Section 80C of the Income Tax of India allows a deduction of certain investments and expenditures up to a maximum of Rs 1,50,000 from the gross total income of an individual in a given financial year. So, if your total investment is say Rs 2,50,000 in a financial year, you can claim tax deduction up to Rs 1,50,000 under Section 80C.

Section 80C of the Income Tax of India allows a deduction of certain investments and expenditures up to a maximum of Rs 1,50,000 from the gross total income of an individual in a given financial year. So, if your total investment is say Rs 2,50,000 in a financial year, you can claim tax deduction up to Rs 1,50,000 under Section 80C.This deduction is provided by the government to encourage household savings. The benefit of Section 80C tax deduction is applicable to individuals (service, profession and business) and Hindu Undivided Family (HUF).

| Tax Savings Under Section 80C | |

| Taxable Income | Tax Saving Up to |

| 2,50,000 – 5,00,000 | 15,450 |

| 5,00,001- 10,00,000 | 30,900 |

| Above 10,00,000 | 46,350 |

(Source)

Here are the top tax saving instruments below:

Personal Provident Fund (PPF)

PPF is considered one of the safest tax saving instruments for those who have a conservative risk appetite. The interest rate is linked to the Government of India bond, and hence fluctuates every year. Presently, PPF offers an annual interest of 8.70% compounded annually. Any individual can open a PPF account in any nationalized bank, notified private sector bank or post office for a period of 15 years. Minimum of Rs 500 to a maximum of Rs 1,50,000 can be deposited yearly. Loan can also be availed against PPF after the 3rd year, excluding the year of deposit. Interest earned on PPF during the financial year is also tax free. You can partially withdraw money from the sixth year of the date of opening the account.National Saving Certificates (NSC)

NSC is again a safe investment instrument as the interest is linked to the government bond yield. NSC can be purchased at any post office for a period of 5 years or 10 years. Minimum amount of Rs 500 can be invested in NSC to earn an annual interest of 8.5% and 8.75%, if purchased for 5 years and 10 years respectively. Interest on NSC is taxable, but since the interest in reinvested in NSC, it’s eligible for deduction under section 80C. There are penalty charges if you withdraw funds before the expiry of the duration of the certificate. However, you can avail loans against NSC.

Tax Saving Fixed Deposits

One of the most popular investment options among conservative investors in the lowest tax bracket is the tax saving fixed deposits. It is similar to regular fixed deposits with an exception. There is a lock in period of 5 years on tax saving FDs. It can be opened with any scheduled bank. There is no premature exit option, but loan can be availed against these FDs. The interest earned on these deposits is taxable as regular income of the individual.

National Pension Plans (NPS)

NPS is a government backed investment plan managed by Pension Fund Regulatory Development Authority, which aims to provide post-retirement income to all Indian citizens. NPS can be availed by employees of government, private institution, organized and unorganized sector. The contributory amount is invested in the markets. At the time of retirement, investors get a lump sum amount depending on the performance of the fund. While NPS contribution has tax benefits under Section 80C, the annuity amount is taxable.

Life Insurance Plans

The premium paid for the life insurance plans is eligible for deduction under Section 80C. Life insurance plans provide a security to the family members of the insured person. It makes sure that they have a handsome amount of money to lead a decent life in case of death of the insured person. One can have more than one insurance policy and the aggregate premium paid on all the policies paid during the financial year, including premium paid on policies taken for spouse and children (dependent or not) is eligible for deduction. The maturity amount is also tax free.

Home Loans

The tax saving on buying a property is available on two components – principal and interest amount. While Section 80C gives a deduction on repayment of principal, Section 24 gives a deduction on the interest. The first time buyers can claim an additional deduction of Rs 1,00,000.

Equity Linked Saving Scheme (ELSS)

ELSS is the kind of mutual fund that are specially designed for the purpose of tax saving. These funds have a lock in period of 3 years, which is least in comparison to all other investment options eligible for 80C. These funds are suitable for the investors with high risk tolerance to market volatility. These funds beat inflation and provide higher returns in the long term, but there is no premature withdrawal option until you pay an exit load.

Unit Linked Insurance Plans (ULIPs)

ULIPs are a category of goal-based financial solutions that combine the safety of insurance protection with strong wealth creation opportunities. A ULIP can be referred to a hybrid insurance plan that combines the benefit of insurance as well as the investment. In case of ULIPs, the premium is divided into two parts – one part goes towards life cover and other is invested in market-linked funds of your choice. For taxation purposes, unit linked insurance plans are considered as life insurance policies. At the time of investment, there is a deduction of tax that is available on premium paid on life insurance policies under Section 80C. Even the maturity and death benefit amount is tax free under Section 10 (10D).

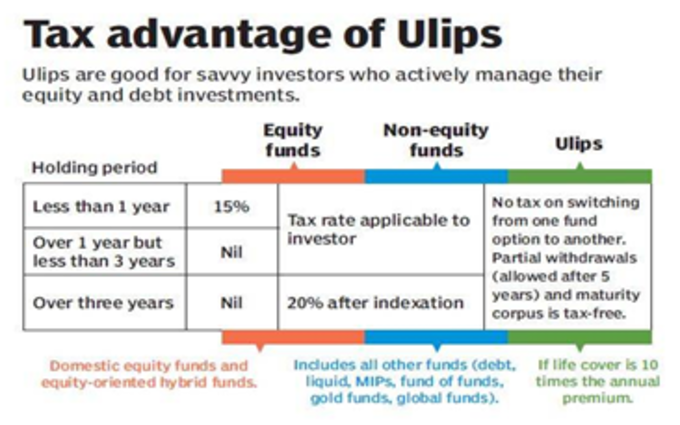

(Source)

ULIPs tend to give higher returns in comparison to all the fixed income investments For companies like ICICI Prudential, close to 96% of their ULIP funds have outperformed respective benchmarks since inception, across debt, equity and balanced funds. ULIPs also has following features.

· An investor has an option of partial withdrawals of up to 20% the fund value every year from the 6th year onwards.

· An investor has an option to make unlimited fund switches based on market fluctuations or investment goals. He has a control over his investments.

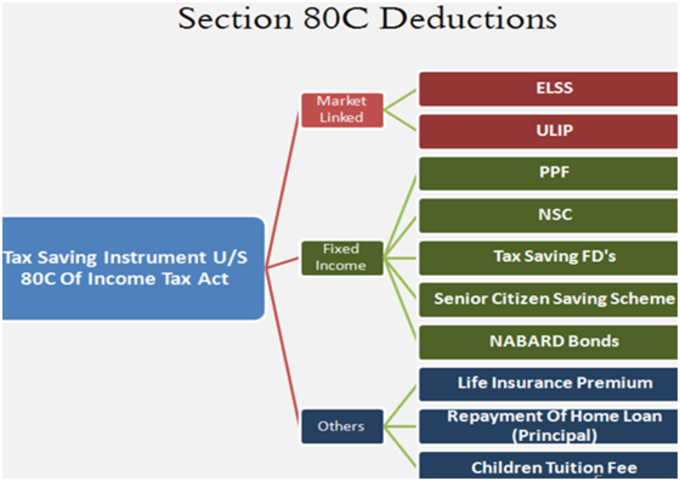

A Snapshot Summary of Section 80C Investment Options

(Source)

Planning of investments for claiming deductions under Section 80C provides gives investors two opportunities - the investor can save tax and the invested money gives returns in future. Based on your financial goals and the features of the above mentioned plans, take an informed decision regarding where you want to invest under Section 80C.

(This article is written by Utkarsh Sahu. He writes for various tech mags and admires technology with paradigm-shifting attributes.)