$50 TRILLION IN DEBT: This is what the 'third wave' of the 2008 financial crisis looks like

Emerging market debt has rocketed since the crisis, while developed market debt has dipped since its 2009-10 high. (Although EM debt is still considerably lower than DM.)

China's debt levels have surged particularly rapidly. As a proportion of GDP, debt accelerated moderately from the turn of the century. In 2007, it was 121% of GDP. Today it's more than twice that — 282%. In the wake of the financial crisis, the government encouraged increased borrowing, which is now particularly visible in the corporate sector's debt.

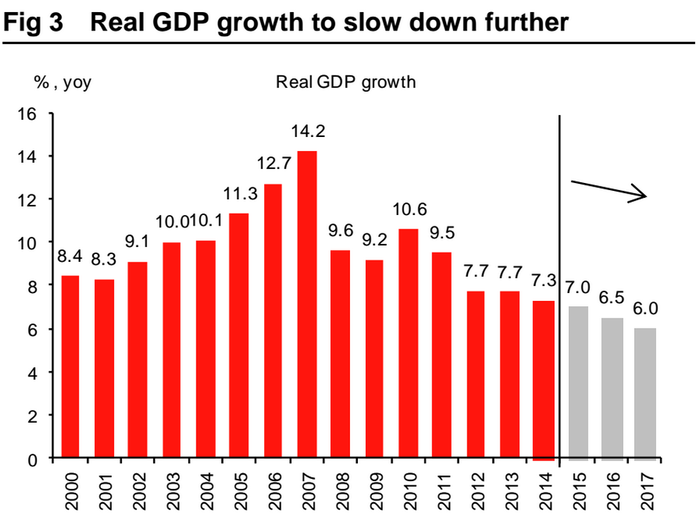

Not only is debt rising, China's natural rates of growth are slowing. This chart shows growth falling to 6% by 2017, which would be a multi-decade low. That's one of the more optimistic forecasts for the next few years. Other economists think the country's transformation will cut growth even further than that.

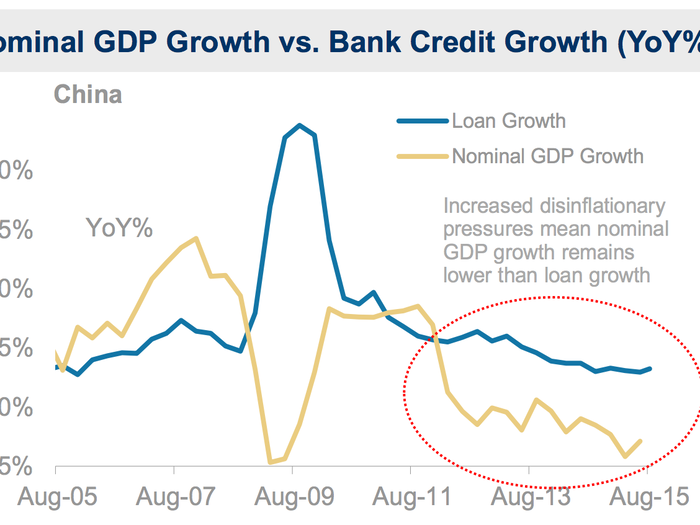

Combined with lower inflation (which reduces nominal growth), it's clear how China's increasing debt is coming about — even though loan growth is slowing, it's not slowing by nearly as much as economic growth has. As long as GDP growth stays below loan growth, then the debt situation in China only gets worse.

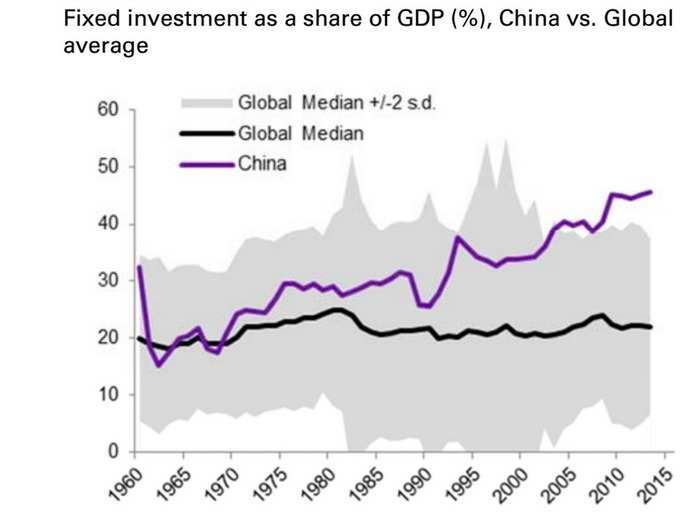

Even among emerging markets, China's investment level has been very high — and with investment comes debt. China has been building like there's no tomorrow, and its investment levels aren't just large by global standards. Among middle-income economies generally, investment runs to about 30% of GDP. In China, by contrast, it's 50%.

The explosion in China's corporate debt is astounding. As a proportion of GDP, the rise since the third quarter of 2008 is more than twice and the next-largest increase in the developing world (Turkey).

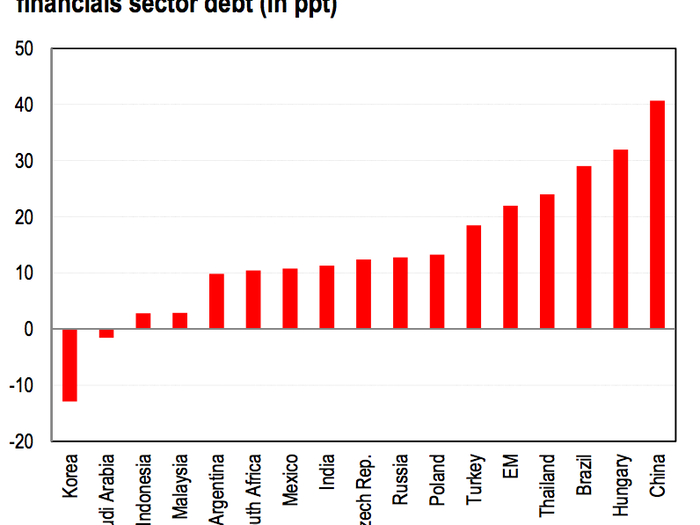

Debt accumulation by financial institutions has been a little bit more reserved, but the country still tops the list for the most borrowing since the middle of 2008.

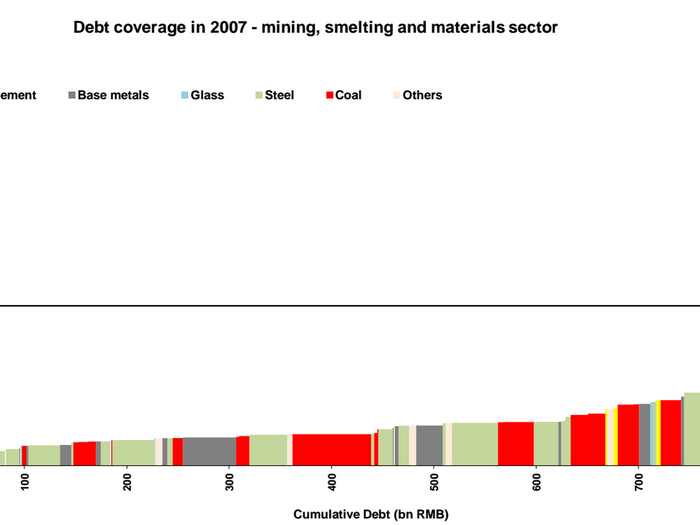

Nowhere is that more visible than in the commodity-reliant sector. On these charts from Macquarie, 100% on the y-axis illustrates the point at which a company's entire profit is overtaken by debt interest payments. Back in 2007, very few companies were in that situation.

Fast-forward to 2014 and the sector is telling a very different and much more worrying story. Not only is the total stock of debt in the sector up by more than 300% in seven years, about half of companies have debt interest payments twice as high as their earnings.

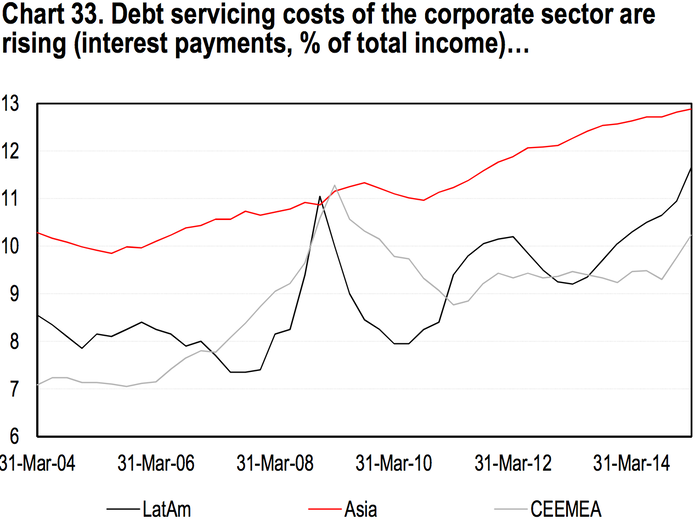

The steep accumulation of debt brings back awkward memories of the Asian crisis. In 1997, south and east Asian developing economies struggled to service their accumulated debts as local currencies plunged in value against the dollar.

The difficulty of servicing that debt in emerging markets has increased this time too, though at a slower pace. For those countries that have a lot of dollar-denominated debts, the strengthening of the US currency (often driven by Fed interest rate hikes) will only make repayment more difficult.

The riskiest part emerging market corporate debt is the proportion that's not denominated in local currencies, particularly the dollar-denominated debt, because the domestic central bank isn't in control. This chart shows the total stock of emerging market bonds, and how it's boomed.

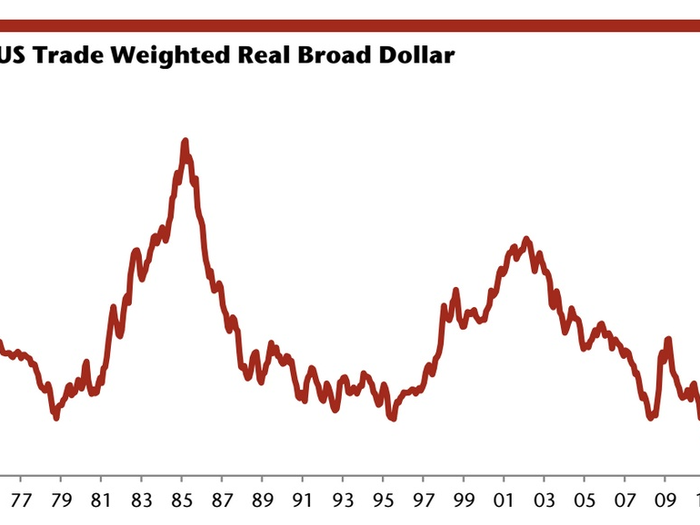

The dollar has appreciated considerably in the last two years, to the highest level in nearly a decade — when the US currency strengthens against others, anyone with an income denominated in an emerging market currency but debts denominated in dollars effectively sees their liabilities increase.

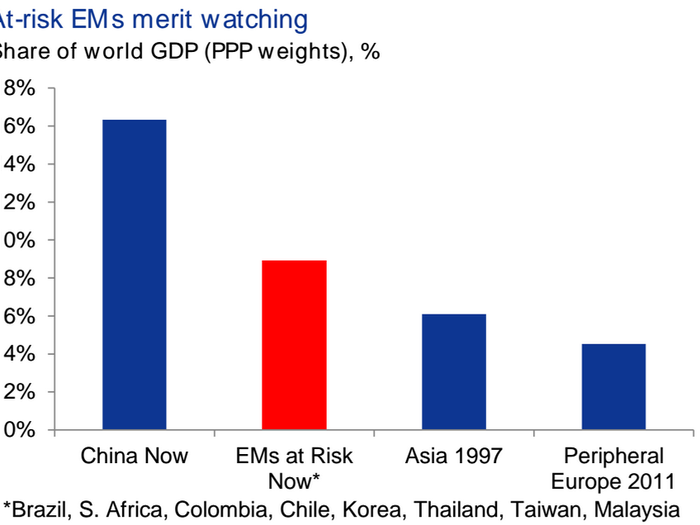

But why does it matter to the world? Most analysts think a 1997-style meltdown is unlikely for emerging markets. But they're now a much larger presence, precisely due to that rapid growth. Developed economies can't simply shrug off their slowdowns.

The lack of a "global consumer" means there is no ravenous demand for emerging market goods, either. Economist Ken Rogoff recently suggested the world is in the later stage of a "debt super cycle," which suppresses? growth everywhere.

According to Goldman, this is the final act of the financial crisis. Either the developing world enters a substantive recovery on the other side, or it goes into a "secular stagnation" period of permanently lower growth, restrained by high debt levels.

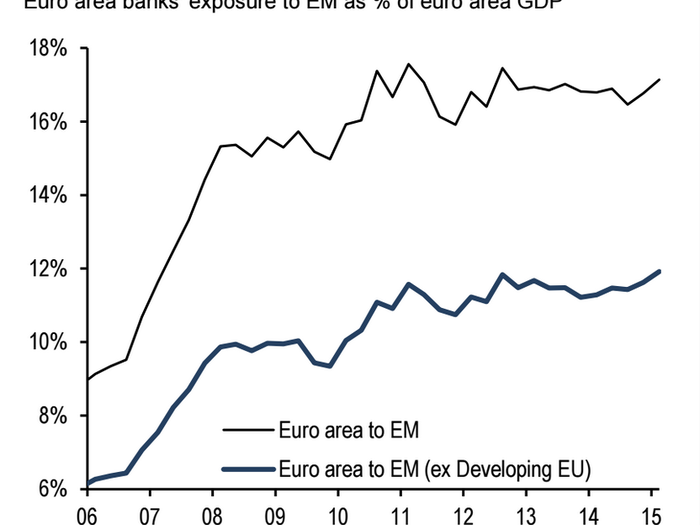

Some economies are more exposed through the trade channel than others. A particularly high portion of German trade is done with the emerging world. But given their bigger place in the world, most developed countries trade more with emerging markets than ever before.

Last year the International Monetary Fund introduced a new word to economy-watchers: "spillbacks". It's commonly understood that growth and conditions in advanced economies affect EM growth — the IMF was trying to draw attention to it working in the other direction.

A paper by economist Hyunju Kang this year suggested that "financial contagion" could be "substantially enlarged" by deeper links between advanced and emerging economies — coupled with increased global debt levels, and it's easy to see how an emerging market slump could put the brakes on growth around the world.

On October 19, China's Sinosteel failed to repay a bond, a sign of financial distress among commodity-focused firms. How the world's largest emerging market handles itself in these uncharted waters will be enormously important to both the developing and advanced world.

Popular Right Now

Popular Keywords

Advertisement