Insurance Cover: Which Term Plan Is For You ?

That’s peanuts, literally. The daily cost works out to Rs 22-25, less than that you pay for a cola. Term plans are no longer the plain vanilla products they used to be till a few years ago. Insurance companies have crafted innovations that suit various customers and situations. Worried about inflation? You can buy a plan where the insurance cover increases every year. Won’t be able to spare money later? Buy a policy that does not require you to pay for the entire term.

Your nominee is not investment savvy? A few companies offer policies that don’t give a lump sum on death, but stagger the payment over 10-15 years. Think a term plan is a waste of money? Some plans give back the entire premium. Not all of these innovations are good for the customer. In our cover story this week, we dissect the variations of the simple term policy to tell you which is the best way to cover your life.

Offline term insurance

Term plans are straightforward products and you can rarely go wrong while buying one. Even so, you can end up with an unsuitable policy or fall into a trap like businessman Sham Kalra (see picture). For most buyers, the premium alone is the deciding factor. Here’s what you should keep in mind when you go shopping for a term plan.

How long is the tenure? Insurance companies usually highlight premium rates for 30-year-old buyers for 20-year plans. It’s a clever ploy because the premiums for this low-risk age band of 30-50 years are very low. However, such a plan will end when the person’s insurance needs are very high. At that age, a new policy will cost him a bomb. He might even be denied the cover if his health is not good. Don’t take a 15-20 year plan that will terminate when you are in your 50s. Buy a cover till the age of 60-65 years.

How solid is the company? An insurance policy is a long-term contract, but there are indications that a few insurance companies may not be around for the long term. The sector is going through a bad phase and several foreign partners are looking for buyers for their stakes. There is a possibility that loss-making companies may be taken over by larger players. Though the insurance regulator will ensure that all policies are honoured by the new owners, it’s best to choose a company that is doing well and is not likely to shut shop.

Online term plan

Online term plans have become very popular in the past three years, but many customers harbour grave misconceptions about these policies. Online plans are roughly 30-40% cheaper than their offline cousins (see table), but the low premium rates make people feel that there is a catch in the policy terms and claims might not be honoured. “There is no mystery behind the low premiums of an online plan,” says T R Ramachandran, CEO and managing director of Aviva Life Insurance. The premium is low because there is no intermediary and the online buyer is perceived as a low-risk customer. He is educated, earns reasonably well, is concerned about protection and is likely to have health insurance as well. In case of a medical emergency, he may be able to quickly reach a hospital and access specialised medical treatment. These factors combine to lower the risk for the insurer.

When you compare term plans, remember that the online quote is based on the assumption that you carry the normal risk in terms of health, family medical history and occupation. When you submit your details online and pay the premium, the cover starts immediately but is subject to your medical tests and actuarial screening. If the medical tests show that you are suffering from a condition, have a family history of an ailment or are exposed to a specific risk at work, the premium quoted is likely to get bumped up. You have the option to decline the higher premium and your money will be refunded after deducting the expenses incurred on the medical check-up.

Increasing cover

A cover of Rs 1 crore may seem sufficient at today’s prices, but you also need to factor in the impact of inflation. “The value of Rs 1 crore today is far less than what it was 10 years ago and what it will be 10 years from now,” says Sanjeev Kumar Pujari, appointed actuary, SBI Life Insurance. Even 8% inflation will reduce the value of Rs 1 crore to less than Rs 15 lakh in 25 years.

To get around this problem, some insurance companies offer plans where the cover increases every year. The Smart Shield plan from SBI Life has an option where the sum assured increases by 5% every year. If you take a Rs 50 lakh cover, it will increase by Rs 2.5 lakh every year. By the fifth year, it would be Rs 60 lakh (see table) and Rs 72.5 lakh by the tenth year.

We found that the regular Smart Shield term plan from SBI Life is a much better option. A Rs 1 crore level term cover will cost you just a tad more than the Rs 50 lakh increasing cover plan charges (see table). The regular level cover plan offers greater coverage at almost the same price. Only in the 25th year does the sum assured of the increasing cover plan exceed the death benefit under the regular plan. This does not justify the higher premium of the increasing cover plan.

The insurance needs of an individual are the highest when he is in his 40s. As he grows older and most of his financial goals are met, the need for insurance cover comes down. So, the buyer may not require a cover of Rs 1.225 crore when he is 60 years old.

Loan protection cover

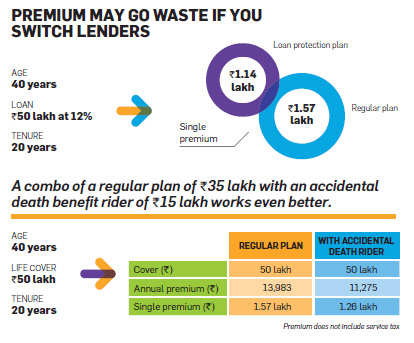

Financial planners advise that you should cover big-ticket loans with an insurance policy. In case something happens to you, your family will not have to sell the house because you are no longer there to pay the EMIs. Home loan protection plans offered by insurance companies are designed to cover loans. The insurance cover is linked to the loan amount and progressively comes down as the outstanding loan is paid off. These are single premium policies where the entire premium is paid upfront.

However, these decreasing sum assured plans are not a good idea. A regular term plan for the same amount will work out to be cheaper and far more useful. It would continue to cover the borrower even after the home loan has been repaid. The HDFC data shows that the average loan is taken for a period of 16 years, but gets prepaid in 8-9 years. Moreover, if a borrower refinances the loan and moves to another lender, his policy goes waste. For the past 6 months, Delhi-based Sanjeev Kumar (see picture) has been trying to get a refund of the Rs 2.21 lakh premium he paid for a 10-year policy in 2012. “The lender and the insurance company misguided me when they sold this plan along with the home loan,” he says wryly.

Single premium

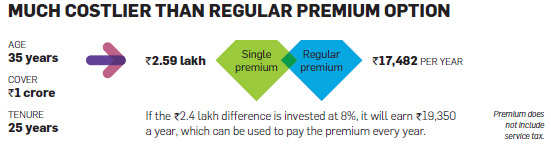

As the name suggests, single premium policies require a one-time lumpsum payment for the entire tenure of the plan. Since this premium is paid upfront, it is lower than that you will pay for a regular premium plan over the entire term. However, these are not comparable figures. The opportunity cost of the lump-sum payment must also be factored in. If the Rs 2.4 lakh extra charged by the single premium plan is invested in a risk-free option offering 8% return, it will yield Rs 19,350 every year. This income can be used to pay the annual premium every year. As our calculation shows, a buyer who opts for a regular payment plan will be able to save a neat sum even after paying the annual premium for the entire tenure of the plan.

Still, single premium policies are hot favourites among buyers because they don’t require paying the premiums year after year. The taxpayers who delay their tax planning till the dying days of the financial year see these single premium plans as a perfect solution for their Section 80C investments. In the first nine months of the current year, life insurance companies registered a growth of 22.5% in new premium income. Most of the growth came from single premium policies, which rose 43%.

Though they are costlier, single premium policies work in certain circumstances. One of the biggest challenges before insurance buyers is to continue paying the premiums over the full tenure of the plan. Many policyholders either change their minds after a few years, miss the due date or cannot spare resources to continue the policy. A single premium policy, where the entire premium for the term has been paid upfront, does away with this problem.

These single bullet plans also work for those who have an irregular income or who are not very sure about their future financial situation. If you are a spendthrift and tend to blow away your money, it may not be a bad idea to put a portion of your annual bonus in a single premium plan.

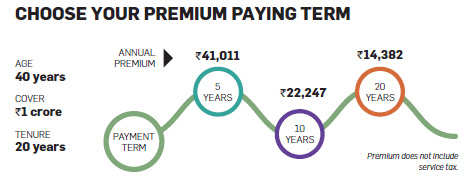

Limited payment period

Till recently, term plan customers had to either opt for a single premium option or a regular premium option that required annual payments for the full term. Now some companies are offering limited premium payment options as well. In many ways, this limited premium payment plan is only an extension of the single premium option. It’s only that instead of one lump-sum payment at the beginning of the term, the premium payment is staggered over 5-10 years.

When a person is young and doesn’t have too many responsibilities, he is likely to have a higher investible surplus. However, as he grows older and responsibilities increase, he may not be able to spare enough money. Limited premium payment plans are designed for such people. Buyers of the iRaksha Supreme plan from Tata AIA Life Insurance can opt to pay for 5 or 10 years.

Of course, this benefit does not come without a hefty price. As the graphic shows, the premium of the 5-year and 10-year option is significantly higher than that of a regular plan, which requires annual payments for the full term.

Such plans will be especially useful for double-income couples, who are planning to start a family in a few years and might switch to a single income after that. Or those who are planning a big-ticket expense like purchasing a house in the next 4-5 years. While such families are comfortably placed right now and can afford a higher premium, they might not be able to find the money to pay the premium in later years when their income shrinks and expenses bloat.

The argument against single premium plans holds true for these limited premium payment plans as well. The buyer is paying a considerably higher premium in the initial years. A regular plan may seem a better option if you are sure that you can continue the plan for the rest of the term. If you are not disciplined enough or doubt if you will be able to spare the money later, go for the limited premium payment period plan.

Staggered payouts

A term insurance plan will pay your nominee a huge sum if something untoward happens to you, but can your spouse or children handle the lump-sum payment? Indians score poorly on financial literacy and the friendly executive from the bank will offer advice that suits his pocket rather than your nominee’s needs.

Can your nominee deploy the amount in a way that all the financial goals you had chalked out are achieved? Or will unscrupulous financial advisers and greedy relatives cheat your family of the money?

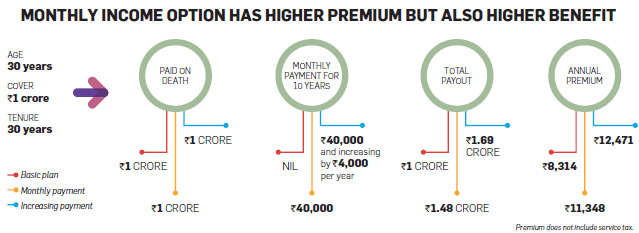

With this in mind, insurance companies have launched term plans that do not pay a lump sum, but stagger the payment over 10-15 years. The Online Term Plan from Max Life Insurance pays the full sum on death like any other term plan, but also gives a monthly payment for the next 10 years. Of course, the premium is higher if you opt for the monthly income compared to a basic term plan. It is even higher if you opt for the monthly payment to increase by 10% every year (see graphic). Inflation can reduce the purchasing power of the monthly payment.

The Max Life Insurance offering is basically two plans bundled into one. The lumpsum payment can be used for settling outstanding loans and other liabilities of the deceased person. The monthly payment takes care of the living expenses of the family. As the graphic shows, the monthly income option is not costlier than a basic plan. The inflation-adjusted payout is Rs 1.32 crore, while the annual premium is Rs 11,348. A basic term cover of Rs 1.32 crore would cost the same. Similarly, the increasing income option pays Rs 1.48 crore after adjusting for inflation. Its premium is the same as that for a basic cover of Rs 1.48 crore.

The i-Secure Term Plan from Aviva India pays only 10% of the sum assured on death and the rest is paid as yearly instalments of 6% each over the next 15 years. So, if the cover is Rs 1 crore, the family will get Rs 10 lakh immediately on death and Rs 6 lakh every year for the next 15 years. While the total payout under this arrangement will add up to Rs 1 crore, inflation will reduce the value of the annual payments over the years. We found that the inflation-adjusted value of the yearly payouts is actually Rs 48.36 lakh. If you add the Rs 10 lakh received immediately on death, the total payout comes to Rs 58.36 lakh. Given the lower benefit, i-Secure Term Plan is priced almost 60-65% lower than the existing i-Life online plan from Aviva. So, in real terms, the new plan costs almost the same as the existing plan. It’s only that the staggered payments ensure the money is not frittered away but used prudently. “This plan is especially useful for a family which will not be able to manage a lump-sum payment,” says a spokesperson of Aviva India.

Rituraj Bhattacharya, head, product development and market management, Bajaj Allianz, says the company is also ready to launch a term insurance plan that gives out a staggered death benefit.

An added advantage of these plans is that unlike an annuity from a pension plan, the monthly income received from the insurance company will be tax-free under Section 10(10d). Of course, that’s true for the lumpsum payment as well, but the income from investments is taxable.

With return of premium

Some people think term plans are a waste of money because they don’t return anything to the customer at the end of the term. They argue that unless an insurance policy offers maturity benefits, one should not buy it. For them, an endowment policy that pays back a large amount at the end is a good buy, irrespective of the fact that the returns are less than 6%. They fail to see that the mortality premium, whether charged by a pure protection term plan or an endowment policy, can never have a maturity value. It is so difficult to reason with this mindset that insurance companies are forced to offer plans with return of premium. The i-Shield plan from Aviva India returns the entire premium paid by the buyer at the end of the term.

However, don’t look at it as a great way of insuring your life at no cost. You get the money back without any interest. Also, the premium of the i-Shield plan is significantly higher than that of the i-Life plan from Aviva. You have to shell out almost Rs 15,000 more every year just to get it all back after 25 years.

As the graphic shows, in 25 years, 8% inflation would have reduced the purchasing power of Rs 5.17 lakh to just about Rs 75,000. On the other hand, if you took the regular i-Life plan and invested the difference (Rs 14,795) in an option that earns 8% annually, you would amass Rs 11.68 lakh in 25 years. That’s more than double of what the i-Shield plan will return to you at the end of the tenure.

Don’t look at your term plan premium as an investment. Just as you don’t get anything back from your house or vehicle insurance policy if there is no claim, the term plan premium is an expense that covers the risk to your life. Only if the policyholder dies does the family get the sum assured. Instead of buying a term plan that returns your premium, it is better to invest the difference in a mutual fund or bank deposit.Will your insurer keep its promise?

It’s A question that haunts all policyholders, and the data with Irda is not very heartening. The insurance regulator says private insurers rejected about 8% of the claims they received in 2012-13, while the LIC rejected 1.12%. The figures may not be comparable because any claim made within two years of buying a policy is investigated in detail and the settlement often gets delayed. Private insurers have been in the market for only 10-odd years, so many of the claims they receive are ‘early death’ claims. Some private insurers have just stepped out of the cradle, while the LIC is two years short of being a senior citizen.

Why do so many claims end up in the trash can? There can be several reasons. The policyholder may have held back certain key facts at the time of filling the application. Perhaps the form was filled up by an agent who, deliberately or otherwise, gave incorrect information.

Or maybe the company didn’t make an effort to verify the information while accepting the application. Whatever the reason, almost 8.5 lakh insurance claims, amounting to almost Rs 9,525 crore, were rejected in 2012-13.

Experts point out that the claim rejection figures are not for term plans alone but for a company as a whole. Claims get rejected usually due to fraudulent practices by the buyer or agent and lax underwriting by the company. This is possible in low-value policies. “However, term plans are a different ball game altogether. The applicant is careful about the information he provides and companies conduct proper underwriting to assess the risk,” says Swapan Khanna, cofounder of insurance research and advisory firm, I-Save.

When you apply for a term plan, you are subjected to stringent medical tests. The higher the sum assured, the more elaborate the tests; but the more extensive the medical tests, the lower is the premium. For example, the Click2Protect online plan from HDFC Life charges a premium of Rs 8,575 per year for a cover of Rs 49 lakh, but if the cover is Rs 50 lakh, the buyer is required to undergo more tests and, therefore, the premium is lower at Rs 6,000 per year.

Khanna says acompany’s claim settlement ratio does not have any bearing on the assessment of a claim. “Claims are assessed on the basis of the merits of a case,” he says. In other words, you can’t rest assured that a company with a high claim settlement ratio will pass a claim even if there is something suspicious. There is no need to lose sleep if your insurer has a low claim settlement ratio as long as you have honestly disclosed all information.

It’s best to be completely honest about your health, social habits, age and occupation when you apply for a term cover. Harshad Doshi’s (see picture) application was rejected by a company because he had kidney stones. However, another company accepted the risk and issued him a policy. The premium of your term plan is 60-80% higher if you consume tobacco in any form. So, it’s tempting to say one doesn’t smoke or chew gutka to keep the premium low, but nicotine traces can be detected in your blood even 2-3 years after kicking the habit. Besides, chest Xrays can have some telltale marks of the damage done by smoking. A buyer’s bid to save a few thousand rupees on premium may deny his nominee the sum assured.