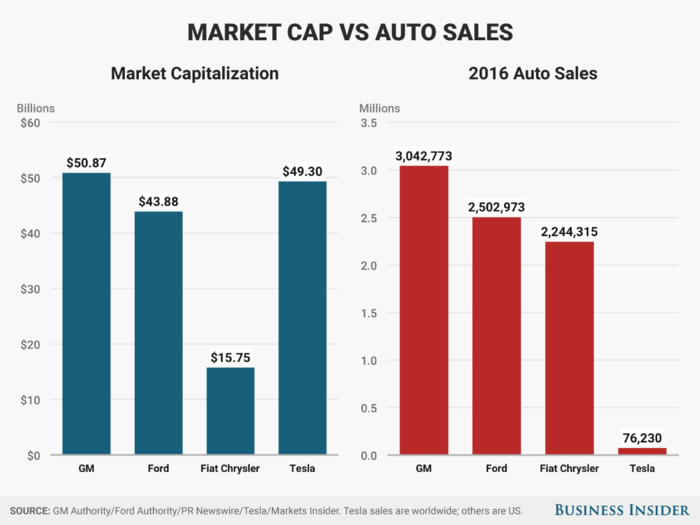

Clearly, Tesla doesn't sell enough cars to make it worth more than Ford, Fiat Chrysler Automobiles, and General Motors. But the stock itself has returned so much — around 1,000% since the 2010 IPO — that it's impossible to argue that Tesla has been a stupid bet. In a low-yield, conservative-investment world since the financial crisis, Tesla has been an excellent place to park cash.

I study the bear analysis all the time and have also considered Tesla in light of its refusal to make money and its appetite for larding up its balance sheet with debt — the classic formula for a carmaker going bust.

Bearishness has moved through phases. When the straightforward analysis of Tesla's business didn't undermine the stock price, an obsession with production emerged. This became especially heated around Model 3, with good reason, but it overlooked the sustainable execution on Model S and Model X.

Now that Model 3 production is starting to appeal more functional (if offbeat by industry standards), management has come under fire. The company is synonymous with Musk, so his every move and utterance has been parsed. Executive departures have been pointed to as signs that the roof is falling in.

There could be something to all this, but again, major investors have affirmed Musk's leadership and minted a massive new pay package for him, predicting a $650-billion market cap. The board survived a proxy contest earlier this year. Investigations by the SEC and the NTSB, the latter related to several Autopilot accidents, haven't crushed shares.

Personally, I think Tesla's valuation will over time revert to a less vertiginous level, but that will be due to the natural course of business and an impending sales downturn that will affect the entire industry. The bears won't be able to hasten this process.

Almost everybody likes the cars.

Sure, there have been some stories about Tesla vehicles having problems that take a long time to fix, and plenty of Model 3 reservation holders are having their patience tested by the extended wait for their cars to get built. There's a valid theory that Tesla might never be able to affordably construct the promised $35,000 base Model 3.

But for the most part, Tesla owners love their cars and have loved them, in some cases, since the days when the only Tesla for sale was the original Roadster.

I drive all kinds of different cars all the time, and I've driven everything Tesla has ever made. The Roadster, Model S, Model X, and Model 3 have all been quite impressive. Not as warp-your-mind stunning as Musk and others would have you believe. But very nice cars.

Producing a beloved product is no guarantee of success — just ask anybody who bought a Saturn in the 1990s. But it goes a long way toward amassing brand equity, which is deceptively valuable. It doesn't even have to be as irrational as with Tesla.

Take the BMW 3-Series. An excellent car. Some people have bought or leased dozens. Is the car free of problems? Of course not. Are there competitive alternatives? To be sure. Has this hurt the vehicle? Well, sales have declined as SUVs have become more popular, but the 3-Series has been largely bulletproof. It has routinely delighted customers, and they've consistently returned for more.

In the end, Tesla skepticism will persist. And rest assured, there will be another crisis. And another and another and another. But that's how it's always been. Yes, Tesla could still go bust. But anybody who knows anything about the company realizes now that the familiar pattern of crisis and recovery is currently underway, and at this point it seems that the worst is over.

Popular Right Now

Popular Keywords

Advertisement