Fintechs are under scrutiny over fraudulent PPP loans and small businesses could suffer. Here are the biggest takeaways from the federal investigation.

Jennifer Ortakales Dawkins

- A federal investigation blames fintechs for rampant Paycheck Protection Program loan fraud.

- The resulting report named fintechs and lenders it said failed to screen for fraudulent claims.

America's fintech darlings became the MVPs of the Paycheck Protection Program by easing the process for troubled small-business owners, but now they're in hot water over suspicions that they facilitated fraud.

The US House Select Subcommittee on the Coronavirus Crisis released a report this month that named Blueacorn, Womply, Bluevine, and Kabbage among fintechs and small-business lenders that failed to prevent fraudulent loans.

Small businesses benefited most from fintechs' participation in the program because easier online applications meant increased access to government funding, especially for underrepresented founders who were largely left out of initial PPP rounds. Now, the report's findings put fintechs under scrutiny and may jeopardize their participation in future government programs.

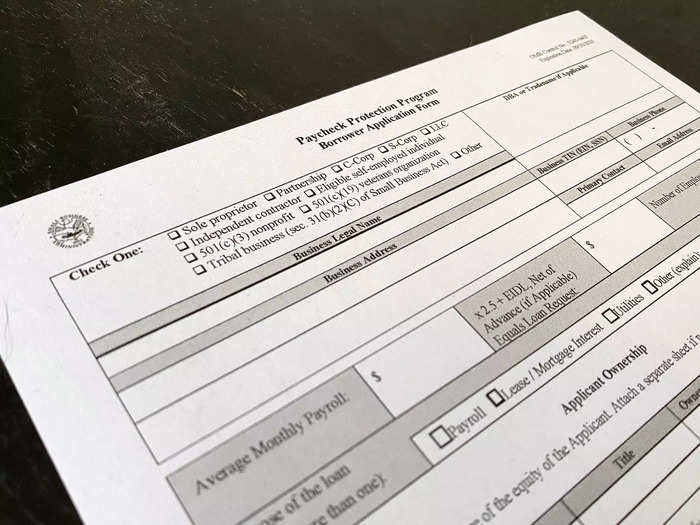

The Paycheck Protection Program was a federal rescue program intended to help the 7.5 million US small businesses at risk of closing permanently in the first year of the COVID-19 pandemic. The Small Business Administration awarded nearly $800 billion in PPP loans to 11.47 million businesses.

Since then, the Justice Department has charged several business owners over accusations that they fraudulently obtained forgivable PPP loans, alleging they never used the funds for eligible purposes, such as employee payrolls or certain business expenses. In two notable examples, one man pleaded guilty to purchasing a Lamborghini with one of the government-funded loans, and the Justice Department charged another man over accusations that he bought an alpaca farm with PPP money.

In a two-year investigation into PPP use, the House subcommittee interviewed witnesses, executives, and former employees and obtained internal company communications. The resulting report places much of the blame on the fintech companies and lending partners, saying they failed to screen for fraudulent claims and "abdicated that responsibility, in many cases recklessly."

Kabbage, Blueacorn, and Womply did not immediately respond to Insider's request for comment.

Here are the biggest takeaways from the federal investigation.

Kabbage, Bluevine, Blueacorn, and Womply are among fintechs accused of facilitating 75% of fraudulent loans

The House subcommittee started its investigation into the companies in May 2021, following news reports that a significant number of fraud cases were connected to loans approved by fintech companies.

Bloomberg reported that fintechs handled only 15% of PPP loans overall but accounted for 75% of the fraudulent PPP loans investigated by the Justice Department. Bluevine, one of the fintechs in this group, processed over $4.5 billion in PPP loans for at least 155,000 businesses, a letter from its CEO says.

Kabbage, which processed over $7 billion in PPP loans to at least 300,000 businesses, accounted for 20% of all suspicious loans, the Miami Herald reported.

As of October, the Justice Department had prosecuted more than 235 defendants in more than 162 criminal cases of pandemic-related fraud, according to an email from the department to the subcommittee referenced in the report.

Banks are also accused of facilitating fraudulent loans

Some of the banks that partnered with fintechs to facilitate PPP loans are being scrutinized. The report found lenders largely relied on their fintech partners to monitor fraud and that the ones that worked with Womply and Blueacorn conducted little oversight of their activities.

An investigation from the Project on Government Oversight found that Cross River Bank and Celtic Bank were involved in 30% of the Justice Department's fraudulent PPP loan prosecutions.

According to a May press release from the House subcommittee, Cross River Bank approved more than 280,000 PPP loans, worth over $6.5 billion, and Celtic Bank funded nearly 100,000 PPP loans, which totaled more than $2.5 billion.

Fintech and bank executives anticipated fraud early on and watched as it grew out of control

According to internal communications obtained by investigators, executives at the fintechs and bank partners anticipated and acknowledged the fraud was happening early on in the PPP rollout. The report said lenders knew it "was not well controlled."

In April 2020, Cross River's chief risk officer said in an email to staff: "There will be fraud rings going after these [PPP] funds." In October 2020, the CEO of Celtic Bank wrote in an email that the high level of fraud was "not surprising" because of the program's guidelines.

In a November 2020 email, a Celtic Bank compliance manager said there was an "uptick in fraudulent and money laundering activities" as a result of the lender's participation in the program.

One exec described taxpayer losses as a 'helluva lot of money,' and companies estimated the sum was between $10 billion and $80 billion

In an August 2020 email, Celtic Bank's president and chief operating officer estimated that fraud losses from PPP loans could have reached "over $10 billion" and described the total loss to taxpayers as well below the expected rate but still a "helluva lot of money."

In September 2020, a Kabbage executive wrote in an email that the consumer-credit-reporting agency Equifax found a PPP fraud rate between 4 and 10%, which amounted to as much as $80 billion in fraudulent funds through the lifetime of the program.

Blueacorn's owners pocketed nearly $300 million in loan-processing fees, and the House subcommittee report found they may have fraudulently received PPP loans themselves

The House subcommittee investigation found that the fintech Blueacorn in 2021 processed most of the loans facilitated by Capital Plus and Prestamos, the top two PPP lenders by volume that year.

According to the subcommittee investigation, Blueacorn made more than $1 billion from taxpayer-funded processing fees, of which $8.6 million funded the company's fraud-prevention efforts. Meanwhile, the report said the company gave $300 million in profits to its owners and $666 million to a marketing firm controlled by its senior leadership.

Former Blueacorn employees told the subcommittee that they received "poor training" and that they were pressured to "push through" PPP loans even if they suspected inauthentic applications.

The subcommittee investigation found that the Blueacorn founders Nathan Reis and Stephanie Hockridge received nearly $300,000 in PPP loans for themselves, facilitated through their own company. The report added: "In one application, Mr. Reis claimed to be an African American and a veteran, both of which appear to be false."

Womply generated over $1 billion in profits from PPP loans, and lenders described its fraud prevention systems as 'put together with duct tape and gum'

The fintech Womply generated more than $2 billion in loan-processing fees and had a gross profit of $1.8 billion in 2021, according to the report. Lending partners said the company allowed "rampant fraud" and described its fraud-prevention systems as "put together with duct tape and gum."

The subcommittee investigation found Womply received $5 million in PPP loans. The SBA later determined the company was not eligible for the loans and required the company to pay them back in full. That year, Womply's CEO and president earned salaries of more than $400,000 and received PPP loans.

Womply's CEO, Toby Scammell, who was convicted in 2014 of insider trading, led the company's fraud prevention

Womply's CEO, Toby Scammell, was convicted of insider trading in 2014 and has been barred from the securities industry. But he led the company's PPP fraud-prevention efforts.

The report said he resisted the federal government's efforts to gain information and told his staff not to cooperate with investigators.

Womply transferred millions of tax documents and bank data from PPP applicants to its cofounders' new business

In May, Womply notified customers that it had changed its privacy policy in order to transfer sensitive data to its founders' new business, Solo Global Inc., a mobile-payment platform.

In an email to staff, Scammell confirmed this included millions of tax documents and bank-account information from PPP-loan applicants. This meant that customers' sensitive information such as bank-account numbers, full credit-card numbers, geolocation data, tax-return details, Social Security numbers, and income information could be used to market and sell additional products, the report said.

Scammell did not tell the House subcommittee whether the company had transferred the data or how it's being used.

Kabbage employees were confused and concerned by the company's loan-review process

According to the House subcommittee report, Kabbage facilitated more than 310,000 PPP loans. Meanwhile, between May and June 2020, the company cut its risk- and account-review teams by about half.

According to the subcommittee report, one employee told her supervisor that she was "really uncomfortable with the review procedures" and that she believed "the level of fraud we're reviewing is wildly underestimated."

In October 2020, American Express acquired a majority of Kabbage's assets and a spinoff company took over PPP loan processing. That company had just one full-time employee handling fraud prevention. The report did not name that company.

Bluevine reduced fraud rates by improving software and review processes

The subcommittee report found that the fintech Bluevine initially saw high fraud rates but that its lending partner Celtic Bank stepped in with oversight and prevention measures. Bluevine implemented new software and manual-review processes that significantly reduced fraud cases.

But both Bluevine and Celtic Bank lacked timely reporting of fraud and suspicious activity to law enforcement, the report said.

Bluevine provided the following statement to Insider: "We are proud to have participated in the PPP program during a time that was truly extraordinary. As the subcommittee noted, all fintech companies are not the same, and Bluevine 'adapted to the ongoing threats better' than some of the other fintech companies examined in the inquiry."

Fintech and bank executives passed the buck to the SBA

The report concluded that there was little incentive for fintechs to monitor fraud because of the low risk to lenders who approved questionable loan applications.

In a May 2020 email, the CEO of Celtic Bank wrote: "The industry should push hard to make sure the SBA accepts the fraud risk."

Another bank executive said the Trump administration was too slow in providing guidance to prevent fraud.

The head of policy at Kabbage wrote in a September 30, 2020, email that it was "the SBA's shitty rules that created fraud," not Kabbage.

The CEO of the Florida mortgage lender Benworth, which provided PPP loans, expressed his concern about what he described as fraud unchecked by his fintech partner.

"When the party is over and the lights turn on, we will be the only ones at the party (and it seems standing naked)," he wrote in an email.

Fintechs face continued scrutiny

Fintechs may have blown their chance to be a part of future government loan programs.

The report called for "stricter oversight during emergency programs" and urged the Small Business Administration to examine whether unregulated businesses like fintechs should be allowed to participate in federal lending programs.

The report also called for further investigation into these companies and their contribution to fraud.

Popular Right Now

Popular Keywords

Advertisement