Fast

Fast Globalization may mean macro changes and yet the micro changes may have macro effects. In more recent times, the traditional mithai shops have taken a hit; Indians seem to be showing a departure in taste palates in favour of the more modern, neatly packed chocolate boxes. These sugary delights especially packaged for Diwali are available anywhere, in the price range of USD 1.5 to USD 100 and more, form the affordable to for the affluent.

While

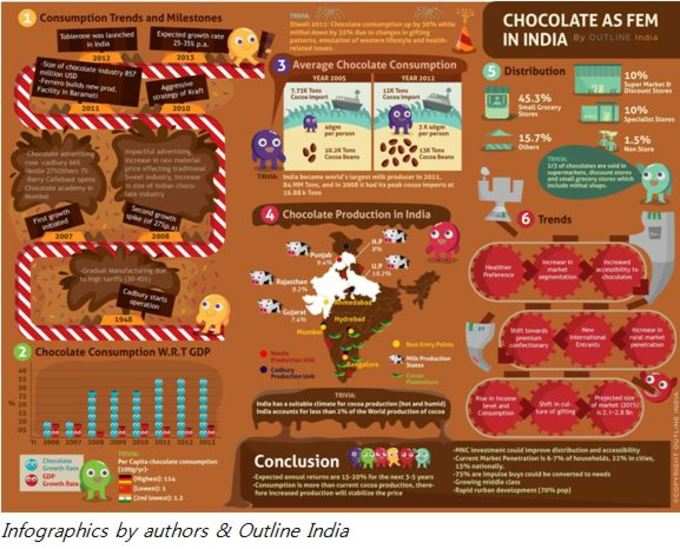

To put things in perspective, the chocolate industry is growing at a rate of nearly 3x that of GDP. Such spiralling high growth rates lead us to believe that the chocolate industry may in fact be a good example of FEM.

Outline India, a research start-up focusing on field data collection within the socio–economic domain, took on this study under their guidance to explore if this was indeed the case, and the result can be summarized in the below infographics.

India’s current chocolate consumption pattern suggests very low per capita levels of around 1.2 owing to few traditional players and high import tariffs on import of chocolates. This however, leaves ample scope in terms of change in domestic production and consumption rates. To bolster this argument, India’s hot and humid climate is conducive to cocoa production, key to the chocolate industry. As of 2011, India is also the largest milk producer in the world. With the middle class growing, average incomes rising and information asymmetry levels going down, consumers are more aware than ever before, about available choices to them. With more cultural exposure and an urge to appear more western in terms of behaviour and at par with the international consumer, levels of chocolate consumptions are rising, especially among urban Indians. Also cited are health reasons that favour chocolates over the more the more traditional Indian sweets. A majority of these savouries, house a higher number of calories and shorter shelf lives. No longer is chocolate considered a ‘luxury item’ or one meant only for ‘special occasions’.

In terms of what may prove to be a dampener? On the supply side, there have been numerous hurdles; the most important being bad connectivity and infrastructure. As a solution, a majority of the chocolate factories sprung up on the outskirts of big city centres, which were also best entry points for producers. A keen effort is being made to improve supply side channels to ease distribution. For instance, breaking away from the traditional supermarkets and discount stores, the big names such as Ferrero Rocher and Mars are trying to integrate into the lives of the upper middle class Indians by becoming available at the more accessible and approachable grocery stores. Local producers like

While the chocolate industry grows at 15% annually, projections put the expected market size at USD 2.8 billion by 2015 and USD 3.2 billion by 2018.

Current market penetration rates are as low as 6 to 7 % at household level and about 22% in cities. This leaves scope for much change.

One of the best known ad campaigns in the industry by Cadbury read, “Khane ke baad kuch mitha ho jaaye” which translates to Grab something sweet after a meal, only this time, the company was pitching a chocolate, breaking into and away from the traditional Indian household mindset which correlates sweet with mithai. The big guns are going the extra mile to suit the Indian consumer;

((Dr. Amit Kapoor is President and CEO of