Buy these 14 stocks set to benefit most from the surge in year-end holiday spending: Morgan Stanley

James Faris

- Holiday spending is expected to rise from last year's record high.

- However, elevated inflation has made many consumers especially deal-conscious.

Americans are gearing up for one of their favorite seasonal activities: shopping 'til they drop.

End-of-year spending is expected to be robust once again, according to a new note from Morgan Stanley based on the Wall Street giant's survey of roughly 2,000 US consumers.

"This holiday season is likely to see stronger spending than last," Morgan Stanley strategists led by Michelle Weaver wrote in a November 13 note, citing sentiment from her firm's economists.

The key finding from the survey is that about a third of respondents plan to spend more over the holidays than they did last year, while only 22% or so plan to cut back. About 37% of consumers said they anticipated spending about as much as they did last November and December.

Holiday spending reached a record of over $964 billion in 2023, which was up 3.8% from 2022, according to the National Retail Federation. That jump was near the higher end of the NRF's estimate and outpaced inflation, which was 3.4% last December and 3.1% in the prior month.

Rich shoppers are ready to spend, deals or no dealsAlthough price growth is down substantially from its highs, it ticked up in October and remains problematic for most consumers. Persistent inflation has made many shoppers hungry for deals.

"Companies could see a little more holiday cheer this year, but spending isn't likely to increase across all categories as consumers remain selective," Weaver wrote.

To that point, roughly half of consumers say that they expect stores to cut prices over the holidays. By comparison, only 28% of shoppers expect price hikes, which is down from 33% of respondents in 2022, when inflation was just starting to fall from its peak.

Without discounts, an eye-catching 69% of survey respondents indicated that they'd reduce their spending at least modestly, in part by buying cheaper goods. But some shoppers seem to be insulated from elevated prices, as 27% said they'd spend like normal without major sales.

Unsurprisingly, this discrepancy is most evident across income segments. Lower-income shoppers are most likely to trim their spending without deals, while upper-income households are most likely to increase their spending compared to last year.

"The setup for the consumer remains tricky as higher-income consumers continue to drive spending, while lower-income consumers feel the impact of multiple years of elevated prices," Weaver wrote.

Another under-the-radar headwind for businesses is the calendar. There are just 27 days between Black Friday and Christmas, which is the shortest possible holiday shopping season.

How to ride the end-of-year spending waveAlthough almost everyone is feeling the pinch from higher prices, there are several reasons to be upbeat about holiday spending, not counting Morgan Stanley's findings.

Money is flowing into goods at a faster pace after lofty interest rates had weighed on spending earlier this year, Weaver wrote. That momentum may carry into the holiday season.

Consumer spending also grew faster than last year on an inflation-adjusted basis in the first nine months of 2024, and there haven't been any economic hiccups big enough to derail that.

However, that's not to say that all companies will equally enjoy that surge in holiday spending.

"Consumers are not planning to go on a spending spree across categories and will continue to allocate budgets selectively," Weaver wrote. "This is likely to create an environment of leaders and laggards with industries exposed to lower-priced goods faring better than those exposed to big-ticket items."

In the note, Weaver and her team outlined 16 companies with significant exposure to holiday spending, though only 14 of those stocks have bullish ratings from Morgan Stanley analysts. These firms are from various industries, including e-commerce, retail, and travel.

Below are those 14 overweight-rated stocks, sorted alphabetically by industry and within their industries, if applicable. Each is accompanied by its ticker, market capitalization, price-to-earnings (P/E) ratio, industry, and commentary about that industry from Morgan Stanley.

1. Alaska Air

Ticker: ALK

Market cap: $6.5B

P/E ratio: 20.8x

Industry: Airlines

Industry commentary: “We continue to expect a strong holiday season ahead as demand for air travel has continued to show strength and management teams have been pointing to a solid forward booking curve for the holidays.

“Despite concerns around the health of the consumer and the supply vs. demand picture, management teams continue to point to strong travel demand, particularly during peak periods. This is evidenced in the supportive TSA data, which has continued to consistently come in above 2019 and 2023 levels.

“We remain encouraged by the strong data as it proves air travel demand remains resilient (and a priority among consumers), and we only expect this to continue as we enter the holidays.”

2. American Airlines

Ticker: AAL

Market cap: $9.2B

P/E ratio: 40x

Industry: Airlines

Industry commentary: "We continue to expect a strong holiday season ahead as demand for air travel has continued to show strength and management teams have been pointing to a solid forward booking curve for the holidays.

"Despite concerns around the health of the consumer and the supply vs. demand picture, management teams continue to point to strong travel demand, particularly during peak periods. This is evidenced in the supportive TSA data, which has continued to consistently come in above 2019 and 2023 levels.

"We remain encouraged by the strong data as it proves air travel demand remains resilient (and a priority among consumers), and we only expect this to continue as we enter the holidays."

3. Delta Air Lines

Ticker: DAL

Market cap: $41.6B

P/E ratio: 9x

Industry: Airlines

Industry commentary: "We continue to expect a strong holiday season ahead as demand for air travel has continued to show strength and management teams have been pointing to a solid forward booking curve for the holidays.

"Despite concerns around the health of the consumer and the supply vs. demand picture, management teams continue to point to strong travel demand, particularly during peak periods. This is evidenced in the supportive TSA data, which has continued to consistently come in above 2019 and 2023 levels.

"We remain encouraged by the strong data as it proves air travel demand remains resilient (and a priority among consumers), and we only expect this to continue as we enter the holidays."

4. United Airlines

Ticker: UAL

Market cap: $29.5B

P/E ratio: 10.8x

Industry: Airlines

Industry commentary: "We continue to expect a strong holiday season ahead as demand for air travel has continued to show strength and management teams have been pointing to a solid forward booking curve for the holidays.

"Despite concerns around the health of the consumer and the supply vs. demand picture, management teams continue to point to strong travel demand, particularly during peak periods. This is evidenced in the supportive TSA data, which has continued to consistently come in above 2019 and 2023 levels.

"We remain encouraged by the strong data as it proves air travel demand remains resilient (and a priority among consumers), and we only expect this to continue as we enter the holidays."

5. Knight-Swift Transportation

Ticker: KNX

Market cap: $9.2B

P/E ratio: 247.5x

Industry: Freight Transportation

Industry commentary: "The US domestic freight transportation market has been dragging along the bottom for roughly the last two years, putting us in a reasonably unprecedented extended downcycle. However, we expect an inflection is imminent (if not already in motion), as evidenced by several data points and positive company commentary on improving yield and peak project opportunity (despite lackluster 3Q results)."

6. Schneider National

Ticker: SNDR

Market cap: $5.5B

P/E ratio: 49.3x

Industry: Freight Transportation

Industry commentary: "The US domestic freight transportation market has been dragging along the bottom for roughly the last two years, putting us in a reasonably unprecedented extended downcycle. However, we expect an inflection is imminent (if not already in motion), as evidenced by several data points and positive company commentary on improving yield and peak project opportunity (despite lackluster 3Q results)."

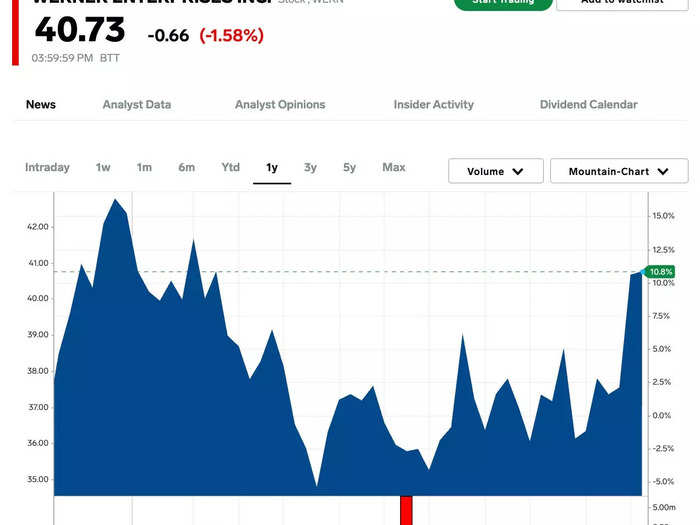

7. Werner Enterprises

Ticker: WERN

Market cap: $2.5B

P/E ratio: 56.2x

Industry: Freight Transportation

Industry commentary: "The US domestic freight transportation market has been dragging along the bottom for roughly the last two years, putting us in a reasonably unprecedented extended downcycle. However, we expect an inflection is imminent (if not already in motion), as evidenced by several data points and positive company commentary on improving yield and peak project opportunity (despite lackluster 3Q results)."

8. Target

Ticker: TGT

Market cap: $71.4B

P/E ratio: 16x

Industry: Hardlines/Broadlines/Food Retail

Industry commentary: "Durable goods spending has slowed in '24, but the backdrop is normalizing, which creates a more favorable setup for the holiday season. Most retailers face low Q4 expectations, and this is coupled with lower inflation, a relatively stable consumer, and minimal inventory/promotional risk.

"We expect the durable goods reversion trend to continue into the '24 holiday season, which could set up a more neutral backdrop for holiday spending and leave room for upside. This outlook is supported by the National Retail Federation which expects holiday '24 spending will increase ~3% y/y. Consensus comps indicating a favorable setup for 4Q. Consensus is modeling a ~20 bps acceleration in 4Q vs. 3Q comps for holiday-exposed retailers vs. a ~40 bps acceleration for our broader coverage. This mild acceleration represents a relatively low bar, in our view, and creates a favorable setup for comp beats in 4Q."

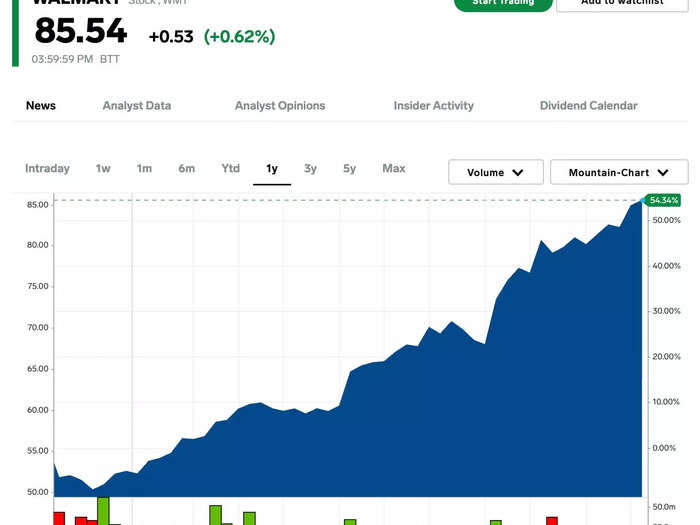

9. Walmart

Ticker: WMT

Market cap: $687.3B

P/E ratio: 44.5x

Industry: Hardlines/Broadlines/Food Retail

Industry commentary: "Durable goods spending has slowed in '24, but the backdrop is normalizing, which creates a more favorable setup for the holiday season. Most retailers face low Q4 expectations, and this is coupled with lower inflation, a relatively stable consumer, and minimal inventory/promotional risk.

"We expect the durable goods reversion trend to continue into the '24 holiday season, which could set up a more neutral backdrop for holiday spending and leave room for upside. This outlook is supported by the National Retail Federation which expects holiday '24 spending will increase ~3% y/y. Consensus comps indicating a favorable setup for 4Q. Consensus is modeling a ~20 bps acceleration in 4Q vs. 3Q comps for holiday-exposed retailers vs. a ~40 bps acceleration for our broader coverage. This mild acceleration represents a relatively low bar, in our view, and creates a favorable setup for comp beats in 4Q."

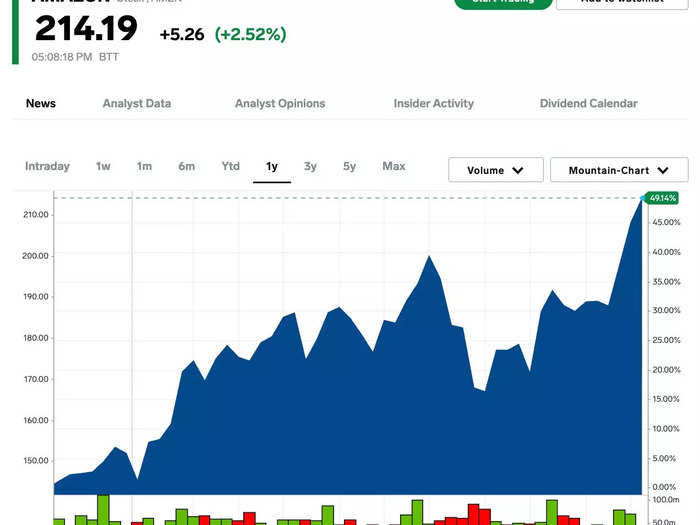

10. Amazon

Ticker: AMZN

Market cap: $2,250B

P/E ratio: 45.9x

Industry: Internet/ecommerce

Industry commentary: "Ecommerce growth has been pressured as of late with non-store sales tracking ~MSD, below '23 & '22 levels through 2Q & 3Q. Weakness has been focused in discretionary goods with pinched consumer spending while outsized growth has come from non-discretionary categories like groceries & everyday essentials. As a result, durable goods spending is now tracking below the pre-COVID average without indications of an inflection.

"The shorter holiday season may also have an impact, especially for eComm players with longer average delivery times. Although there are cautionary signs, the holiday outlook looked similarly soft last year with eComm growth decelerating through 3Q in a weaker consumer spending environment, but ended better than expected with ~10% y/y US eComm growth.

"It is possible we see a similar dynamic unfold in '24, especially as our survey largely screened positive as forward intentions are improving with 35% of respondents planning to increase spend, up ~11pts y/y … the highest level we have recorded. The rationale for increasing spend is encouraging with material upticks in responses for buying more gifts, increased income, and better credit (each up ~5pts y/y). Elevated higher-income spend could also benefit online sales given greater exposure, and we do expect eComm share gains to accelerate slightly (~30 bps) in 4Q."

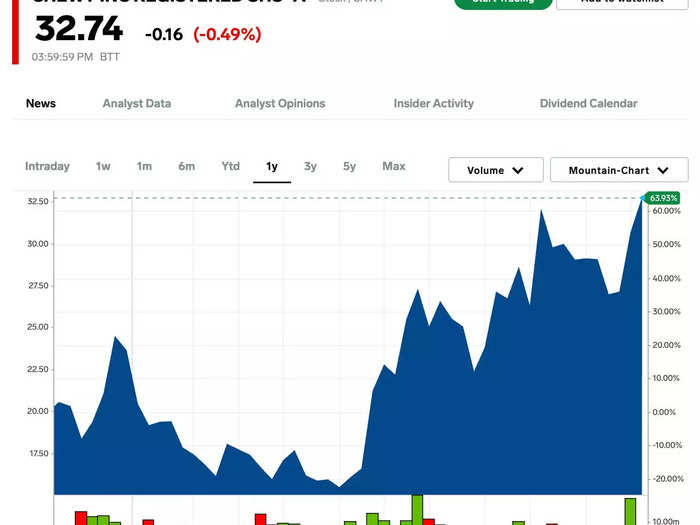

11. Chewy

Ticker: CHWY

Market cap: $13.7B

P/E ratio: 39.3x

Industry: Internet/ecommerce

Industry commentary: "Ecommerce growth has been pressured as of late with non-store sales tracking ~MSD, below '23 & '22 levels through 2Q & 3Q. Weakness has been focused in discretionary goods with pinched consumer spending while outsized growth has come from non-discretionary categories like groceries & everyday essentials. As a result, durable goods spending is now tracking below the pre-COVID average without indications of an inflection.

"The shorter holiday season may also have an impact, especially for eComm players with longer average delivery times. Although there are cautionary signs, the holiday outlook looked similarly soft last year with eComm growth decelerating through 3Q in a weaker consumer spending environment, but ended better than expected with ~10% y/y US eComm growth.

"It is possible we see a similar dynamic unfold in '24, especially as our survey largely screened positive as forward intentions are improving with 35% of respondents planning to increase spend, up ~11pts y/y … the highest level we have recorded. The rationale for increasing spend is encouraging with material upticks in responses for buying more gifts, increased income, and better credit (each up ~5pts y/y). Elevated higher-income spend could also benefit online sales given greater exposure, and we do expect eComm share gains to accelerate slightly (~30 bps) in 4Q."

12. Gap

Ticker: GAP

Market cap: $8.4B

P/E ratio: 11.1x

Industry: Softlines Retail & Brands

Industry commentary: "Holiday headwinds & tailwinds are mostly balanced in number, in our view — leaving us neutral to slightly positive on holiday [this year], with the view that leaders & laggards will be made clearer. Though we caution a number of '24e holiday headwinds — including 1) a challenging calendar (i.e., the 53rd week reversal & compressed holiday shopping period), 2) difficult y/y compares, & 3) potentially higher y/y discounting activity — we also highlight a nearly equal number of positive offsets, including 4) constructive holiday spending survey results, 5) favorable weather compares, & 6) conservative retail hiring trends.

"When considered against what we see as a mostly ~fair consensus 4Q24 EPS bar, seemingly neutral market sentiment, as well as possible tailwinds from pent-up demand post-election &/or on improved weather, we altogether lean neutral to slightly positive on the holiday season. More granularly, we think the 4Q24/holiday backdrop will prove highly competitive in light of these various puts & takes — creating a leaders/laggards dynamic in our coverage."

13. Apple

Ticker: AAPL

Market cap: $3,400B

P/E ratio: 37x

Industry: Tech Hardware

Industry commentary: "We are cautious on consumer electronics sales this holiday season. Consumer hardware spending intentions remain negative as we near the holiday season. One-month-forward net spending intentions (i.e., expectations for spending next month vs. this month) on consumer electronics downticked 3 points M/M to -7%, while one-month-forward PC net spending intentions downticked 2 points M/M to -14%. The M/M deterioration in next month consumer electronics and PC spending intentions signals caution for Black Friday/Cyber Monday sales this year as this metric has upticked M/M in October in each of the last three years.

"Although a net 14% of consumers expect to spend more vs. less (broadly) during the holidays, consumers are less positive on big ticket and/or discretionary items, including consumer electronics, with a net 5% of respondents expecting to spend less vs. more on consumer electronics this holiday season."

14. Hasbro

Ticker: HAS

Market cap: $8.8B

P/E ratio: N/A

Industry: Toys, Leisure Products, & Services

Industry commentary: "Overall, our consumer survey results look promising, indicating consumer spending is likely to be stronger this holiday season than last, with intentions increasing y/y in all of our covered categories. Most consumer goods companies we follow guided 4Q cautiously, which was prudent, in our view, given uncertainty around the election/macro and a shorter holiday season y/y with five fewer days between Black Friday and Christmas.

"However, results from our survey suggest discretionary spending could reaccelerate this holiday season, with a net 15% of consumers planning on increasing their total holiday budget this year, a pronounced 18 point increase from this time last year. Additionally, while the majority of consumers are still likely to shop during elevated promotional periods (72% of consumers expect to shop between Black Friday and Christmas), 26% of consumers plan to do most of their shopping before Black Friday/ Cyber Monday this year, a 5 point increase vs. last year, indicating, to us, further signs of increased consumer confidence and important considering the shorter holiday shopping window overall.

"Consequently, we are cautiously optimistic that the holiday season could prove better than feared though continue to believe there will be relative winners and challenged companies with our survey work indicating those with more accessible price points are best positioned."

Popular Right Now

Popular Keywords

Advertisement