HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

We’re going to start with how conventional thinking has led Apple and other large tech companies into having such bloated balance sheets. We’ll talk about the usual solutions, and why they don't align well with Apple's priorities. Then we're going to walk you step by step through our idea.

In most sectors, companies run with debt, and issue equity currency as needed for growth or acquisitions. Technology companies have operated differently – particularly some of the largest, most successful companies. They have accumulated enormous amounts of cash that sit idle on their balance sheets for years on end.

...Much of Silicon Valley has learned the lesson: If Wall Street can’t be counted on, the key to survival is a rainy day fund that will get you through tough times.

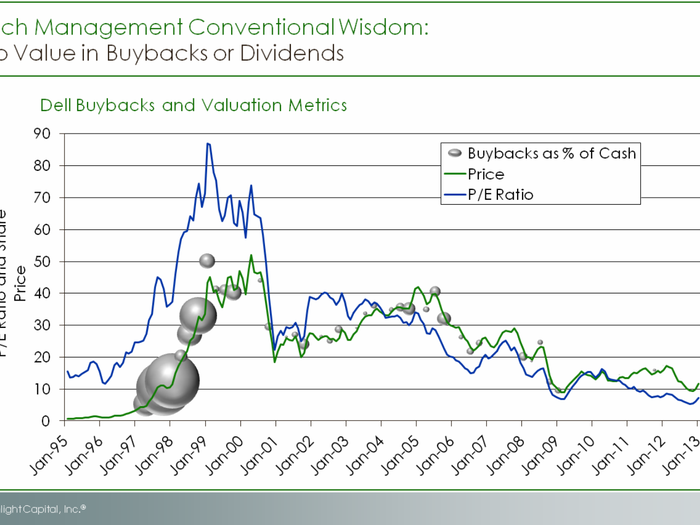

...Back when Dell’s P/E ratio was in the stratosphere, much of its free cash flow went into share repurchases. Conversely, when Dell’s shares have traded at reasonable values, Dell has allowed cash to pile onto its balance sheet.

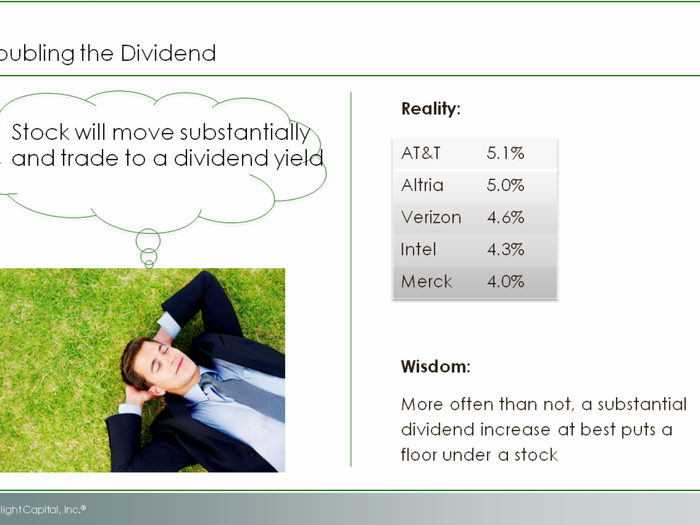

Further, there is a fear that dividends signal poor growth prospects or the end of innovation. Microsoft is apparently the poster child for this argument. Over the last few years Microsoft has shown that one-time dividends, ongoing dividends, and share repurchases aren’t by themselves good enough to drive value in the face of a deteriorating competitive position.

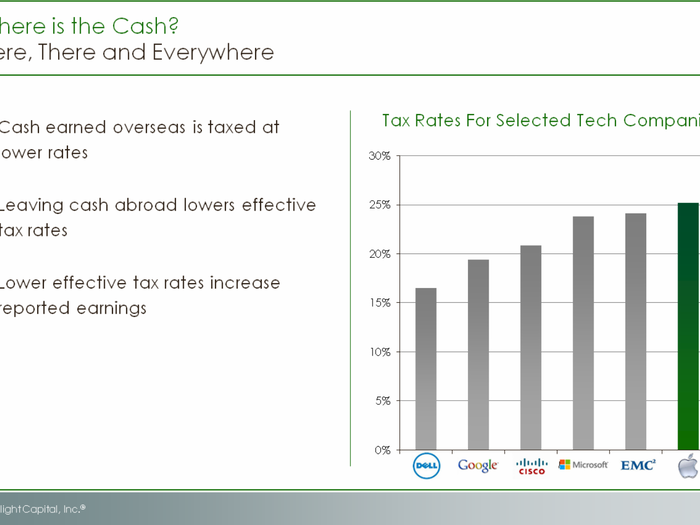

Tech companies use tax strategies available under current laws that maximize ‘offshoring.’ They earn their money in jurisdictions with more favorable tax rates than the U.S. As long as they don’t bring it back to the U.S., they pay only the lower tax rate. I guess what’s earned in Ireland stays in Ireland. The lower rate allows for higher reported earnings.

Occasionally, a U.S. company finds a foreign acquisition where it can deploy some offshore cash, but in general overseas earnings remain overseas. In contrast, companies have complete access to their domestic cash. So this generally gets used, while the foreign cash accumulates....

In some ways, the cash sitting unused year after year is analogous to having an inventory problem. The opportunity cost of trapped foreign cash is very high. The money sits earning only a small amount of interest and generates a return less than inflation. Like decaying inventory, the real value of the cash decays a little bit every day....

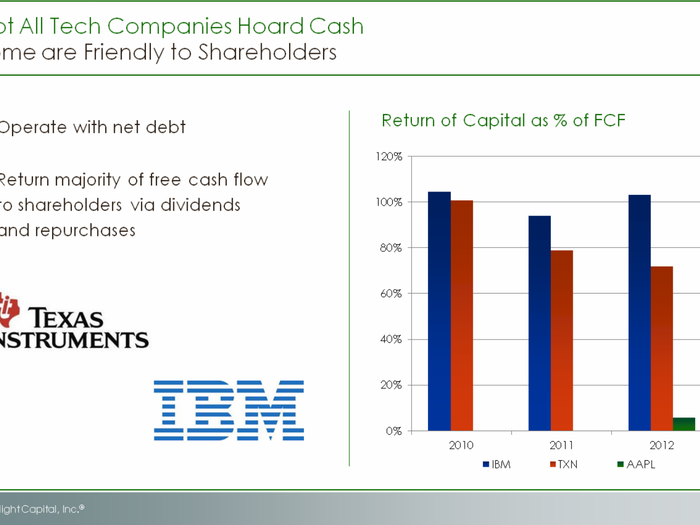

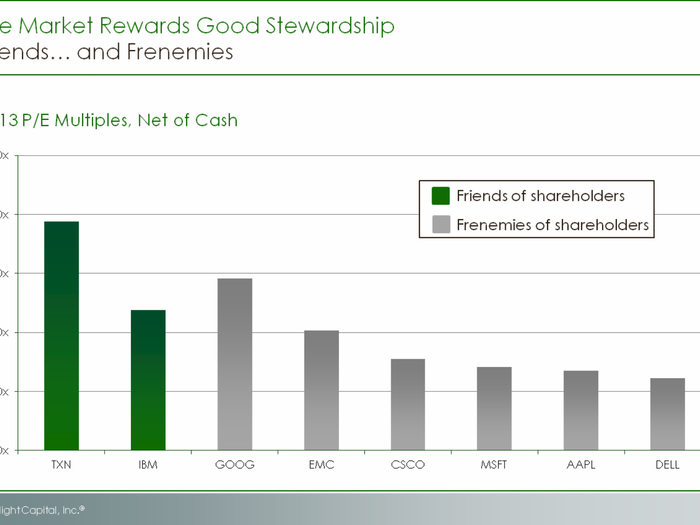

While cash hoarding is prevalent in the tech industry, it isn’t practiced universally. Consider Texas Instruments and IBM. Both have net debt, illustrating that large tech companies can operate with debt. Both return the majority of free cash flow to shareholders via dividends and repurchases.

...IBM and Texas Instruments are considered shareholder friendly and are rewarded for their behavior. You can see that they have better P/E multiples net of cash despite expected earnings growth rates comparable to peers with excessive cash balances....In contrast, cash-rich balance sheets have led to poor P/E multiples. And then we have the story of Dell, which has the lowest P/E of all.

...Last year, we were large shareholders of Dell. We were told that foreign cash couldn’t be repatriated, and that domestic cash needed to be saved for strategic acquisitions, financial flexibility and tough times. We found their attitude toward capital allocation to be so unappealing that we sold the stock. We suspect that we weren’t the only shareholders who were frustrated. The frustration helped depress the stock.

Michael Dell probably didn’t mind the stock falling. For him, it created an opportunity. Now, he wants to take Dell private and voilà! The balance sheet will be fully utilized to finance his purchase of the company. Dell’s cash-rich balance sheet will become a leveraged balance sheet. At least some of the untouchable foreign cash – take a deep breath – is set to be repatriated...

...My first thought is, doesn't letting tens of billions of dollars accumulate on the balance sheet for years on end also reveal an inability to find good use for the cash? My second thought is that the better the business, the more likely it is to generate more cash than it needs. The excess cash reflects the success of prior investments, which were made in the hopes of generating a lot of profits. When a business doesn't require every penny to be reinvested, it doesn’t mean the business can’t grow. It just means that the growth of the business is limited by something other than cash.

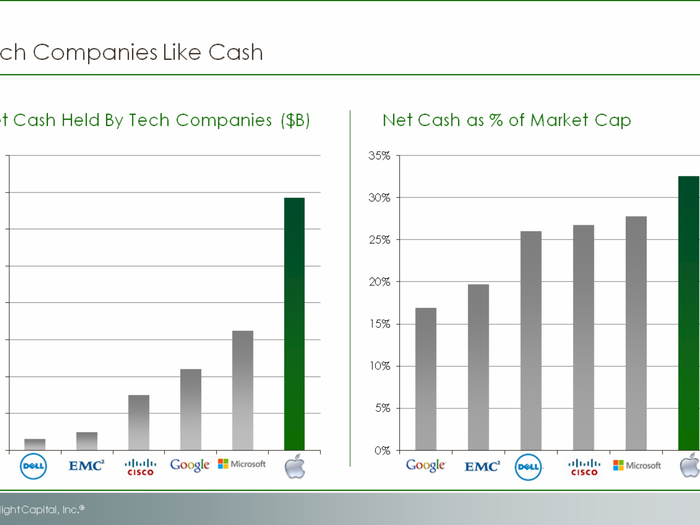

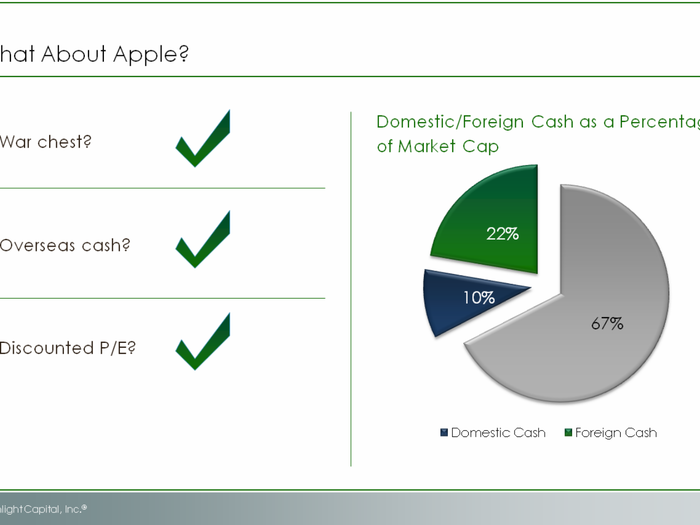

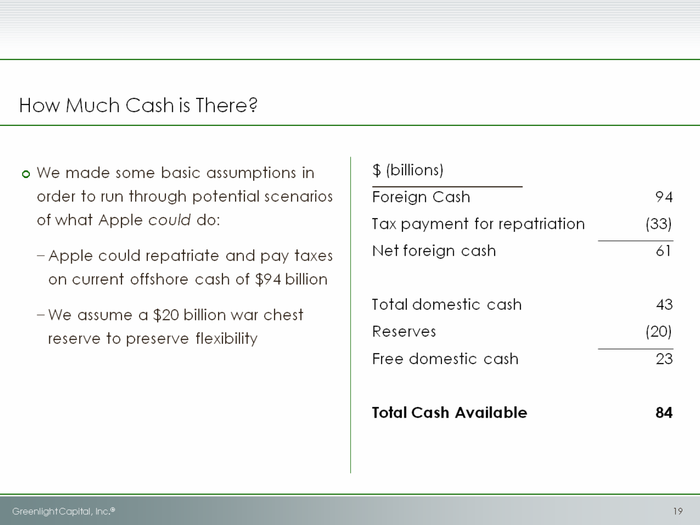

So let's look at Apple: War chest? More like a war vault. Apple has by far the largest cash pile – $137 billion and growing rapidly. Its cash represents nearly a third of its market cap.

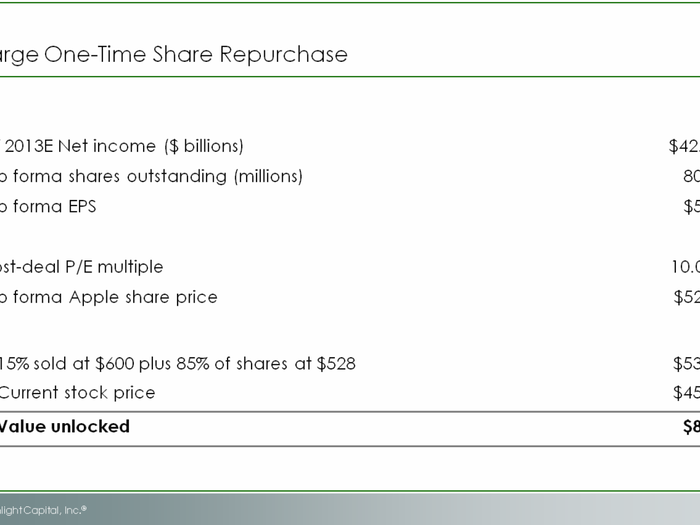

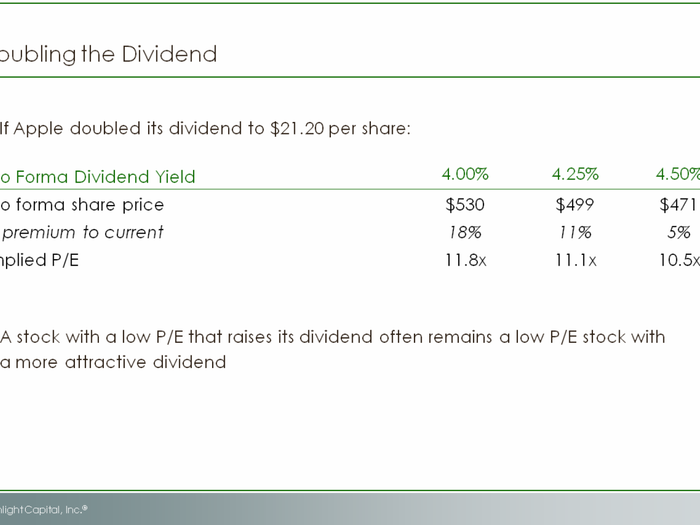

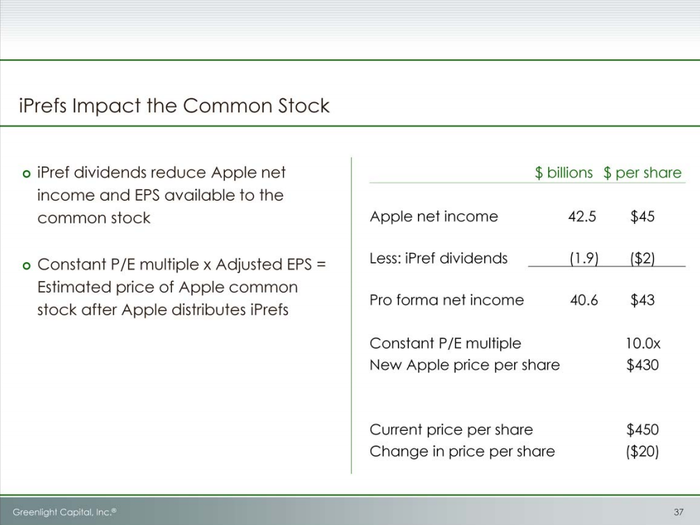

...Apple’s balance sheet is all equity. This means that both the business and the growing cash pile are entirely supported by high cost-equity capital. Assuming a 10% cost of equity, the opportunity cost of the trapped foreign cash is $9.4 billion per year and growing. The opportunity cost of the domestic cash is an additional $4.3 billion. Combined, that is more than $14 per share in EPS. Apple can unlock value by either deploying the cash productively, returning the cash to shareholders, or lowering the cost of its capital that is supporting the cash pile.

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

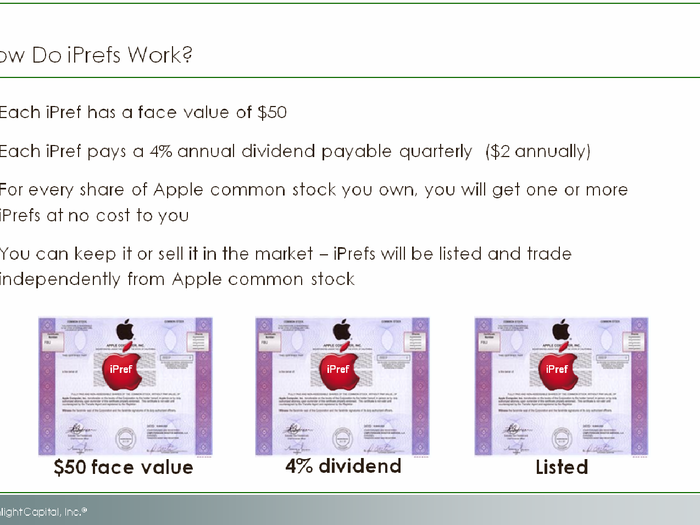

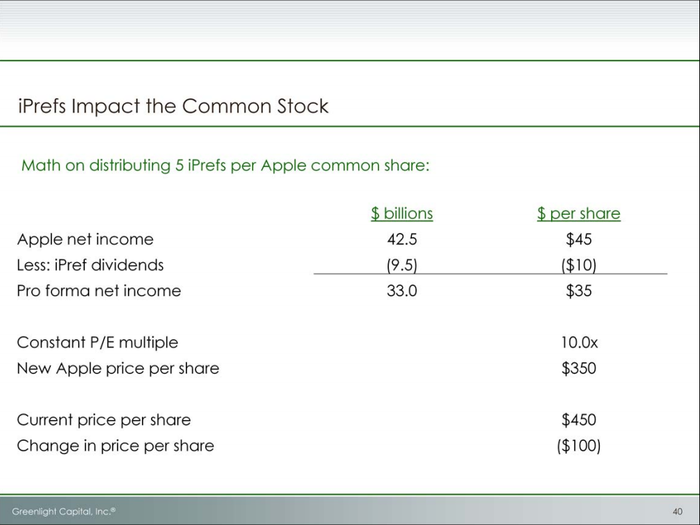

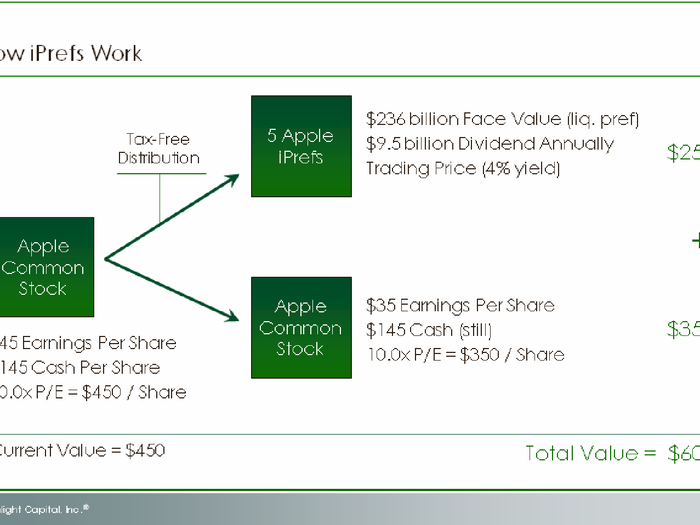

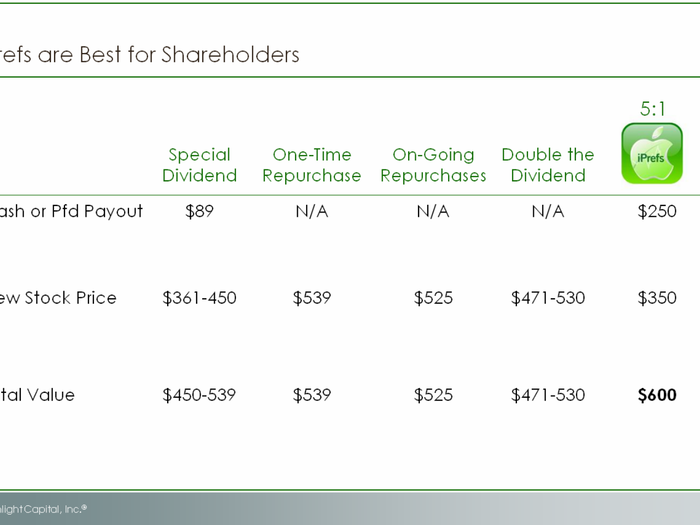

Here is the math on distributing 5 iPrefs per Apple share. It shows the reduction in net income available to the common stock and earnings per share. Distributing 5 iPrefs per Apple common share results in $9.5 billion in additional dividends or $10 per common share. This reduces Apple’s earnings per share from $45 to $35. At a constant P/E multiple of 10.0x, the new Apple price is $350 or $100 less than the current price of $450.

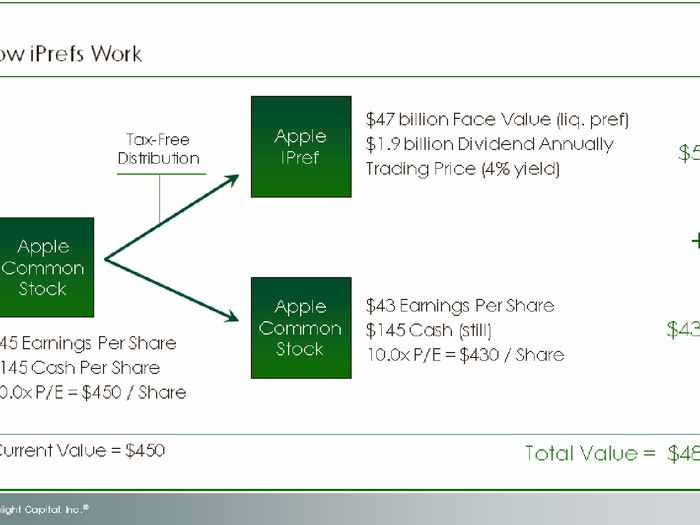

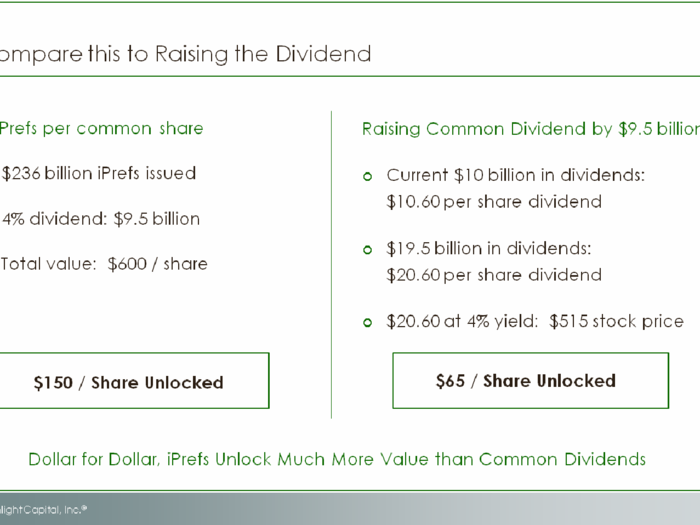

Although the value of the common equity is now lower, if you add the value that the shareholder gets from the iPrefs he receives, the total is a net gain. In the example of a $47 billion iPref issuance, the holder of one share of Apple common stock receives an iPref worth $50, which is added to the new value of the common stock, which is $430. That’s $480 of total value which is $30 higher than the current stock price.

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

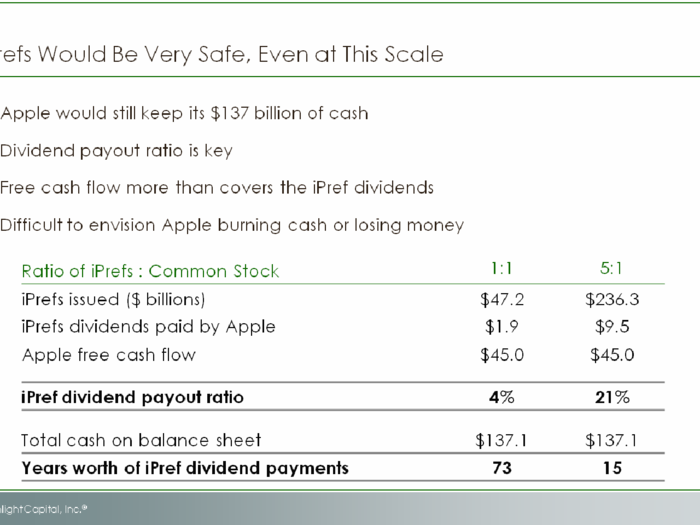

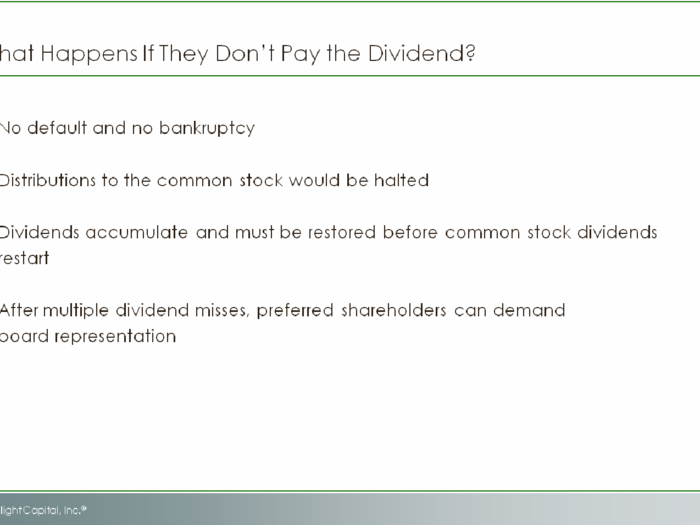

iPrefs are equity, not debt. There is no such thing as a default. The company has the option to cut the dividend, just like it can cut a common dividend, which of course would send a negative message to the market. But aside from that, cutting the dividend just means that there can’t be additional payments or distributions to the common stock until Apple catches up on dividends to the iPrefs. While this scenario is unlikely, it is important to understand that there are no circumstances where issuing iPrefs puts the company at risk of failure.

The important benefit of iPrefs is they don’t interfere with whatever Apple’s business plan is. Because the cash doesn’t go out the door, Apple is free to invest it. Some have speculated whether the money is for a large acquisition or a series of acquisitions. We don’t know what Apple’s plans are, but iPrefs don’t interfere with using the existing cash hoard. If they want to do acquisitions, they can do acquisitions. If Apple wants to keep its cash overseas, it can still do that. If Apple wants to make one-time or recurring dividends or share buybacks, it can still do those things...

While Apple wants to keep its cake, the shareholders get to eat it, too. The iPref program will enable the shareholders to recognize the value in the balance sheet. By splitting the value between incomeoriented investors who will want the safe dividend, and common shareholders that wish to participate in the increased value of the enterprise, the market will reward Apple shareholders with a higher blended multiple of earnings. Even so, to be conservative, we have not assumed any expansion of the P/E multiple on the common equity.

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

HERE IT IS: David Einhorn's Massive Presentation On What Apple Should Do

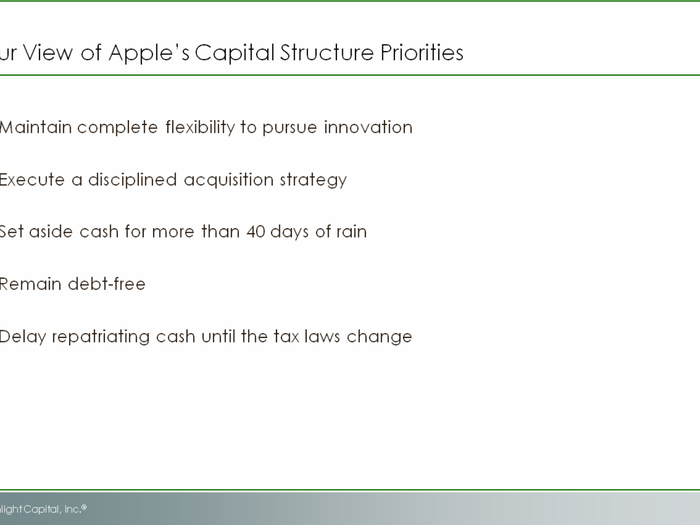

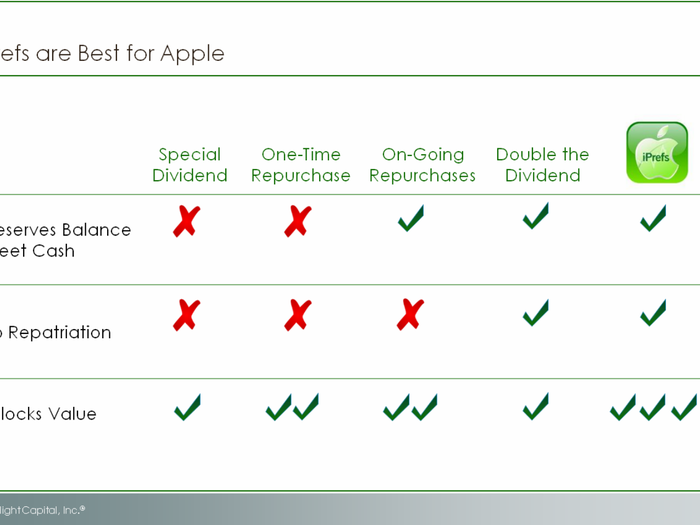

Qualitatively, we think iPrefs are best for Apple. An iPref program uniquely allows Apple to maintain complete flexibility to pursue innovation, execute its disciplined acquisition strategy, set money aside for more than 40 days of rain, remain debt-free, and delay repatriating cash until the tax laws change. They get to do all this, and at the same time, reward shareholders in a big way.

...We know they embrace innovation and can recognize it when they see it, even if it isn’t the kind of innovation people usually think of when they think of Apple. We hope Apple agrees with us when we say that iPrefs are an innovative idea whose time has come.

In the last week, Mr. Cook has called the idea “creative,” and said that Apple would study the proposal carefully. We look forward to meeting with Mr. Cook and his team shortly.

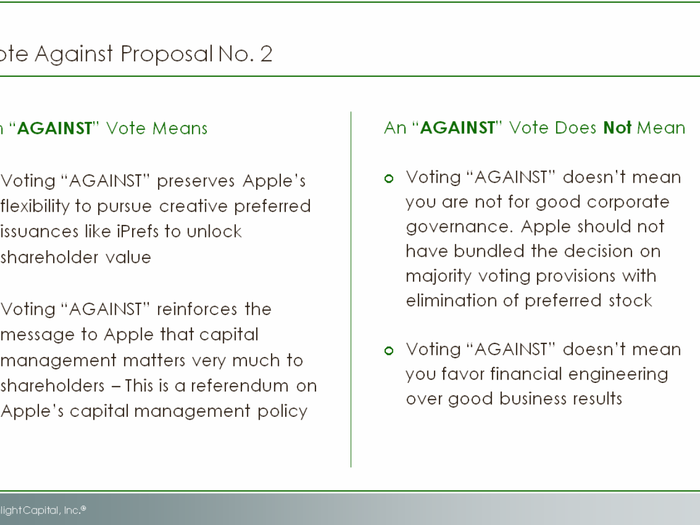

...So, the bottom line is that regardless of how this vote comes out, if Apple decides to go forward with iPrefs, shareholders will have a say. As a result, there is no practical downside to voting AGAINST Proposal 2...

Now let's get to know Einhorn better...

Popular Right Now

Popular Keywords

Advertisement