When thinking of safe savings, most of us always home in on fixed deposits (

Recently, some Indian banks reduced the interest rates on deposits by 0.25%–0.75%, which has made corporate FDs even more lucrative.

What exactly are Corporate FDs?

Corporate FDs, or non-convertible debentures (NCDs), are similar to bank FDs except that they are offered by corporates and not financial institutions or banks. Corporate FDs are, basically, fundraising exercises through which a corporation raises

What’s good about Corporate FDs

The first question on your mind must be: what makes corporate FDs better than regular FDs? And the answer to the same lies in the points below.

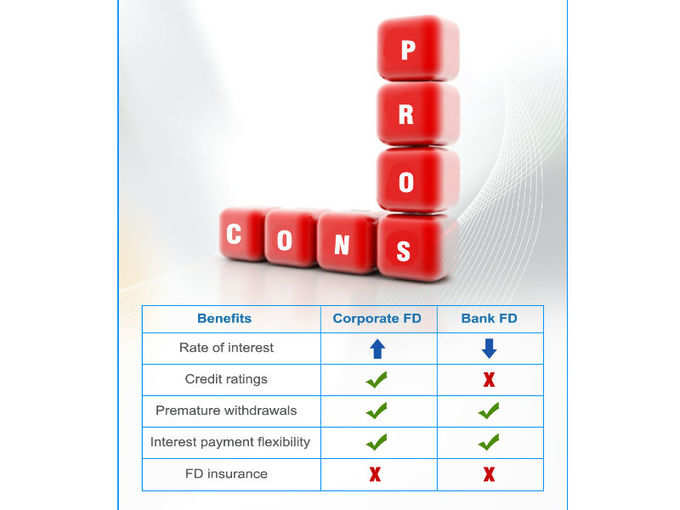

· Rate of interest: Corporate FDs offer higher interest rates than those of a bank, in the range 9%–13%. Some companies offer even higher interest rates to senior citizens.

· Credit ratings: Corporate FDs are rated by independent rating agencies, such as CRISIL, ICRA and CARE, which assess the credit worthiness of the issuing companies. On the other hand, credit ratings are not applicable in the case of bank FDs.

· Interest payments: Investors can choose the frequency of interest payments: monthly, quarterly, half-yearly, annually, or on a cumulative basis. This option offers investors with an additional source of income.

Not all is hunky dory about Corporate FDs

Before you take a plunge in Corporate FDs market, you should measure its pros against the below-mentioned cons.

· FD term: Banks offer multiple term options for investing, starting from 30 days. On the other hand, the typical time frame of a corporate FD ranges from 1 year to 8 years.

· Withdrawals: Bank FDs are easy to withdraw, whereas withdrawing from a corporate FD can take up to a few weeks.

· FD

· Risk Quotient: Corporate FDs come with higher risk as they are unsecured. If a company defaults, the investor stands to lose significant amount of the invested money. To minimize risk, it is advisable to invest in companies with high credit ratings.

Make a note of, when investing …

Before investing in a corporate FD, one of the good initial filters is checking the company’s

Go for the Corporate FD if you:

- are comfortable with lower or no liquidity

- have seen the credit ratings and are comfortable with the sector and the brand (company)

- are seeking returns higher than bank FDs

Table 1: Pros and Cons

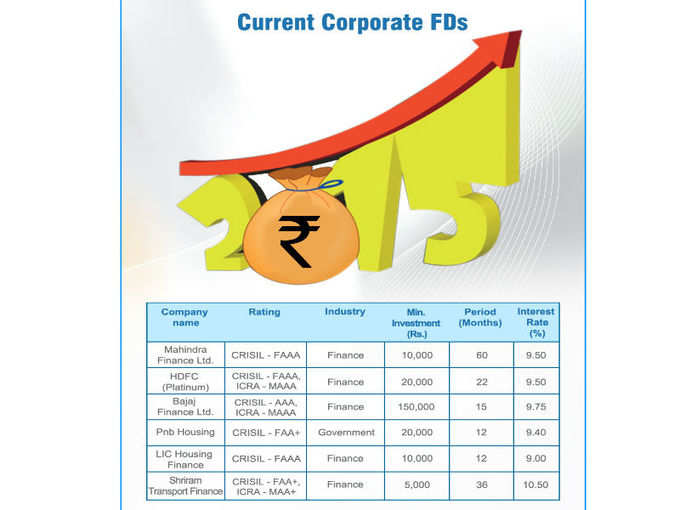

Table 2: Some of the current corporate FDs

Image: Indiatimes

(About the author: This article has been written by Naveen Kukreja, Director, Paisabazaar.com)