Elon Musk's plans for Tesla keep getting weirder and it could put the company's future at risk

Tesla is supposed to be a growth company, but it just laid off 9% of its workforce.

We are getting daily, speculative updates on a 15-year-old carmaker's ability to make cars.

Let's be clear: in over a decade over covering the auto industry, I've never seen anything like the level of fixation on the production ramp of the Tesla Model 3. Usually, a car company announces that it will launch a new vehicle — and when the launch date arrives, the vehicles start rolling off the assembly lines in reliably projected quantities and buyers can find them on dealers' lots.

You don't even have to think about it — that's how good the world's global automakers have gotten at production management. Manufacturing is simply assumed.

But with the Model 3, nothing is assumed. We've fallen into an epic, daily saga over how many cars Tesla is making. Will it be 5,000 a week by the end of June — or merely 4,000? Less than that? A surge to 6,000? Will the assembly lines be shut down again? Will the new robots work?

This is bonkers stuff. If Toyota thinks it will sell over 300,000 Corolla sedans in the US in 2018, as it did in 2017, it will crank out 25,000 per month as it is currently doing and — Presto! Goal achieved. Zero drama! And that's just one vehicle, in a portfolio of dozens.

The Model 3's much-heralded arrival has been accompanied by an astonishing amount of futuristic and bizarre dialog, as well. We've been lectured on S-curves and step-functions, first principles, and drowned in distracting rhetoric about a system that, while far from easy, isn't exactly poorly understood or still being worked out in practice: almost 80 million automobiles were constructed and sold in 2017.

Tesla is getting a massive pass on this because the tech media are clueless about auto manufacturing — understandable as they've never covered it before — and the well-informed car-business press considers Tesla to be a gigantic exception to the rules.

Elon Musk keeps spending money borrowed against Tesla shares to ... buy more Tesla shares.

Musk has bought about $35 million worth of Tesla stock in the past two months. In May, shares were sliding when he bought. Last week, when he laid of $25 million to purchase 72,000 shares, they had been rallying.

Musk isn't really getting paid by any of his companies (Tesla and SpaceX), so he funds his life by borrowing against his Tesla stake. He holds about 20% of the company and is its largest shareholder.

Last year, Tesla disclosed that Musk has loans with Morgan Stanley to the tune of about $624 million, pledged to Tesla stock as collateral. Presumably, this is the funding channel he's using to buy more stock.

I've never been comfortable with this arrangement. Musk has an incentive to move the stock price higher, although he has at times talked it down. With cash borrowed against Tesla's valuable shares, he buys more shares and ... the shares become more valuable! In a sense, this is pretend money creating speculative value.

Bulls see it as a positive because the CEO is putting his money where his mouth is. But it leaves Musk vulnerably to a stock decline that would undermine the value of his collateral, and it saves him from having to sell any stock to support his lifestyle.

It's difficult to be moralistic about this kind of stuff: Musk can spend his millions as he sees fit, and as far as I know, he isn't buying private islands. One could argue that he's all-in with Tesla. But one reason he is able to borrow so heavily is that Tesla is worth $50 billion — and yet in the year since the Model 3 launched, with 400,000 in pre-orders at $1,000 a pop, the company has barely made a dent in the order book.

Tesla doesn't need a higher stock price, and Musk himself doesn't need more shares, to rectify this problem. The company simply needs to jettison some of its more grandiose concepts about reinventing carmaking and just — make some cars! Musk might be in personal production hell, as he likes to call it, but the ability to lay your hands on $25 million whenever you need to should take the edge off.

The question is whether dropping that kind of coin right after you've handed out 3,000 pink sips sends the right message.

Tesla is practicing austerity while the rest of the business is actively investing.

The numbers don't lie. Tesla is cost-cutting at a time when big automakers, rolling in cash after three years of record US sales, and spending. GM and SoftBank together are investing $3.35 billion in GM's Cruise division, giving it an $11.5-billion valuation inside a company that's already worth over $50 billion.

Alphabet's Waymo, formerly the Google Car project, is acquiring 62,000 Chrysler minivans to use for a fully autonomous ride-hailing service rolling out in 2018. The company could be worth $50 billion-$70 billion.

Tesla, meanwhile, is nickel-and-diming, scraping off what Musk calls "barnacles" and subjecting every $1-million allocation for the CEO's approval.

Tesla has undertaken some acquisitions, notably Grohmann Engineering, a German automated-manufacturing firm. However, that's been a mixed bag as the company's founder was ousted last year after reportedly disagreeing with Musk. Grohmann's technology also hasn't yet been a boon to Tesla, as the carmaker has backed off its plans to aggressively automate its assembly lines for vehicles and batteries.

Big car companies know that now is the time to invest and take risks. The booming US sales cycle has lasted longer than expected, but it can't last. Eventually, the market will turn and everybody, including Tesla, will have to play defense.

But major automaker won't completely stop playing offense. Tesla could be facing a different story: nothing but defense as it faces it first downturn as a mature carmaker.

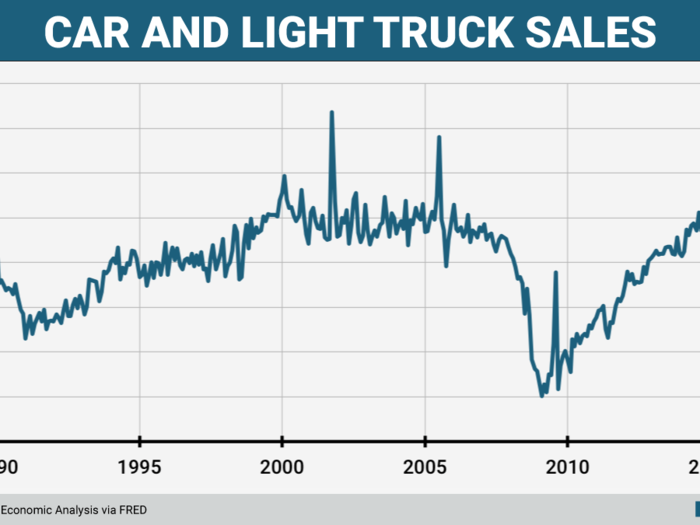

Tesla is playing chicken with an overextended auto-sales boom in the US just as interest rates and gas prices are starting to creep up.

Tesla has dodged bankruptcy before — in 2008 — but its recovery and rise have coincided with a massive upturn in new-car sales since 2010, driven by low-interest rates and, more recently, by historically cheap gas.

That dynamic has led to 17-million-vehicle sales years in the US since 2015.

Now the pace is weakening. We'll be lucky to make 17 million again in 2018. Something north of 16.5 million is more likely. Interest rates are ticking up, affecting car loans and leasing, and gas prices are rising. These are probably the early days of a sales slide that could be more substantial than anything we've seen since the end of the financial crisis.

I think the sales constriction will reduce demand for both gas-powered and electric vehicles, as the entire US market contracts. This doesn't mean that Tesla won't sell more cars than it did in 2017, or more in 2019 than it expects to sell in 2018. But the expansion of Tesla sales could slow, and that will impact the company's business.

In particular, it could leave Tesla with inventory issues, especially with used vehicles. Tesla should have a significant number of cars coming off lease in the next few years, as well as trade-ins showing up. The market for used electric cars is flatly awful, and in any case, Tesla needs to sustain new car sales at profitable levels before it even thinks about the costs and benefits of selling used cars.

Interestingly, this is a case of Tesla's Bizarro World intersecting with the Bizarro World of the traditional auto industry. The outcome could be double Bizarro. The worst-case scenario is that the entire electric-vehicle market collapses, as it did during the financial crisis. The best-case, for Tesla, is that a downturn imposes some discipline and compels the company to simplify its future production systems.

Popular Right Now

Popular Keywords

Advertisement