Here's what citizens of 11 advanced nations really think of their economies

Advanced economies.

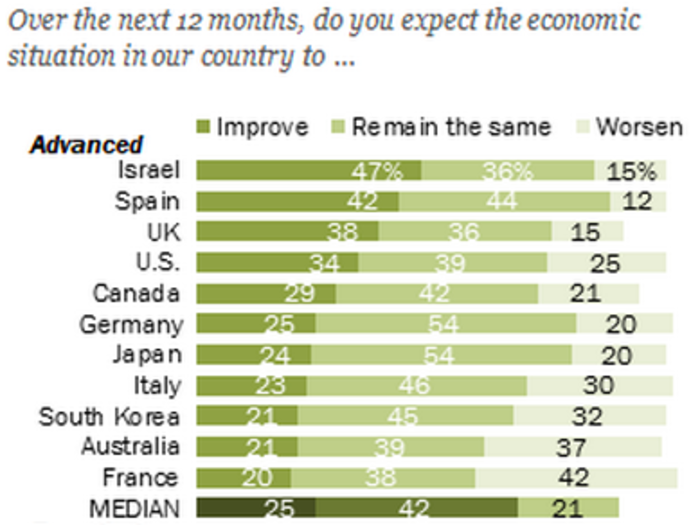

Among the advanced economies, Israelis were the most optimistic about the next 12 months. The French were the least.

Israelis were the most optimistic for the future, with close to half saying they expected the economy to improve.

France is the most pessimistic for the future, with 42% of respondents saying they expected their economy to worsen.

1. Germany

Who said the economy is good: 75% — though that's down 10 percentage points since 2014.

Who said it'll improve over 12 months: 25%, down 1 point since 2014. The majority believe the economy will stay the same.

What's been going on: The country exited the recession early on in 2009 because of a successful $70 billion euro stimulus package, a rebounding manufacturing sector, and exports. The country's GDP is expected to continue to grow because of low global energy prices, low inflation, and a weak euro.

Germany is one of Greece's biggest creditors. Many countries and analysts have advocated for debt relief, but Germany has instead demanded that $70 billion of public Greek funds be put aside in a private trust in Luxembourg and used to pay off debts. (CIA World Factbook)

GDP: $3.8 trillion in 2014 with 1.6% growth (World Bank).

2. Canada

Who said the economy is good: 57%. That is down 10 points from the score in 2013, when it was last polled.

Who said it'll improve over 12 months: 29%, same as 2013 levels.

What's been going on: Canada's Q1 postings for GDP were "atrocious," according to the governor of the Bank of Canada, Stephen Poloz, and shrank for the fifth consecutive month in May.

The country, one of the world's major oil producers, is dealing with falling global oil prices and decelerating demand for raw materials. Mining, manufacturing, and quarrying output also recently fell.

The country is looking toward a general election this year, meaning economic changes could be on the horizon. (CIA World Factbook)

GDP: $1.794 trillion in 2014 with 2.3% growth (World Bank).

3. Australia

Who said the economy is doing well: 55%. Australia has not been polled since 2013, when 67% of respondents described the economy as good.

Who said it'll improve over 12 months: 21%, down 10% since 2013.

What's been going on: The Australian dollar has fallen to its lowest since 2009, and it seems as if investor sentiment in Asia has turned against the country.

The country avoided the worst of the global financial crisis but is having to deal with falling commodity prices.

GDP: $1.44 trillion with 2.7% growth in 2014 (World Bank).

4. UK

Who said the economy is good: 52%. That's up 8 percentage points since 2014.

Who said it'll improve over 12 months: 38%, down 7 points from 2014, but up 16 points since 2013.

What's been going on: Services industries, and in particular banking, insurance, and business, are all key drivers of growth in the British economy.

The country's "austerity programme," initiated in 2010, has been controversial. The economy has rebounded, however, with the Organisation for Economic Co-operation and Development forecasting 2.7% growth in 2015.

GDP: $2.9 trillion in 2014 with 2.6% growth (World Bank).

5. Israel

Who said the economy is good: 49%, down 10 points from the previous year.

Who said it'll improve over 12 months: 47%, up 14 percentage points since 2014.

What's been going on: The Israeli-Palestinian conflict has kept investors wary of the country. Demand for cut diamonds, high-tech equipment, and pharmaceuticals — the country's three main exports — have slowed. GDP growth fell to 2% in 2014.

GDP: $12.7 billion in 2014 with 1.5% decrease (World Bank).

6. US

Who said the economy is good: 40%. That's the same level as 2014.

Who said it'll improve over 12 months: 34%, down 1 percentage point since 2014.

What's been going on: Consumer confidence has been on an upward trend since 2007.

Wage growth hit its record low since 1982, while the national unemployment rate has dropped.

The dollar has strengthened ahead of an expected hike in interest rates this year.

GDP: $17.42 trillion in 2014 with 2.4% increase (World Bank).

7. Japan

Who says the economy is doing well: 37%, up 2 points from 2014, but a dramatic 30 percentage points higher than 2012 levels.

Who said it'll improve over 12 months: Optimism is low. Less than a quarter, or 24%, say it will improve, while 54% believe it will stay the same.

What's been going on: President Shinzo Abe's plan for saving the Japanese economy took center stage in 2012, based on stimulus, monetary easing, and structural reform. The plan has been controversial. Many say it contributed to a widening of the wealth gap in Japan.

Japan's domestic consumption has remained subdued low, but exports have risen because of a weaker yen. The IMF has warned the country not to be overly reliant on a yen weakened by quantitative easing.

GDP: $17.42 trillion in 2014 with 2.4% increase (World Bank).

8. Spain

Who said the economy is good: 18%, that's up 10 points since 2014.

Who said it'll improve over 12 months: 42%, up 8 points since 2014, and 19 points since 2013.

What's been going on: The country's GDP contracted 2008 to 2009, and again from 2010 to 2013. The economy improved between May and June, however, showing a 1% growth spurt. That's the best the country has seen since 2007.

The unemployment rate has barely budged, however; it stood at more than 26% in 2013 to 24% in 2014. Youth unemployment was posted as 49.2%.

Spain’s 2015 budget, published in September 2014, rolls back some recently imposed taxes in advance of national elections in November 2015 — which are hotly anticipated.

GDP: $1.404 trillion in 2014 with 1.5% decrease (World Bank).

9. South Korea

Who said the economy is good: 16%, down 17 percentage points since 2014.

Who said it'll improve over 12 months: 21%, down 9 percentage points since 2014, and 19 percentage points since 2013.

What's been going on: The economy experienced slow growth between 2012 and 2014, and analysts have cautioned investors to hold off from investing in the country because of reduced demand for its exports.

The export-reliant country posted its sixth straight month of falling demand in June. The country has had to fight off a MERS epidemic, which has led to reduced tourism and consumption. That prompted the government to announce a $13 billion stimulus package.

GDP: $1.4 trillion in 2014 with 3.3% growth (World Bank).

10. France

Who said the economy is good: 14%, down from 12% in 2014.

Who said it'll improve over 12 months: 20%, down from 17% in 2014.

What's been going on: The country's public debt rose to 95% of its GDP in 2014, and may hit 100% by 2016.

In 2014, President Hollande announced $24 billion in spending cuts, and plans to sell off $6 to $12 billion in state-owned assets.

France's businesses are reporting the best conditions in four years, however.

GDP: $2.83 trillion in 2014 with 0.2% growth (World Bank).

11. Italy

Who said the economy is good: 12%, up from 3% in 2014.

Who said it'll improve over 12 months: 23%, down 2 percentage points from the year prior.

What's been going on: Italy is known to have a sizable underground economy that could account for as much as 17% of its GDP.

The country's youth unemployment hit a record high of 44.2% in June — the second highest in Europe.

Italy's trend growth between 1995 and 2011 was just 1%, while public debt leapt to 132% of the country's GDP by 2014. The country's GDP is nearly 10% below 2007 precrisis levels.

GDP: $2.1 trillion in 2014 with -0.4% growth (World Bank).

Popular Right Now

Popular Keywords

Advertisement