IIM Bangalore students tell you what really led to a BREXIT and it's possible impact on Indian equities

Jun 27, 2016, 19:54 IST

Advertisement

Here take a look at what they have to say about Brexit:

Why wasn’t this anticipated?

As seen in the polls data, even till the last day there were more votes in favour of Bremain. However, the key folly is that the markets over-discounted the Remain stance when the fact is that it was always going to be a close call to begin with. Moreover, less than 5 hrs before the results came clear, the betting markets gave Remain a 88% chance of winning. According to us, some of the critical reasons for the deviation in expectation and actual result are as follows:

- The markets expected that the undecided voters would go towards status-quo i.e. Bremain.

- There was a big disconnect between the frustrated population and the political establishment

- The concern of UK citizens towards immigration overcame the fears of economic disruption that a departure could cause.

Advertisement

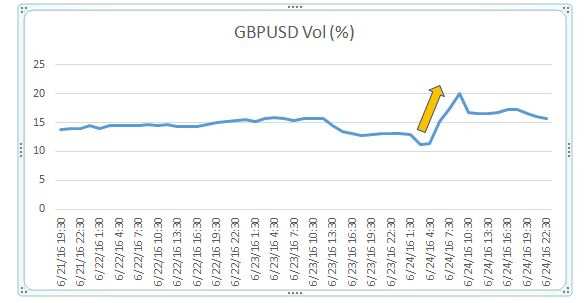

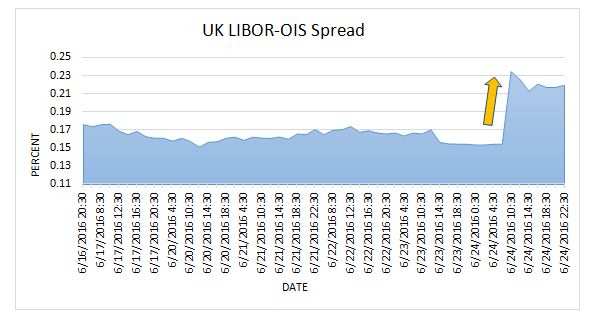

As we can see in the 2 graphs below, the 3 month GBPUSD options volatility spiked up a lot and so did the Libor – OIS Spread (because of underpricing) as soon as the event happened.

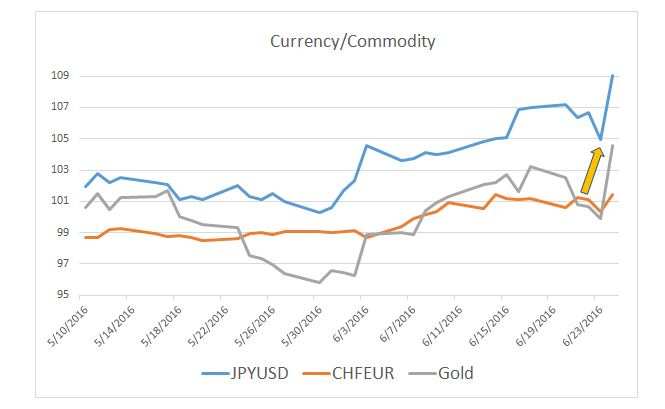

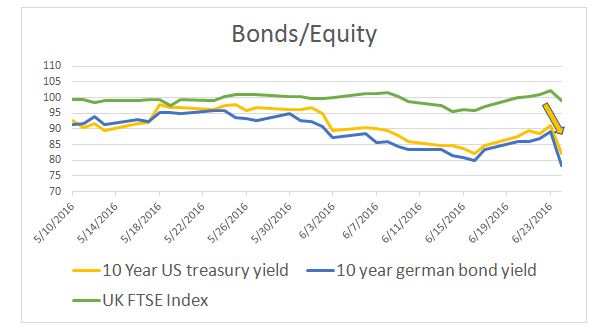

Movement in Asset Classes

The financial markets also didn’t expect it and hence there was a big correction in equity, currency and bond markets that otherwise would have been priced into trading. Referring to the assets in our earlier blog, there was a big movement towards safe haven assets.

Advertisement

Note – The graphs below have been adjusted to a base of 100 as on 17/3/2016. Hence, a value more than 100 means that respective asset is appreciating.

Brexit – Impact on Indian Equities

The negative impact of the Brexit vote was felt on Indian equities with nearly every stock in the Nifty plunging near the opening bell on Friday, 24th June. Overall the Nifty fell to a low of 7927 Pts from its opening at 8270 Pts before recovering to close at 8075 Pts. The major impact was felt on the IT, Pharma, Auto & Metals sectors.

However, a key takeaway after observing the intraday activities is to segregate the impact on stocks from (i) fundamental and (ii) sentimental perspectives.

Advertisement

In anticipation of a situation such as the Brexit when global volatility spikes and risk aversion in the market goes up, negative impact on equities can be expected. But if one keeps track of individual stock fundamentals closely, there are some great investment opportunities there for the taking.

As can be seen from the Figure 1, all the stocks initially fell once the news of the Brexit started coming in. However there are some stocks that recovered during the mid-day and closed in the positive, while others closed 5-8% below the opening stock price. A couple of quick comparisons to illustrate why this happened:

1. Mahindra & Mahindra versus Tata Motors- Tata Motors has significant exposure to the European markets with both customers and production facilities located there, especially that of its Jaguar Land Rover business, which it acquired in 2008. On the other hand M&M’s export markets are majorly based in Africa and Asia. As can be seen in the graph while Tata Motors fell and closed in the negative, M&M recovered quickly and closed in the positive.

2. Aurobindo Pharma versus Dr.Reddys- While Aurobindo Pharma has ~28% revenue exposure to the EU markets, Dr.Reddy’s exposure is ~10-12%. While Aurobindo Pharma fell by ~3%, Dr.Reddy’s closed in the positive. Another key reason why such a negative impact could have been felt is that investors often put their money in a market fund (example- Nifty Auto) comprising a portfolio of companies (instead of individual stocks). When global volatility spikes, FII’s begin selling part of their investments in favor of safer investment options. Thus the stocks end up taking a beating.

What happens now?

Advertisement

This referendum doesn’t mean that Britain will exit the Euro immediately. From a legal point of view, Article 50 sets the clock ticking from the moment that the UK notifies the Council of its intention to leave. If an agreement is not reached and if there is no unanimous decision to extend negotiation between UK and EU, all existing EU treaties may cease to apply after 2 years.Regulatory Aspect

In order to contain the risk, we expect BoE to ease rates, though its not clear cut given the fact that as growth slows and unemployment rises, fall in sterling will lift inflation. The BoE has stepped in to provide $345bn liquidity in financial system. The ECB is also expected to open up so-called swap lines with BOE, allowing euros and sterling to be exchanged and effectively make funding in both currencies available to European banks. However extending its QE, which has already saturated markets with $1.1 trillion might be contested by some members, given that it is gradually running out of bonds and securities to buy.

If peripheral financial market pressure is intense enough to threaten the integrity of the region, it could alternatively introduce a new instrument to limit contagion. This could involve country-specific bond market intervention (like the OMT). Regarding potential bank funding pressure, banks already have access to unlimited liquidity in the weekly and three-monthly operations. If needed, the ECB could adjust the timing of these operations. Click Here To Know More.

(All the above views are expressed by member of the finance club of IIM Bangalore – Madhur Bajpai, Spriha Saggar, Madhav Marda and Dinkar Mohta)