South Korea is open to cryptocurrencies and making an effort to regulate them, but crypto exchanges still aren't happy

Jul 1, 2021, 16:46 IST

- South Korea doesn’t want to ban cryptocurrencies, but it does want strict regulation in place.

- The clock is ticking for crypto exchanges in the country, with the government setting a September 2021 deadline for them to comply.

- Caught in limbo, players in the crypto industry are reportedly thinking of suing the government to fight back on terms and conditions, which are not in their control.

Advertisement

South Korea’s crypto industry is undergoing one of the biggest shake-ups in history. The past four years have been a tumultuous storm between crypto exchanges and the regulatory authorities. And now, in 2021, the government has finally put its put down. What comes next will either make or break South Korea’s crypto legacy.For those who only turned into the crypto blaze this year, South Koreans were among the major players during the 2017 crypto boom. Even though they account for less than 1% of the world population, they were behind 30% of the crypto trading volume that year, according to estimates by fintech company Cindicator at the time.

However, the boom came with its own terms and conditions — and the impact is playing out till date. And, there’s a lot on the line if these exchanges mess up.

You can’t be anonymous if you want trade crypto in South Korea

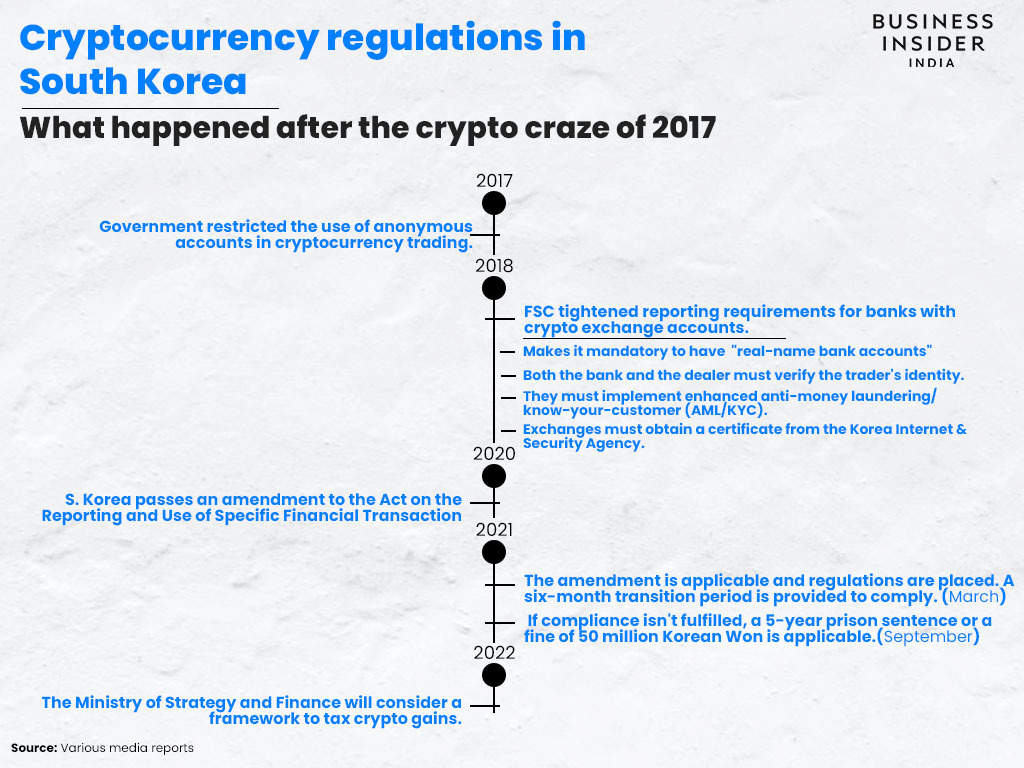

After the crypto boom hit the peninsular nation in 2017, the South Korean government decided to restrict the use of anonymous accounts in cryptocurrency trading. While cryptocurrencies were not regarded as lawful money, exchanges were permitted and governed by a strict regulatory framework. Advertisement

A new law introduced the concept of ‘real-name bank accounts’ which helps establish the unique and verified identity of a trader, indirectly helping keep a tab on money laundering and other unlawful activities.

And, traders could only transact with cryptocurrency dealers that used the same bank, putting the responsibility to verify the customer identities on both the banks and the exchanges.

You can’t just set up a crypto exchange, you need approval from a bunch of authorities

In March 2020, the Act on Reporting and Use of Specific Financial Transaction Information was amended. It extended mandatory anti-money laundering and counter-terrorist financing (AML/CTF/KYC) obligations to all crypto exchanges in the country.

Advertisement

Simply put, the financial regulator has tasked its intelligence team to keep an eye on large trading volumes that could be potential laundering attempts. And, ultimately, crypto exchanges would require a license from the FSC's Financial Intelligence Unit in order to continue with their business.This makes the process of tracking illegitimate activity proactive, rather than reactive. The authorities can keep an eye on suspicious transactions directly and don't need to bureaucratically request data from exchanges after a crime is reported.

The new laws apply to Virtual Asset Service Providers (VASPs), and an entity is called one if it is:

- Selling and purchasing of cryptocurrencies

- Crypto-to-crypto transfers

- Transmitting cryptocurrencies

- Administration or safekeeping of virtual assets

- Custodian

- Initial coin offerings

2021 brings a catch with heavy consequences

Even though these measures aren't new and have been in existence since 2018, the South Korean government has now made them mandatory. The regulations were officially enacted in March 2021 and there's a six-month transition period with a September 2021 deadline. Hence, crypto exchanges are now looking at a sink or swim decision. If they don't comply, they'll either have to shut down or move out of the country in order to keep operating.

Advertisement

And, not abiding by the new law carries a punishment of up to five years in prison or a fine of 50 million Korean won (around $43,000 or ₹32 lakh) — neither of which is an enticing prospect.

For some exchanges, the decision may be out of their hands. Domestic banks hold the key to their customers being able to trade on crypto exchanges, and right now they’re reluctant to open the door fearing the possibility of being involved in money laundering.

The ‘big four’ — UPbit, Bithumb, Coinone, and Korbit — are currently under risk assessment by K Bank, NH Bank and Shinhan Bank. Meanwhile, smaller exchanges and related businesses are caught in limbo.

South Korean crypto exchanges may look at legal recourse

Players in the South Korean crypto industry are considering filing a lawsuit against the government and the financial regulator, alleging the new law is unconstitutional.

Advertisement

According to them, the authorities should be held accountable for cryptocurrency and exchange verification but are conveniently putting all the responsibility on banks. And, since the banks are risk-averse, they prefer giving up on crypto altogether rather than venture into turbulent territory."We are facing an existential crisis. We want to legitimize our business, but banks are reluctant to offer us real-name accounts," Lee Chul-ie, the CEO of cryptocurrency exchange Foblgate, told the FT. The regulation creates a new black and white for these smaller companies, thrusting them forcibly towards the grey.

A report from The Korea Herald also says that crypto exchanges with too many coins could be denied real-name accounts. The report cites risk assessment guidelines that ask commercial lenders to classify exchanges with "a high number and frequency of virtual money transactions" as high risk. The rule is made to discourage the adoption of altcoins that are often used to scam investors or have no inherent backing per se.

Meanwhile, South Korea wants to set up its own centralised cryptocurrency

The Bank of Korea (BoK) — South Korea's central bank — will soon seek bids for a technology partner to launch a pilot program for a ‘digital won’. The pilot will run from August to December and involve multiple simulations involving banks, retailers, deposits, fund transfers, and mobile payments. BoK's research suggests that the new central bank digital currency (CBDC) will be treated on par with fiat currency and not a crypto asset despite being a digital currency. Hence, one will likely be able to exchange digital won for cash.

Advertisement

While the plan is still in its early stages, a trial run is definitive. Being a technological powerhouse, South Korea is leaving no stone unturned in determining the actual value of blockchain and its wider repercussions. It's among the first countries to develop an in-depth framework that factors in practicality with future promises as the world watches with bated breath to see how it will all play out. For a more in-depth discussion, come on over to Business Insider Cryptosphere — a forum where users can deep dive into all things crypto, engage in interesting discussions and stay ahead of the curve.

SEE ALSO:

The world's largest crypto exchange is having a hard time convincing regulators with multiple bans piling up

China's oldest crypto exchange exits cryptocurrency business amid government crackdown on Bitcoin mining

Google, Facebook, and Tesla crypto tokens are launching on crypto exchange FTX