Large deposits in bank accounts due to demonetization is expected to soften bond yields and also lower rate of interest in the economy as banks will be forced to use the extra cash to buy more government papers and rush to lend money to the customers, or do both. With people unable to spend due to tight liquidity, this could also lead to slower growth, which would leave enough space for the RBI to cut rates, economists and bond dealers said. (Source – Economic Times)

Large deposits in bank accounts due to demonetization is expected to soften bond yields and also lower rate of interest in the economy as banks will be forced to use the extra cash to buy more government papers and rush to lend money to the customers, or do both. With people unable to spend due to tight liquidity, this could also lead to slower growth, which would leave enough space for the RBI to cut rates, economists and bond dealers said. (Source – Economic Times)The lower and stable bond yields bring stability in the economy; however consistently reducing bond yields has an adverse impact on the financials of the companies especially where the employee benefits liabilities are concerned.

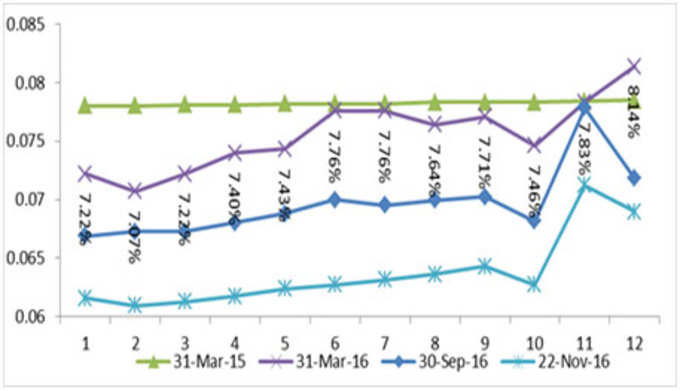

We can see from both the Graph as well as the table below, that Post Demonetization, the zero coupons Government bond yields as on 22nd November has dropped significantly. The zero coupons Govt Bond yields have fallen by 28 bps to 73 bps since September 2016 and by 79 bps to 149 bps since March 2016 over different tenures. Specifically Yields on a 10 year zero coupon bonds has fallen by 55 bps since 30th September 2016 and by 115 bps since 31st March 2016.

Fall in the Bond Yields has a direct impact on the balance sheet and the P&L of the organizations, as In India, the defined benefit obligations are determined with reference to the market yields at the balance sheet date on government bonds of appropriate tenure according to the Para 78 of the AS 15 (Revised 2005) and Para 83 of the Indian Accounting Standard (Ind AS) 19. Also, the currency and term of the government bonds need to be consistent with the currency and estimated term of the post-employment benefit obligations.”

While the total Employee benefit obligation depends on many factors, the impact of reduction by 50 bps in the discount rate is anywhere in between 0.83% to 8.28% depending on the Future working life time/Duration of the liabilities on which the Discount rate depends Assuming an Average future working life time of 10 years, in the post demonetization scenario, the impact of the decrease in bond rates may result in the liabilities to increase approximately by 5% since September 2016 and by 12% since March 2016 which for organizations with large liabilities is quite a big impact to the financials.

What Demonetization means for funded employee benefit schemes

Assets under funded post-employment benefit schemes are primarily invested in debt securities, the reduction in govt. bond yields will lead to reduced future earnings and hence more contributions may be required to match both the current and future liability. Though the self-managed investments may enjoy higher market/fair value of assets invested in the past at higher interest rates, the future contributions and reinvestments would be invested on lower yielding bonds. The trusts who have invested through the

Demonetization and Exempt Provident Funds

India’s labour ministry passed a new regulation on November 11 allowing for inactive employee

From the current EPF interest rate of 8.8% , it is unlikely that the Government would reduce the next year rate that steep to match the current bond yields. Given this scenario the exempt PF funds will have to meet any shortfall in the funds that may arise in future to meet the obligations .

Companies that have their own exempt fund have two future risks-

• Investing the new contributions in Bonds yielding the promised guaranteed interest.

• Reinvesting the monies from the matured bonds in Bonds yielding the promised guaranteed interest

For now the market/fair value of assets is on the higher side as the companies have invested in the past in bonds with high yields , however this advantage will be lost if the situation continues which appears to be a certainty for now.

May be it is time for companies with exempt provident fund trusts to re-look at their PF strategy.

The above article does not provide any legal/statutory advice and should only be used for general reference only.

(Image Credits: Economic Times)

(About the Author: The author of this note is Chitra Jayasimha, Actuary and Practice Leader, RFM at Aon Hewitt Consulting, India.)