The 2016 global economy explained in 7 charts

Emerging market corporate debt has rocketed in the past few years and is risky bet in 2016.

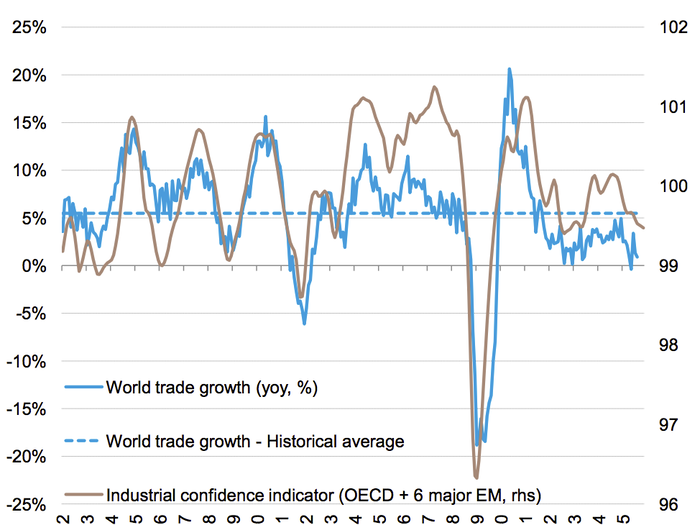

International trade will continue its decline.

"Global trade growth has been anchored below its historical average since the Great Recession, offering further evidence of tepid world economic recovery. Decreasing global demand, especially due to slowing emerging markets, weighs on the outlook for world trade."

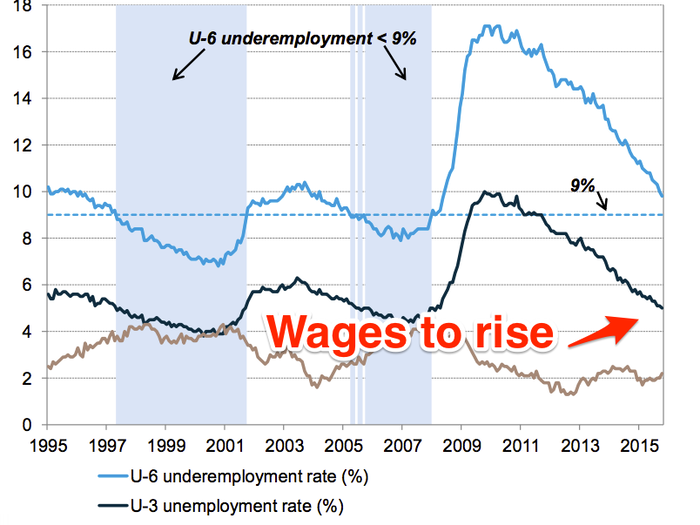

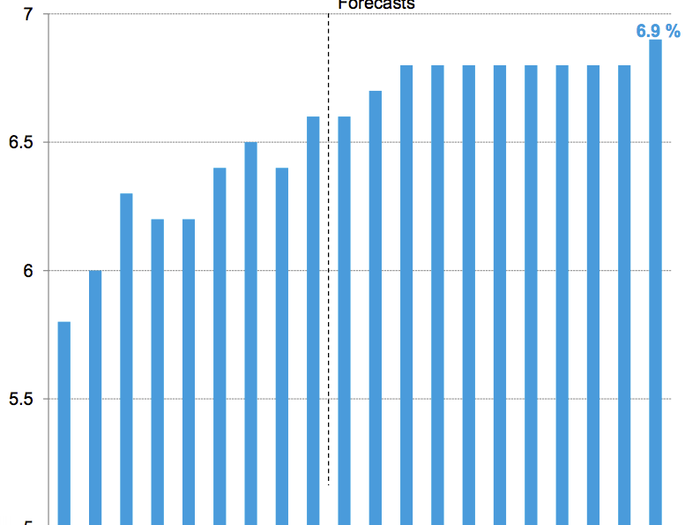

US wages will rise, fuelling consumer spending.

"Although salary growth has remained modest so far, continued labour market improvement should fuel wage inflation eventually. On the other hand, the strong USD will continue to cap headline inflation."

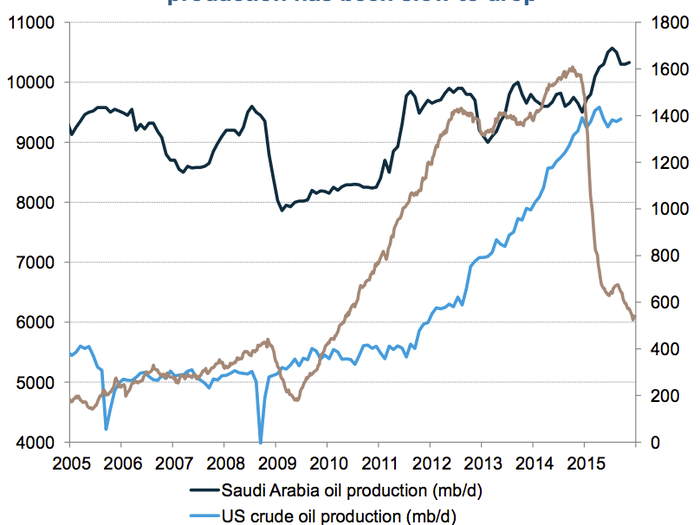

Oil will stay cheap, with Saudi Arabia showing no sign of turning off the taps.

"Saudi Arabia is still pumping at full speed and last summer’s nuclear deal is paving the way for Iran to return to the oil export market. In the US, ongoing efficiency gains have allowed non-conventional oil producers to slash production costs by 20%. In our view, oil prices should remain stuck at low levels – around the USD 50 mark – and any upside is likely to be short-lived."

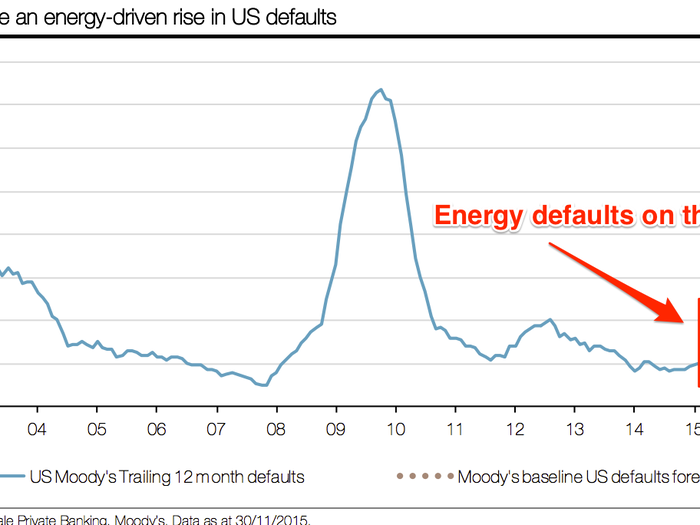

As a result, beware of US energy companies defaulting on their debt.

"Spreads have widened again since mid-2015 and high yield now stands at levels close to those reached in 2000 and 2008 when the US economy went into recession, causing a spike in default rates.

"Sure, we do not expect such a scenario to repeat in 2016 and current valuations offer some value in this respect. However, with the credit cycle already well advanced and moving further ahead next year, the asset class will need to be traded with increasing caution."

Spending on infrastructure will rise, benefiting companies that specialise in big transport and construction projects.

"Infrastructure spending in Asia-Pacific is expected to soar to $5.3 trillion per annum by 2025, accounting for nearly 60% of the global total over the next 10 years. China and India, where urbanisation is in full swing, should dominate the picture."

The Japanese stock market should rise as loose monetary policy and corporate governance reforms take hold.

"On the valuation side, Japan is one of the cheapest developed markets, trading at 14.2x the earnings expected for the next fiscal year, a 16% discount to the 10-year average."

Popular Right Now

Popular Keywords

Advertisement