CREDIT SUISSE: Here's the best stock to buy in every sector

FMC

US Steel

Ticker: X

Sector: Metals & Mining

Year-to-date performance: -1.86%

Credit Suisse’s take: "The US flat rolled market is firing on all cylinders, as (a) seasonally demand is accelerating and peaks in 2Q, (b) scrap prices recover from historically low levels at the start of winter, and b) S/D fundamentals benefit from limited imports and a strong US/global economy. We like X for its strong leverage to the cycle, accretion from its Granite City BF restart, and likely asset sales as the company refocuses on its core steelmaking operations."

Source: Credit Suisse

Sealed Air Corp.

Ticker: SEE

Sector: Paper & Packaging

Year-to-date performance: -12.2%

Credit Suisse’s take: "We believe recent share price weakness offers an attractive entry point. In part, we believe weakness has been driven by near-term resin cost headwinds that we view as passing. We believe SEE has entered a period of strong EPS growth."

Source: Credit Suisse

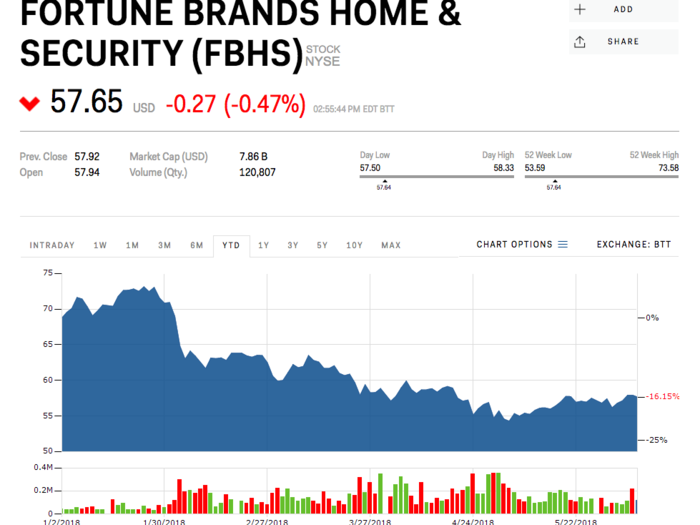

Fortune Brands Home & Security

Ticker: FBHS

Sector: Homebuilding & Building Products

Year-to-date performance: -16.15%

Credit Suisse’s take: "Fortune Brands is among the best-positioned names within our coverage as: (1) it leverages its base of established brands, especially in plumbing, to gain share, (2) seeks expansion in attractive, higher margin categories through acquisitions, and (3) maintains a balanced capital structure, including returning cash to shareholders. As such, the company has delivered industry-leading margins, which we expect to hold as we enter the middle to latter parts of the housing cycle.

Source: Credit Suisse

Marriott Vacation Worldwide

Ticker: VAC

Sector: Leisure

Year-to-date performance: -9.57%

Credit Suisse’s take: "Marriott Vacations (VAC) is a top tier timeshare company―an industry we like given strong forward macro indicators, consolidation and the shift of consumer spending to travel and leisure. VAC is acquiring a close competitor, ILG, in a transaction we think is highly accretive – with minimal synergies reflected in the stock.

Source: Credit Suisse

McCormick & Company

Ticker: MKC

Sector: Packaged Food

Year-to-date performance: -0.43%

Credit Suisse’s take: "McCormick will continue to drive robust 3-4% organic growth and gross margin expansion through unparalleled pricing power at retail, RB Foods’ accretion and strong momentum in its Flavor Solutions segment."

Source: Credit Suisse

Home Depot

Ticker: HD

Sector: Retail: Hardlines

Year-to-date performance: +3.99%

Credit Suisse’s take: "We view HD as a best-in-class retailer with a strong management team that participates in one of the strongest segments of retail, marked by oligopoly pricing, reduced supply, and relative insulation from e-commerce. At a time when most retailers are on defense, HD has a unique ability to reinvest its margins, leveraging its lead in the category and the strength of the cycle. That has served HD well in recent years, with early investments online, in distribution and on the Pro side of the business, supporting significant outperformance."

Source: Credit Suisse

PVH

Ticker: PVH

Sector: Softlines Retail & Global Brands

Year-to-date performance: +18.9%

Credit Suisse’s take: "We think PVH’s +13-15% long-term EPS algorithm is becoming easier to achieve and Consensus underappreciates the upward P&L pressure from PVH’s increasing mix towards its higher-margin and faster-growing international business (~50% of revenues)."

Source: Credit Suisse

Five Below

Ticker: FIVE

Sector: Staples Retail & Distribution

Year-to-date performance: +43.15%

Credit Suisse’s take: "(1) Insulation from online competition and a white space opportunity that could be larger than management predicts wrapped in the quickest new store return model we’ve seen. (2) Solid visibility for 20% top- and bottom-line growth through 2020 and 20% EPS growth beyond as share repo begins."

Source: Credit Suisse

Sunrun

Ticker: RUN

Sector: Alternative Energy

Year-to-date performance: +108.26%

Credit Suisse’s take: "Non-regulated residential rooftop solar financing and installation market leader. With a market price that reflects current contract with limited credit for growth."

Source: Credit Suisse

Marathon Oil

Ticker: MRO

Sector: Exploration & Production - Large Cap

Year-to-date performance: +21.58%

Credit Suisse’s take: "MRO’s divestiture of its Canadian oil sands mining business coupled with two Permian acquisitions last year sharply improved the company’s portfolio, a dynamic we believe is still underappreciated by investors. Meanwhile, MRO offers one of the most attractive oil and cash flow per debt-adjusted share growth profiles among the global E&Ps."

Source: Credit Suisse

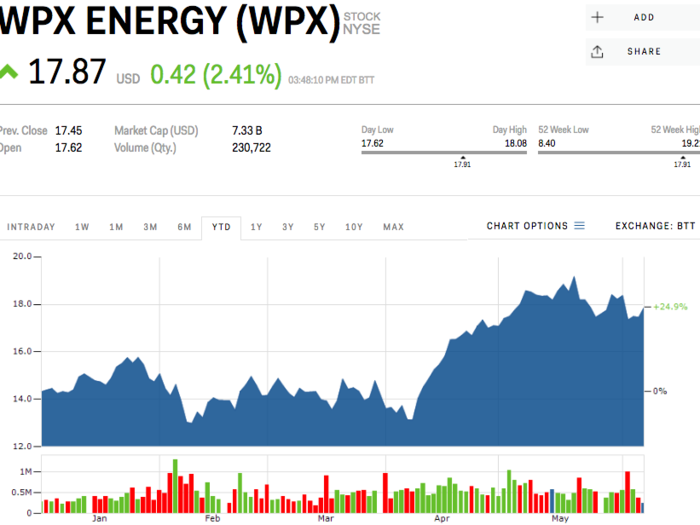

WPX Energy

Ticker: WPX

Sector: Exploration & Production - Small to Mid Cap

Year-to-date performance:n +24.9%

Credit Suisse’s take: "WPX stands out as having the most differentiated Permian takeaway portfolio in the SMID E&P space, which provides protection from widening Mid-Cush basis―a key investor concern. Moreover, shares have historically traded at a discount in-part due to an elevated leverage profile vs peers."

Source: Credit Suisse

Halliburton

Ticker: HAL

Sector: Oil Services & Equipment

Year-to-date performance: -1.41%

Credit Suisse’s take: "North America has come back first and fastest; considering HAL is the biggest player in the NAM onshore market, this is a major positive. In many ways HAL has been cursed by the step change in NAM activity. Rather than a 20% CAGR for five or six quarters, the rig count doubled in a few months. We do not view this as a negative, as activity will now move forward from a higher level than expected. HAL has the most exposure to the fastest-growing segment of the NAM market (completions) than any other large company we cover."

Source: Credit Suisse

Marathon Petroleum Corporation

Ticker: MPC

Sector: Refining & Marketing

Year-to-date performance: +17.24%

Credit Suisse’s take: "CEO Gary Heminger has been focused on the right steps to add value at MPC. We liked the acquisition of Galveston Bay, as it is a high-quality refinery in a good location with helpful access to export markets, bought on a low multiple. We thought the acquisition of the Hess Retail store footprint was similarly strong, with management able to beat seemingly lofty synergy targets."

Source: Credit Suisse

Exelon Corporation

Ticker: EXC

Sector: Utilities

Year-to-date performance: +1.85%

Credit Suisse’s take: "Strong non-regulated nuclear cash flows are set to in crease 2H18 and beyond with electric market reforms support above-average utility growth, dividend and de-levering. The stock remains inexpensive on our sum of the parts target price, with >12% total return expected. EXC also has a series of positive catalysts coming up: the NJ zero emission credit subsidy program (signed into law on May 23), the Fast Start energy market reform approval at FERC (Sept/Oct), and baseload energy market reform approvals (mid-2019). "

Source: Credit Suisse

Blackstone Group

Ticker: BX

Sector: Asset Managers / Retail Brokers

Year-to-date performance: +0.37%

Credit Suisse’s take: "Markets are missing the improvement in underlying earnings power: Given the rapid growth in BX’s core/underlying earnings power (carry generating AuM, carry eligible AuM, fee-earning AuM), we think BX could roughly double its 2015 (last cycle peak) Distributable Earnings (DE) generation in three to five years."

Source: Credit Suisse

JPMorgan Chase

Ticker: JPM

Sector: Banks

Year-to-date performance: +2.56%

Credit Suisse’s take: "JPMorgan represents the value inherent in the universal banking model--best-in-class execution—leveraging its complete, scaled and well-integrated product set to drive profitable and sustainable revenue growth. Add to that a willingness to drive down unit operating costs (capacity for investment to drive incremental growth; a virtuous circle) and an ability to optimize capital; this sustains better-than-average earnings growth and ROEs."

Source: Credit Suisse

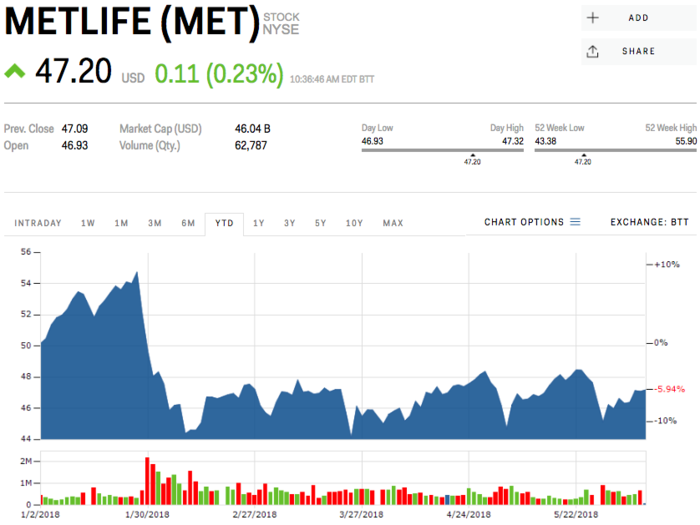

Metlife

Ticker: MET

Sector: Insurance - Life

Year-to-date performance: -5.94%

Credit Suisse’s take: "MET has a relatively high degree of control over its future success, driven by strong retirement, group benefits, and international businesses, which have low sensitivity to equity market fluctuations. Further, with the majority of its variable annuities (VA) business divested via the BHF spinoff, we expect the large one-time charges experienced over the last several years to subside, as the VA business was the source of most of the charges."

Source: Credit Suisse

Nationstar Mortgage Holdings

Ticker: NSM

Sector: Mortgage Finance

Year-to-date performance: -4.51%

Credit Suisse’s take: "NSM agreed to be acquired by WMIH for a combination of cash and stock; the deal should not affect the operations of the company. Servicing profitability (pretax) has been improving while the company has been growing its subservicing mix – this shift toward a less capital intensive business model should allow for better returns on capital and better free cash flow generation."

Source: Credit Suisse

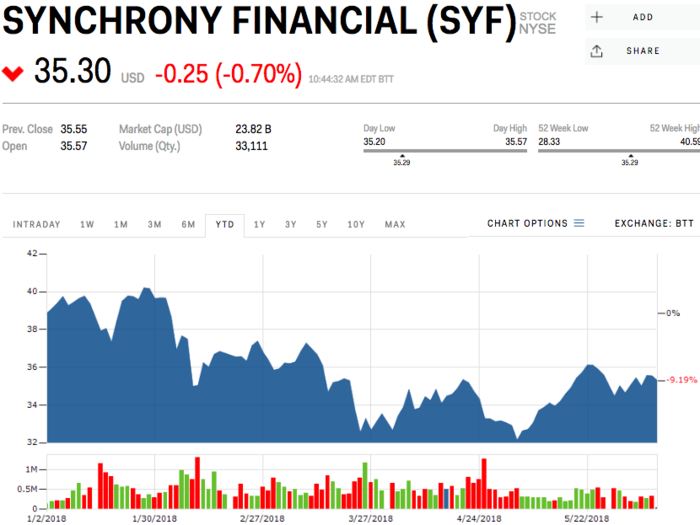

Synchrony Financial

Ticker: SYF

Sector: Specialty Finance

Year-to-date performance: -9.19%

Credit Suisse’s take: "Synchrony, a leader in retail cards and financing of large ticket purchases and healthcare is well positioned for continued strong growth, and is protected from rising credit losses (relative to peers). Long-term lockup for the bulk of its large contracts insulates SYF from the current competitive environment."

Source: Credit Suisse

Biomarin Pharmaceuticals

Ticker: BMRN

Sector: Biotechnology — Small to Mid Cap

Year-to-date performance: -1%

Credit Suisse’s take: "We view BMRN as one of our highest conviction long-term ideas with a clear catalyst path to drive sustained growth (pegvaliase commercial launch, Phase 3 data for vosoritide late 2019, and Phase 3 data for valrox early 2020). Without a clear fundamental overhang in the name (the contra-case on BMRN we most often hear from investors is not on competition or pricing, for instance, but rather that key catalysts are too far off in the future), we expect the weight on BMRN shares could start to lift as investors reassess pegvaliase commercial launch expectations and refocus on positive fundamental pipeline developments."

Source: Credit Suisse

HCA Healthcare

Ticker: HCA

Sector: Healthcare Facilities

Year-to-date performance: +16.49%

Credit Suisse’s take: "HCA is a play on the long-term secular growth in demand for medical services. As the market leader, we believe HCA is poised to continue to generate above-average volume growth and market share gains. The company has strong positioning in large urban markets and continues to invest in its existing hospital operations to improve access and expand its reach. Given the company’s low leverage profile coupled with its strong FCF generation and track record for returning capital to shareholders, capital deployment is a further differentiator for HCA."

Source: Credit Suisse

Express Scripts

Ticker: ESRX

Sector: Healthcare Technology & Distribution

Year-to-date performance: +4.25%

Credit Suisse’s take: "With a deal spread now approaching 15% as of June 1, ESRX remains our top pick in our HCT&D universe despite an ongoing proposed merger with leading health insurer Cigna."

Source: Credit Suisse

UnitedHealth Group

Ticker: UNH

Sector: Managed Care

Year-to-date performance: +12.92%

Credit Suisse’s take: "With almost $225 billion in revenues, UNH is a Dow component stock that represents a compelling core holding to play health care’s secular growth. UNH targets attractive long-term EPS growth of 13-16%. UNH’s health benefits franchise (UHC) is positioned to capture share and grow earnings. UHC’s relationship with Optum enables it to manage medical costs effectively, enhancing the competitiveness of its offerings."

Source: Credit Suisse

Merck Pharmaceuticals

Ticker: MRK

Sector: Pharmaceuticals

Year-to-date performance: +10.85%

Credit Suisse’s take: "MRK is our Top Pick in our universe driven by the strong uptake of Keytruda monotherapy and our expectation of rapid uptake in combination with Alimta in additional 1L non-small cell lung cancer patients after full KEYNOTE-189 full data release at this year’s AACR. MRK is also positioned to pursue business development deals using its large cash reserves, further boosted by corporate tax reform."

Source: Credit Suisse

Bombardier

Ticker: Bombardier (Toronto)

Sector: Aerospace & Defense

Year-to-date performance: +64.19%

Credit Suisse’s take: "Our outperform thesis is based on the following: (1) We believe in the turnaround story, and note that this management team has consistently hit targets during its first three years; (2) We believe additional CSeries orders are likely following the JV transaction with Airbus, which the companies hope to close before the Farnborough Air Show in July; (3) beyond CSeries, other businesses are improving with BT backlog and sales expanding nicely, and BT, Bizjet and Aerostructures all enjoying solid margin improvement; (4) even after the 7% dilution from the offering, shares remain extremely attractive on our 2020 forecast."

Source: Credit Suisse

FedEx

Ticker: FDX

Sector: Airfreight & Ground Transport

Year-to-date performance: +0.07%

Credit Suisse’s take: "FDX is our top pick, as a stepdown in Ground capex in conjunction with accelerating volumes and solid pricing should lead to meaningfully better Ground margins. TNT operations are also back to normal and its integration presents an opportunity to generate earnings growth as FDX executes on its plan to improve operating profit at the combined Express business by $1.2-1.5B by FY20 vs. FY17. In the longer term, we expect the USPS to raise prices for parcel delivery, which should act as a secular tailwind that lifts pricing across the entire industry."

Source: Credit Suisse

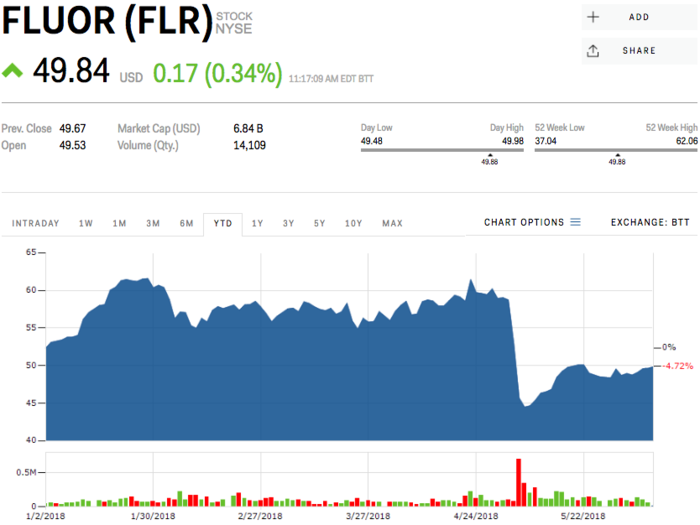

Fluor

Ticker: FLR

Sector: Engineering & Construction

Year-to-date performance: -4.72%

Credit Suisse’s take: "Given the outperformance of broader industrials, and with the market near an all-time high, we believe investors will gravitate back to E&C, as fundamentals for the group are improving. We believe FLR will be the go-to name, viewed as a higher-quality bellwether with a diverse end market offering, and more important a more cyclical growth bias. Furthermore, with commodity CapEx improving, FLR is best positioned competitively."

Source: Credit Suisse

Deere & Co.

Ticker: DE

Sector: Machinery

Year-to-date performance: -0.91%

Credit Suisse’s take: "We believe DE could be the breakout stock this year and would draw similar analogies to CAT. We would buy the stock when it is clear markets are bottoming versus looking for green shoots. DE's story into 2019 looks even more encouraging. In addition to what will still be early innings of a Farm Equipment recovery, DE's earnings beyond 2018 benefit from the lack of one-time items (purchase accounting/deal costs) in Wirtgen's margins (margins go from 2-3% in FY'18 more toward the 11-12% range), cost synergies associated with Wirtgen and potential for share repurchase again post the debt pay-down."

Source: Credit Suisse

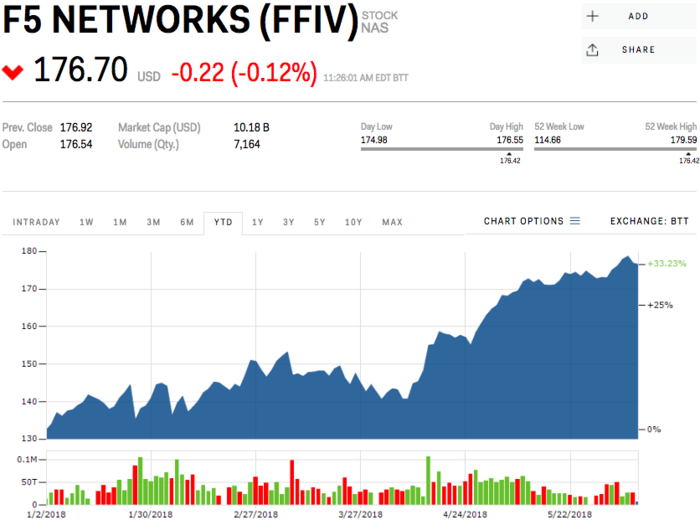

F5 Networks

Ticker: FFIV

Sector: Communications & Networking Equipment

Year-to-date performance: +32.23%

Credit Suisse’s take: "FFIV is the ADC market leader and its solutions are well positioned to grow as enterprises shift their workloads into hybrid cloud environments. In addition, FFIV has been transitioning well into a recurring revenue stream, deserving a multiple premium."

Source: Credit Suisse

Alphabet

Ticker: GOOGL

Sector: Consumer Internet

Year-to-date performance: +5.5%

Credit Suisse’s take: "Our Outperform investment thesis for GOOGL remains predicated on the following factors that can potentially drive material increases to our current estimates and hence share appreciation: (1) Ongoing monetization improvements in Search advertising through product updates such as Expanded Text Ads and Individual Bid Adjustments, (2) Greater-than-expected revenue contribution and margin expansion within Google's larger nonSearch businesses—namely YouTube (Bumper Ads) and Google Play (App Install, Sponsored Ads), (3) Optionality, upward bias to estimates, and long-term shareholder value creation from new monetization initiatives such as Maps as well as the eventual commercialization of Google's Other Bets."

Source: Credit Suisse

Equinix

Ticker: EQIX

Sector: Datacenter REITs

Year-to-date performance: -9.91%

Credit Suisse’s take: "Despite solid 1Q18 results (See our note: EQIX: Solid 1Q18 Earnings Results), EQIX continues to trade near its 12-month lows on a P/FY2 AFFO multiple. We believe the upcoming investor day will re-ignite interest in the stock. EQIX is the most global and distributed data center REIT along with being the market interconnection leader."

Source: Credit Suisse

PayPal

Ticker: PYPL

Sector: Financial Technology & Payments

Year-to-date performance: +13.37%

Credit Suisse’s take: "We are incrementally positive on PYPL following the acquisition of iZettle on May 16, which signals PYPL’s expanding strength as fin-tech consolidator and leader in digital financial services. Recommend the stock for exposure to fast-growing online payments industry, leading consumer wallet platform"

Source: Credit Suisse

Analog Devices

Ticker: ADI

Sector: Semiconductors

Year-to-date performance: +11.07%

Credit Suisse’s take: "ADI is well positioned, with more than 80% of revenue in more favorable I/A/I buckets and well levered to (1) Accelerating penetration of ADAS, A2B, and BMS, (2) More integrated transceivers in Infrastructure, (3) HITT Rev synergies especially in Mil/Aero, (4) Factory Automation, and (5) Emerging opportunities in Healthcare. The addition of LLTC provides a significantly larger and leverageable position in Power Management which positions ADI to benefit from the proliferation of silicon in non-traditional applications. While scale has not historically been a strategic imperative in analog, we see increasing silicon content in non-traditional areas driving customers to seek fewer suppliers with greater capabilities over-time; providing the basis for faster than historical share gains."

Source: Credit Suisse

Lam Research

Ticker: LRCX

Sector: Semiconductor Research

Year-to-date performance: -1.32%

Credit Suisse’s take: "We believe LRCX is the best way to play secular growth in Data, and believe that the company is growing secularly but priced as a cyclical. We see potential for multiple expansion (valuation as growth company supports >25x P/E vs current 12x), but even assuming it continues to trade as a cyclical at 3x on EV/sales, growth targets could support a $45-51bn EV by 2021, implying a ~$315-350 per share by end of 2020. We would also note that LRCX has historically provided conservative target models."

Source: Credit Suisse

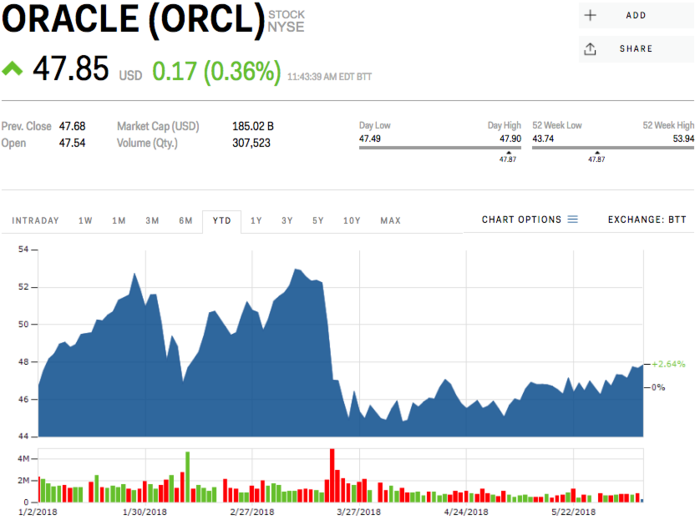

Oracle

Ticker: ORCL

Sector: Software

Year-to-date performance: +2.64%

Credit Suisse’s take: "We are constructive on Oracle’s autonomous cloud DBaaS opportunity and resurgence in license revenues, while our field work validates Oracle’s strength in Cloud ERP applications. (1) We view the release of the Autonomous Database cloud (Data Warehouse Cloud GA in March 2018, OLTP GA in mid-2018) as significant catalysts. Shift to Autonomous Database cloud generates efficiencies for the customers (~50% three-year TCO savings vs. on-prem), and encourages spending on additional capabilities. For example 70% of on-premise ERP deployments run without Disaster Recovery (DR), but greater number of customers add this functionality in the cloud. (2) We expect continued stabilization of Oracle’s license business, bolstered by its BYOL or “Bring Your Own License” program, continued 12c refresh, and resurgent IT datacenter spend."

Source: Credit Suisse

1. FMC

Ticker:

Sector:

Year-to-date performance:

Credit Suisse’s take:

Popular Right Now

Popular Keywords

Advertisement