Investment income is money earned by your financial assets or accounts, and understanding how it works can help maximize your profits

- Investment income, money earned by financial assets or financial accounts, comes in three basic forms: interest, dividends, and capital gains.

- Bonds generate interest; stocks generate dividends; and capital gains (profits) can come from any investment.

- Depending on type, investment income is taxed at regular income tax rates; at special, lower rates; or not at all.

All investing is ultimately about income — making money. Of course, depending on your investment strategy, sometimes the money comes in later (if you're investing for appreciation) and sometimes sooner (if you're aiming for immediate funds).

Whatever your approach — whether you try to time the markets for a quick hit or take more of a long-term, buy-and-hold view — it's important to understand the different types of investment income, and how they are taxed.

What is investment income?

Investment income, also known as portfolio income, is derived from money you've put into financial assets: stocks, bonds, and other securities. It also applies to money generated by a brokerage, bank, or credit union account.

Investment income can take several forms. But it generally falls into one of these categories:

- Interest

- Dividends

- Capital gains

Generally speaking, interest is paid by debt securities, like bonds, and accounts at a financial institution: savings account, money market account, etc. Dividends are paid by stocks. And any investment can generate a capital gain — which happens if you sell it for more than you paid for it. Profit, in other words.

Some investments can provide more than one type of investment income. For example, say you bought IBM stock. If your shares pay dividends, that would be considered one type of investment income. If you later sell the shares at a profit, the difference between the sales price and your basis (i.e., what you paid for the shares) is a capital gain — another type of investment income.

The key to identifying which investment option is better than others lies in identifying which investments offer greater income potential. And that depends to some degree on how they're taxed — how much of the money you actually get to keep.

Interest basics

Savings, checking, and other financial accounts all earn interest. Among investments, interest comes from debt securities — certificates of deposit (CD) and bonds.

When you buy a bond, you're essentially loaning money to the issuer. In exchange, you earn a predetermined rate of interest over a set period. It's usually paid annually or semi-annually.

The interest income earned from a bond (or a bond fund) may be taxable or tax-free; it depends on who the bond issuer is.

- Interest from municipal bonds – those issued by state and local governments – is generally not subject to federal or local income taxes (if you live in that state). US Treasury bonds are not subject to state taxes.

- Interest earned on other bonds, like corporate bonds, is taxed at the federal and state level at ordinary income tax rates – the same rate paid on income from employment. Whatever your income tax bracket, that's the rate you pay on taxable bond interest.

Dividend basics

Investing in stocks or stock mutual funds and exchange-traded funds (ETFs) can generate dividend income. When you buy stock in a company, you essentially are buying an ownership stake in it. Some companies distribute part of their profits to investors in the form of dividends.

Companies pay dividends based on the number of shares of stock you own. For example, if you own 100 shares of IBM and IBM pays $3 per share in dividends annually, you will earn $300 in dividend income. Dividends are usually paid quarterly.

Often people reinvest their dividends back into the company, buying more stock. But those dividends are still taxable.

How your dividend income is taxed depends on whether the dividends are "ordinary" or "qualified." Ordinary dividends are taxed at your ordinary income tax rates. Qualified dividends are taxed at lower capital gains rates.

To be classified as a qualified dividend:

- The dividend must be paid by either a US company, a qualified foreign corporation, or the shares must trade on an American stock exchange

- You must have owned the stock for more than 60 days (within a certain time frame, based on the dividend record date — when you got on the company's books).

Capital gains basics

Capital gains are profits from selling assets such as stocks, real estate, bonds, and other investments. If you sell the investment at a price higher than your basis — what you paid for it — it's a capital gain. If you sell the asset at a price lower than your basis, it's a capital loss.

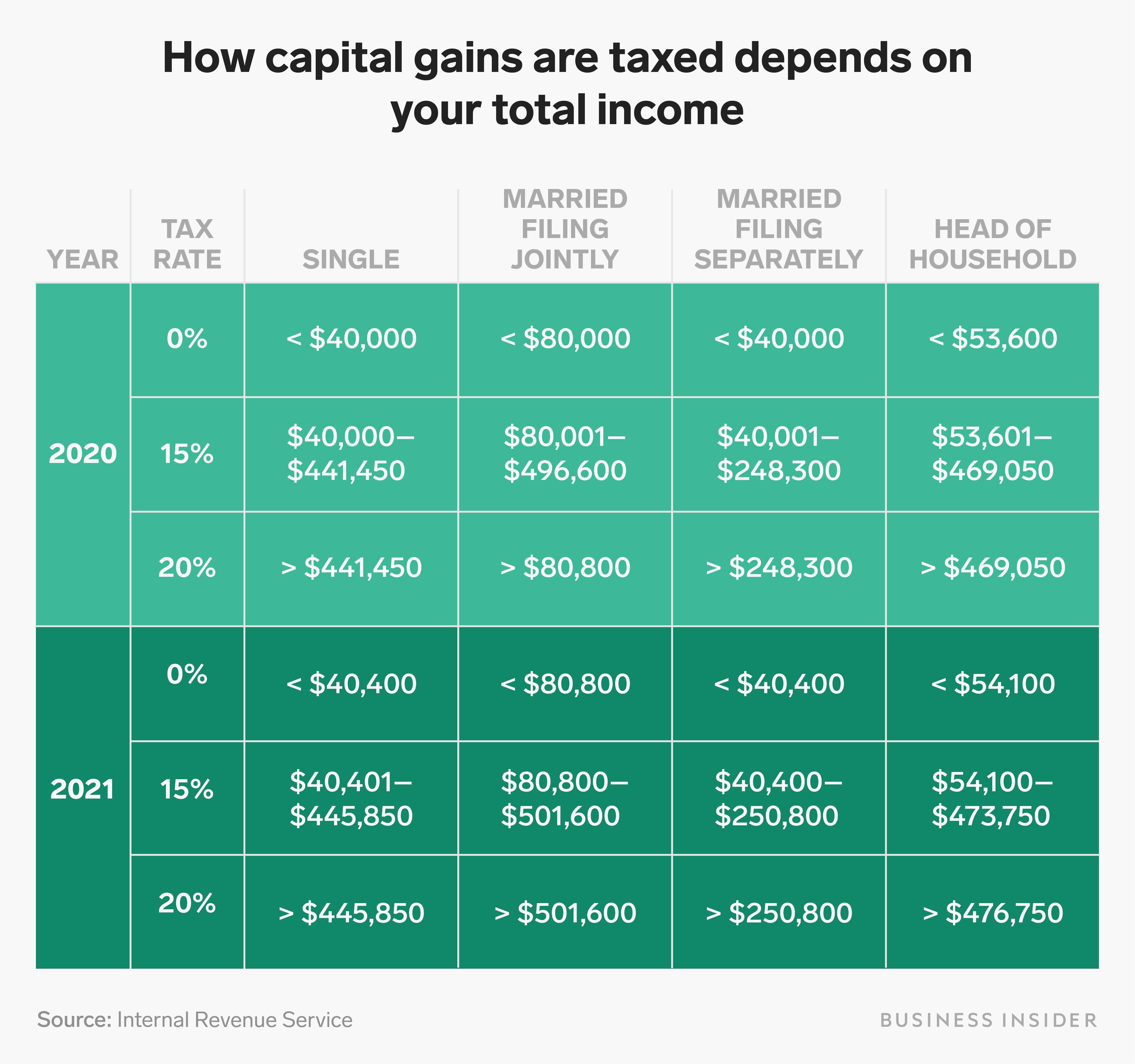

The tax you'll pay on a capital gain depends on whether the gain is short-term or long-term. In most cases, if you owned the investment for more than one year, it's a long-term capital gain or loss. If you held it for one year or less, the profit or loss is short-term.

Short-term capital gains are taxed at your ordinary income tax rates. Long-term capital gains are taxed at a lower rate. The exact amount depends on your total taxable income.

Since the highest ordinary income tax bracket is currently 37%, having capital gains taxed at 15% or 20% can result in some serious tax savings.

Another investment-income option: annuities

Annuities are often considered a source of investment income, though technically they are insurance products.

Annuities represent a contract with an insurance company. When you purchase an annuity, you pay over a lump sum; your money is then invested and converted into periodic payments that can last for life. So it's really your own money being paid back to you, though with a little extra sweetener from its earnings over the years.

Exactly how much, and how your funds are invested, depends on the kind of annuity you purchase. Your money may earn interest, dividends, and capital gains.

However, how the annuity invests your funds has no impact on the taxes you pay. Once you begin receiving annuity payments they're generally taxed as ordinary income.

Investment income vs. passive income

Investment or portfolio income is similar to, but not quite the same as, passive income.

Portfolio income, as the name implies, comes from your assets in your investment portfolio, or other investment/financial accounts.

Passive income comes from a venture in which you are not actively involved. That can be rental income from real estate or royalties earned from a book or other intellectual property. It also includes income from a business in which you aren't actively involved, but have a stake in, such as a limited partnership.

Both are forms of unearned income — that is, funds you didn't personally work for or come directly from your labor or services. That's known as active or earned income, and it's your paycheck from a full-time job or other employment.

The financial takeaway

There's no one-size-fits-all rule for investing or investment income that works for everyone.

Some types of investment income, such as interest from municipal bonds, are more favorable from a tax perspective — but may result in lower returns over the long haul. Investing in individual dividend-paying stocks may have more potential — but also more risk since they're not guaranteed.

Wherever you invest your money, remember taxes aren't the only thing to consider. The best investment income strategy will address your long-term goals and minimize risk by spreading your money across various investment types.